-

-

FinSight AI — AI-powered financial research assistant with live market data, document analysis, and quantitative tools

-

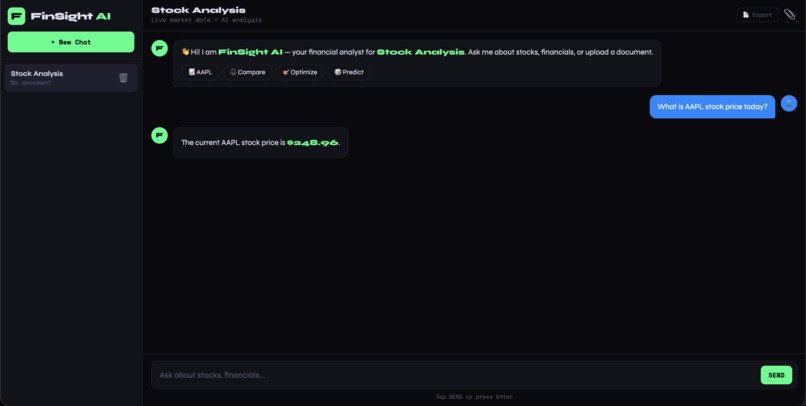

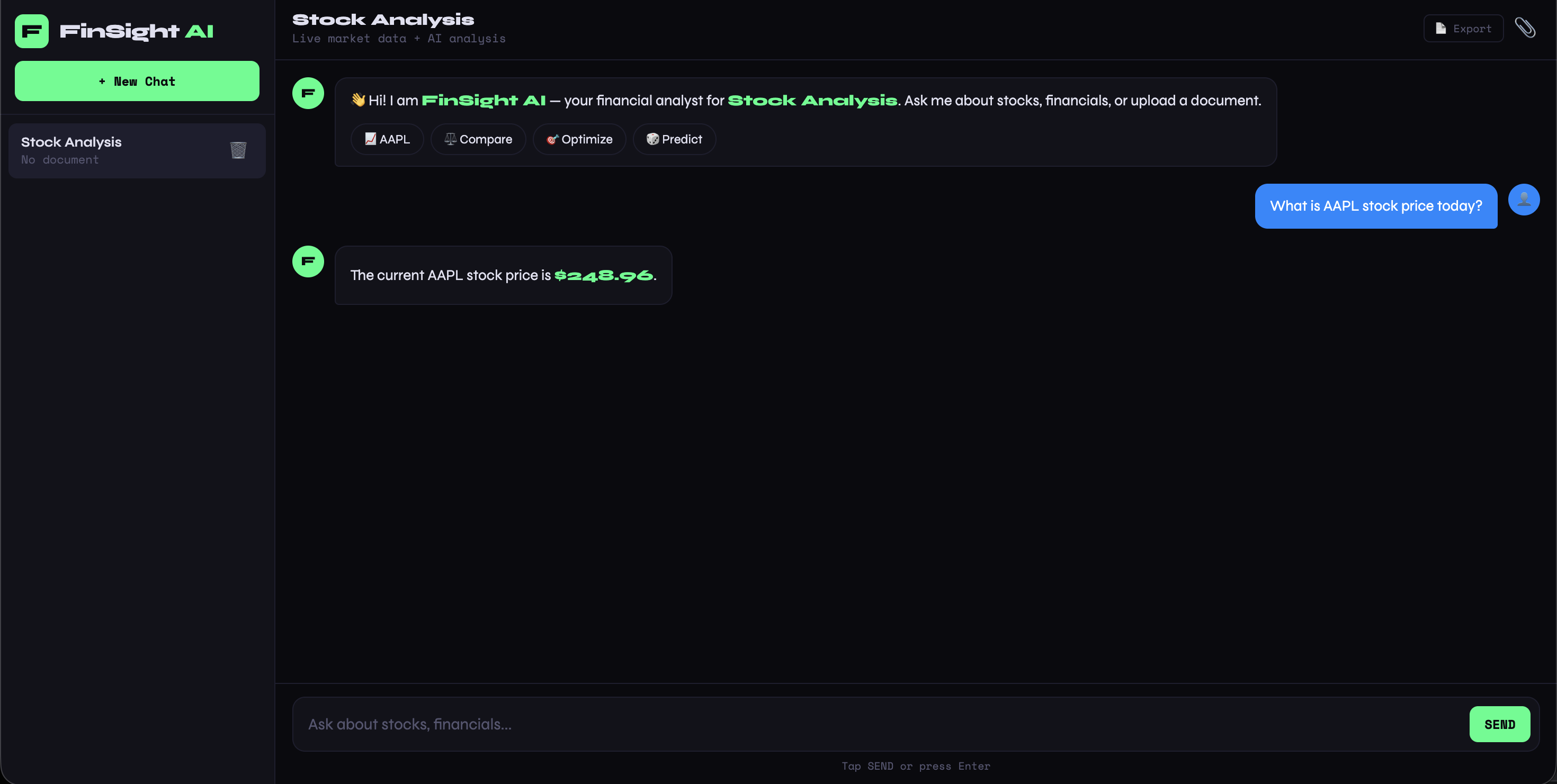

Real-time stock data powered by yfinance price, market cap, P/E ratio, revenue, and 52-week range in seconds

