-

-

Join the waitlist! Coming soon!

-

-

💡 Inspiration

I grew up around money conversations early in a business family. Not in a flashy way, but in a practical way. Cash flow mattered. Tradeoffs mattered. Discipline mattered.

When I came to college and started fully owning my finances and actually earning, I hit a wall.

Every budgeting app showed me where my money went.

None of them told me where my money should go.

Even worse, none of them remembered who I was or what I cared about financially.

- My goals

- My relationship with money

- My risk tolerance

- My past behaviour and mistakes

- The financial rules we all follow intuitively but never write down

Personal finance is deeply personal, yet most financial software is stateless and overwhelming. Many apps bombard users with red numbers, charts, and alerts that quietly increase anxiety instead of reducing it.

This matters because the problem is real and widespread.

More than 70% of Gen Z in the U.S. cannot cover a \$400 emergency expense.

That disconnect is why Finny is designed to guide decisions, not just track them.

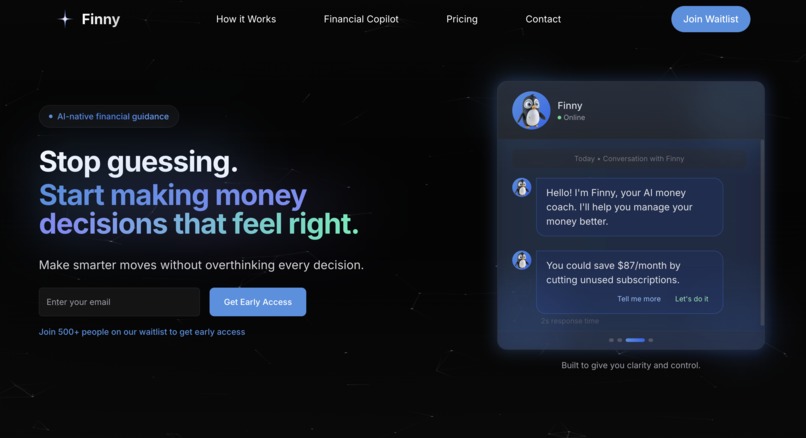

🧠 What it does

Finny is a money coach powered by deep, de-personalized memory. Instead of acting like a mirror, Finny acts like a calm advisor.

It does not just say:

Here’s what you spent

It says:

Given who you are and your goals, here’s what you should do next

Finny remembers stable, long-term truths about a user, such as:

- Financial values and priorities

- Risk comfort and stress thresholds

- Behavioral spending patterns

- Implicit financial rules the user follows

These memories persist across sessions and personalize:

- Budget guidance and spending feedback

- Financial tips and notifications

- The tone and communication style of the assistant

- What Finny emphasizes or intentionally avoids

The goal is simple: reduce anxiety and replace overwhelm with clarity.

🛠️ How we built it

At the core of Finny is Super Memory, which acts as a system-level memory layer, not a chat add-on.

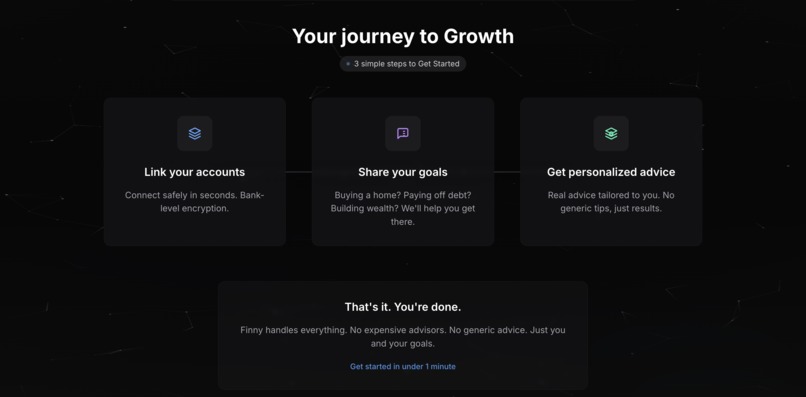

We securely connect users via the Plaid API to understand real financial behavior across checking, savings, credit, and investment accounts. Instead of treating this data as something to store forever, we treat it as something to learn from, abstract, and then discard.