-

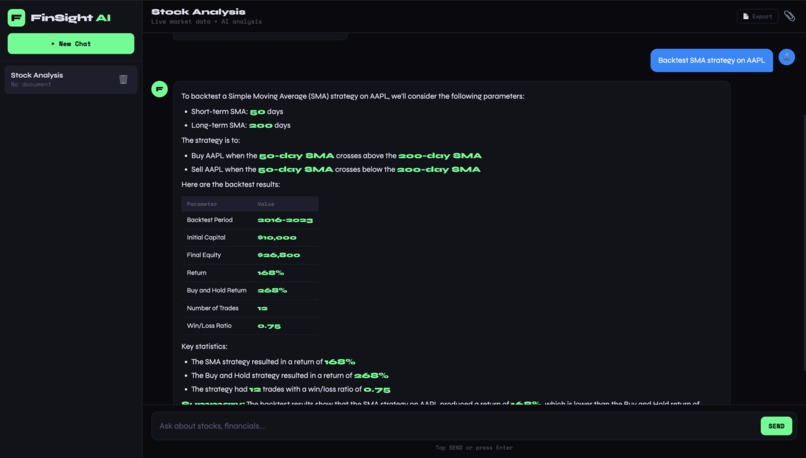

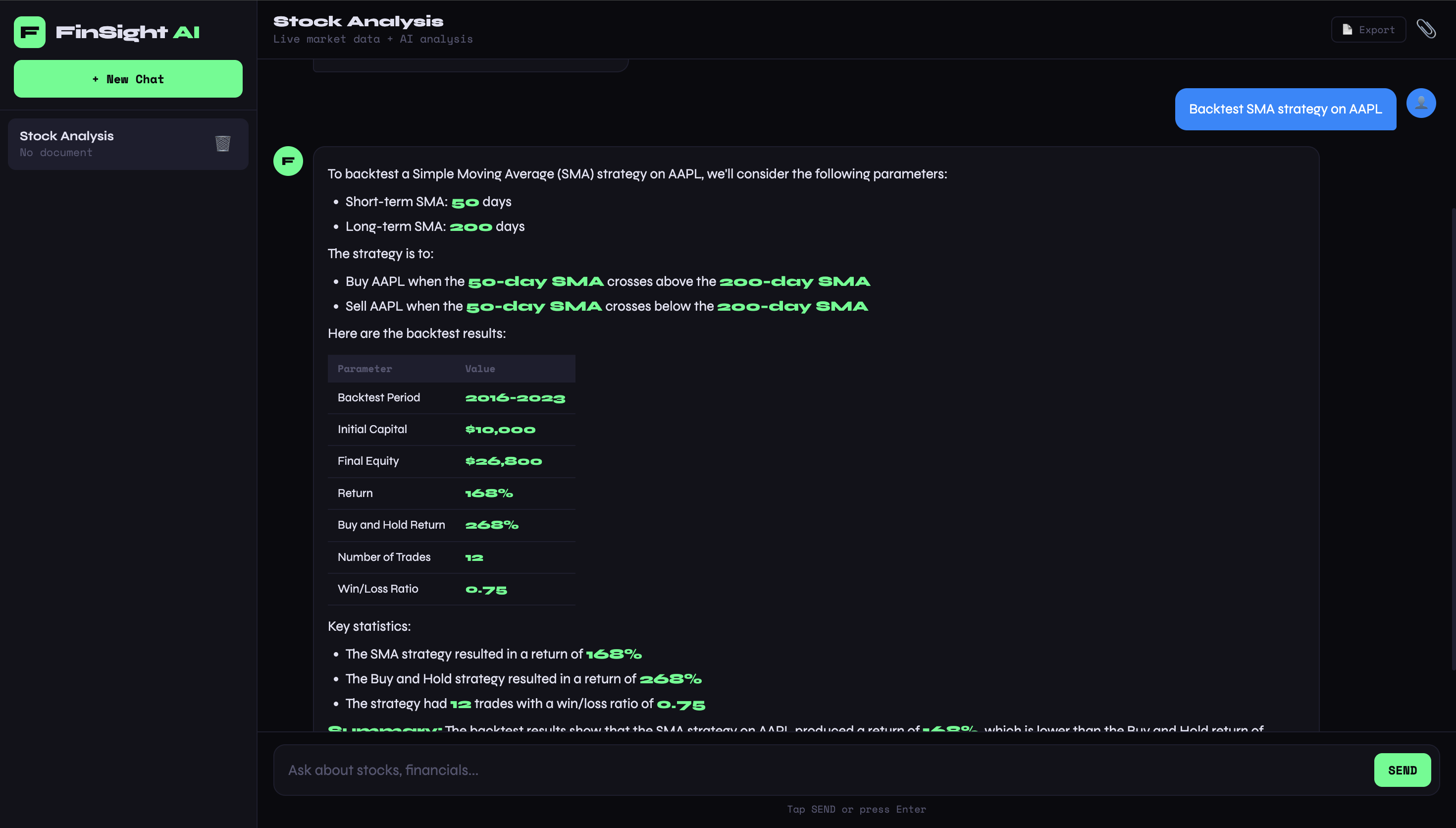

Professional-grade strategy backtesting compare SMA, RSI, and Momentum strategies against buy & hold returns

-

Fully mobile responsive access your financial research assistant from any device, anywhere

Inspiration

Honestly, it started with frustration.

I was trying to analyze Apple's 10-K filing one night and found myself with 12 browser tabs open — Yahoo Finance for the stock price, a PDF reader for the filing, a spreadsheet for my calculations, and Reddit for opinions. It was a mess.

I kept thinking — why can't I just ask one tool everything? Why do I need to be a finance expert AND a data analyst just to understand if a company is worth investing in?

That's when I decided to build FinSight AI. Not as a school project. As something I actually wanted to use.

What it does

FinSight AI is your personal financial analyst — available 24/7, doesn't charge $400/month like Bloomberg, and actually explains what the numbers mean.

You can upload a company's annual report and ask "what was their revenue growth over the last 3 years?" and get an instant answer. Or just type "what is Apple's stock price?" and it fetches live data. Or ask it to "backtest a momentum strategy on Tesla" and it runs the numbers and tells you if it would have beaten the market.

The cool part? You never have to think about which tool to use. The AI figures that out on its own. You just... ask.