The system architecture works as follows:

1️⃣ Data and interaction layer

Transactions, conversations, and user actions flow naturally through the app.

2️⃣ Signal extraction layer

Instead of storing raw financial data long-term, we extract stable signals such as preferences, constraints, behavioral patterns, and stress thresholds.

3️⃣ Supermemory layer

These signals are stored as durable, de-personalized memory objects.

No raw balances. No sensitive snapshots. Just judgment.

This is where the product jumped from rule-based logic to adaptive judgment without hardcoding financial heuristics.

4️⃣ Agent routing and decision layer

Every user query first passes through a classification layer that determines:

- Does this require long-term memory?

- Does it require real-time user financial data?

- Does it require a web search?

- Or can it be answered purely from existing context?

Memory is the default. Tools are invoked only when necessary.

5️⃣ Response generation layer

Final responses are generated using the appropriate combination of memory, user data, and external knowledge.

We also integrated the FinHub API and Web Search to enable stock analysis directly inside chat, allowing users to analyze individual stocks without leaving the app.

Memory is not a feature in Finny. It is the infrastructure.

⚠️ Challenges we ran into

Deciding what not to remember

Financial data is massive and historical. Storing everything increases noise, risk, and latency.Designing with psychology in mind

Most budgeting apps unintentionally create anxiety through dense numbers, red colors, and constant alerts. We applied principles from behavioral psychology to make Finny feel calm, controlled, and supportive.Making memory invisible but everywhere

Memory powers almost everything — tips, notifications, recommendations, goals planning, how finny answers — without ever feeling explicit!Maintaining low latency and smooth UX

Years of financial history had to be abstracted into memory without slowing down the experience.

🏆 Accomplishments that we're proud of

- Building a de-personalized memory layer embedded across the core of the app

- Designing an agentic system that focuses on what matters based on what Finny already knows

- Giving users control over communication style, allowing Finny to adapt how it speaks

- Learning from spending behavior, not just balances or categories

- Combining memory and behavioral insight to create a calm, human financial experience

- Turning a memory system into a finance-aware judgment layer without modifying Super Memory itself.

This is where Finny stopped feeling like a tool and started feeling like an advisor who knows me.

📚What we learned

The biggest insight was simple:

Personalization is not about more data. It’s about better abstraction and acknowledgment.

- Balances change

- Expenses come in

- Numbers fluctuate

But values, habits, and constraints persist.

When memory stores judgment and behavior instead of raw data, the system becomes more private, more trustworthy, and more useful over time.

Super Memory opened the door to deeply embedded personalization across the entire app. It fundamentally changed how we think about personal finance software — not as dashboards that report numbers, but as systems that understand context, intent, and long-term patterns.

Good memory design is mostly about restraint.

🚀 What's next for Finny

Next, we plan to go deeper.

- Expand into investment intelligence, including deeper portfolio and allocation analysis

- Build richer stock-level insights using FinHub and other market data with world class UI

- Use spending behavior and memory signals to guide capital allocation decisions

- Go deep into Financial planning for people all stages of life like couples counseling, 50-year old planning for retirement, etc.

Our short-term focus is new grads and early-career professionals navigating their first paychecks, savings, and retirement accounts.

Long-term, the vision is bigger.

Finny aims to become the go-to personal finance tool for every stage of life — from freelancers with irregular income, to couples planning together, to individuals approaching retirement.

Personal finance should never feel overwhelming.

It should feel calm, controlled, and human.

Built With

- genai

- multi-agentic

- plaid

- react-native

- supabase

Log in or sign up for Devpost to join the conversation.