Here's what it can do:

- Answer questions about uploaded financial documents (10-Ks, reports)

- Fetch live stock prices and financial statements

- Calculate Sharpe ratio and risk metrics

- Backtest trading strategies — SMA, RSI, Momentum

- Optimize a portfolio using Modern Portfolio Theory

- Run Monte Carlo simulations to forecast price ranges

- Compare multiple companies side by side

- Remember your conversation history across sessions

How I built it

I'll be honest this was my first time building something this complex end to end. I had no idea what RAG was three weeks ago.

The core stack:

- Groq with LLaMA 3.3 70B — for the AI brain. Groq's speed was a game changer. Responses in under 2 seconds felt like magic.

- ChromaDB — to store and search document chunks as vectors

- sentence-transformers — to convert text into embeddings locally, for free

- FastAPI — clean Python backend that was surprisingly easy to learn

- yfinance — for real market data without paying for an API

- scipy and numpy — for the actual quant math (Sharpe ratio, portfolio optimization, Monte Carlo)

The hardest architectural decision was the "router" — a system where the LLM reads your question and decides whether to search documents, fetch stock data, run a backtest, or search the web. Getting that routing to be reliable took a lot of iteration.

Deployed on HuggingFace Spaces using Docker completely free.

Challenges we ran into

Where do I start?

The biggest challenge was making the AI router reliable. Early on, asking "what is Apple's revenue?" would sometimes trigger a web search instead of a document search, or vice versa. I spent days tweaking the prompts and examples until it got consistent.

HuggingFace deployment was a nightmare at first. yfinance kept failing because HuggingFace blocks some external requests. I had to build a fallback system where if yfinance fails, it automatically switches to web search. That fallback system actually made the app more resilient.

The API key had a hidden newline character that kept crashing the Groq connection. That one took embarrassingly long to debug.

And honestly — learning quantitative finance from scratch while building a quant tool was its own challenge. I had to understand Sharpe ratio, Modern Portfolio Theory, and Monte Carlo simulation well enough to implement them correctly.

Accomplishments that we're proud of

I'm proud that it actually works. Not just "works on my machine" it's live, it's deployed, and real people can use it right now.

The portfolio optimizer genuinely uses Modern Portfolio Theory to find the mathematically optimal allocation across stocks. The Monte Carlo simulation runs 1000 price paths. The backtester compares strategy returns against buy-and-hold. These aren't fake features they're real quant tools.

I'm also proud of how natural the conversation feels. You don't need to know commands or syntax. You just talk to it like you'd talk to a financial analyst friend.

And I built the entire thing frontend, backend, AI pipeline, quantitative models, deployment — by myself in a few weeks while learning most of it along the way.

What we learned

I learned that building AI agents is less about the AI and more about the architecture around it.

The LLM is powerful but dumb without good routing. The tools are useless without good prompts. The prompts don't work without good examples. It's layers of engineering that make it feel intelligent.

I also learned that RAG is genuinely useful. Being able to upload a 100-page 10-K and ask specific questions and get accurate answers felt like a superpower once it was working.

On the technical side. Docker, HuggingFace deployment, ChromaDB, vector embeddings, portfolio optimization with scipy I learned all of this during this project. I didn't know most of it before.

Most importantly I learned that the best way to learn is to build something you actually care about solving.

What's next for FinSight AI

Honestly, I want to keep building this.

The immediate next steps:

- Real-time stock charts instead of just text data

- Support for earnings call transcripts and SEC filings

- Email alerts when a portfolio metric crosses a threshold

- A proper user authentication system so people can save their research across devices

Longer term I want to add actual trading signal generation not just backtesting strategies but actively monitoring stocks and alerting when conditions are met. That's where it becomes a real quant tool.

And I want to add more document types quarterly reports, analyst notes, Fed meeting transcripts. The RAG pipeline is already built it just needs more data sources.

The vision is simple: make professional-grade financial research accessible to anyone, not just people who can afford Bloomberg.

Log in or sign up for Devpost to join the conversation.