-

-

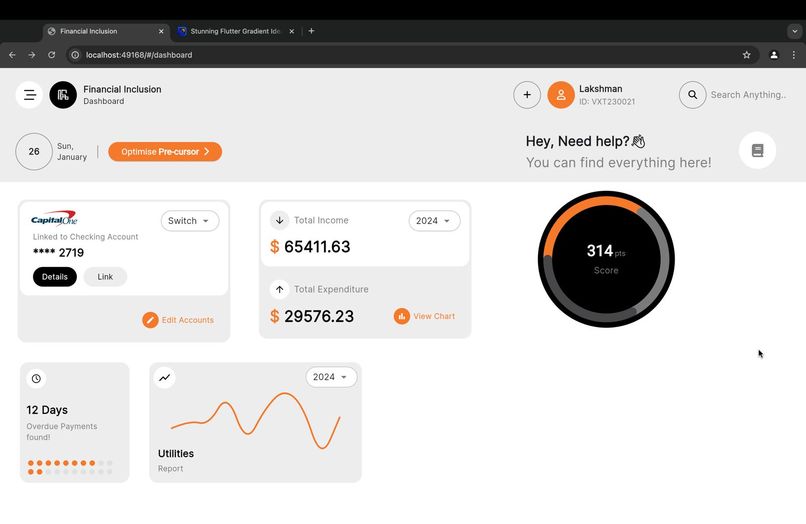

Dashboard

-

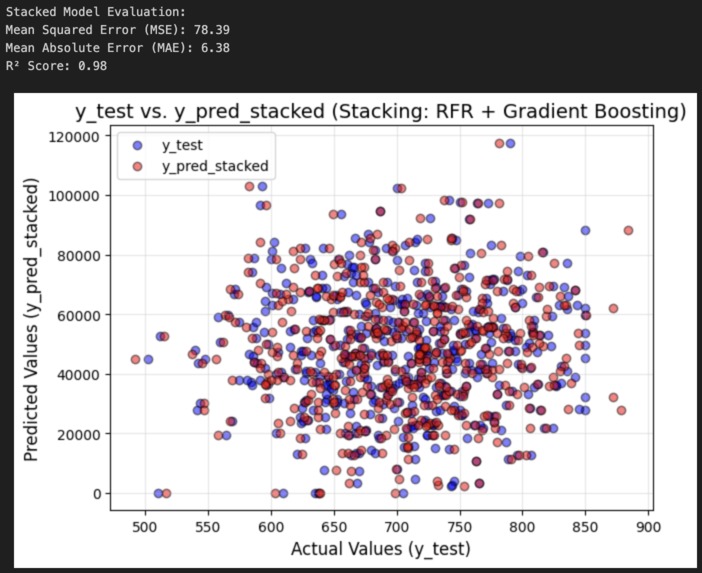

Model Results

Inspiration

As students, we encountered a harsh reality when trying to apply for our first credit cards: no credit history means no credit opportunities. Despite paying rent on time, handling bills responsibly, and managing our finances with care, we were still deemed "invisible" by traditional credit systems. This personal frustration led us to a bigger realization: we were not alone. Over 40 million individuals in the U.S. face the same problem—they are financially responsible but labeled "credit-invisible." This includes gig workers, students, immigrants, freelancers, and low-income earners.

What started as our own challenge became a mission. We wanted to break the barriers of traditional credit scoring and give everyone an equal shot at financial opportunities. Because everyone deserves to be seen—not just as numbers but as stories of responsibility and determination.

What it does

Our solution, "Financial Inclusion," is an alternative credit scoring platform designed to empower the credit-invisible. It uses real-life financial behaviors—like paying rent, utility bills, subscription services, and taxes—to create a fair, transparent, and actionable credit score.

Here’s how it works:

- Data Integration: Users connect their rent, utilities, and subscription accounts, and provide access to income or tax data through APIs.

- Real-Time Scoring: Our algorithm processes this data, evaluating factors like payment timeliness, income stability, and expense consistency.

- User Dashboard: Users see a detailed breakdown of their credit score, with insights and recommendations to improve it.

- Lender API: Partner banks and fintechs access this score to offer credit products, empowering users with loans, credit cards, and financial opportunities.

How we built it

Brainstorming the Framework: We started with the question: "What defines financial responsibility?". This led us to identify alternative data sources—rent, utility bills, subscriptions, and tax filings—as key indicators of responsible financial behavior.

Data Modeling: We created mock datasets representing diverse user profiles, from gig workers with irregular income to students balancing low income with high education expenses. We even simulated outliers like retirees with no savings or students overspending on luxury goods.

Algorithm Design: Our scoring algorithm considers:

- Savings and Financial Discipline

- Employment Stability

- Bill Punctuality

- Dependents and Obligations

- Overdraft Fees

- Aspirational Spending

- Missed Payments The final score ranges from 300 to 850, representing credit readiness based on real-life financial habits.

Challenges we ran into

Every step came with unique challenges:

- Bias in Scoring Models: Traditional credit systems often inherit biases, and we worked hard to ensure our algorithm remained fair and unbiased across demographics.

- Data Privacy: Handling sensitive financial data responsibly was non-negotiable. We had to implement strict encryption protocols and compliance measures.

- Complex Mock Data: Simulating diverse user profiles—gig workers, retirees, students—while maintaining realistic financial behaviors was a tricky but rewarding task.

- Time Constraints: Hackathon deadlines meant sleepless nights, quick pivots, and team debates. But every hurdle made us stronger.

Accomplishments that we're proud of

- Breaking Barriers: We built a platform that shines a light on the credit-invisible, empowering individuals often overlooked by traditional systems.

- Inclusive Design: From gig workers to students, our platform is designed to work for everyone.

- Real-Time Insights: The interactive dashboard gives users clear, actionable advice to improve their financial standing.

- Collaboration Under Pressure: Despite tight deadlines, we came together as a team to solve a real-world problem.

What we learned

This journey taught us more than just technical skills:

- Empathy in Design: Understanding the struggles of the credit-invisible helped us design a platform that truly serves people.

- The Power of Alternative Data: Financial responsibility isn’t limited to credit card transactions; it’s in everyday actions like paying rent and bills.

- Teamwork Matters: Collaboration, communication, and late-night brainstorming fueled our success.

- Inclusivity is Key: Financial systems must adapt to serve everyone, not just those who fit a traditional mold.

What's next for Financial Inclusion

The journey doesn’t stop here. Here’s how we envision the future of "Financial Inclusion":

- Scaling the Platform: Partnering with more banks, fintechs, and service providers to expand the reach of our scoring system.

- Advanced AI Models: Implementing machine learning to refine credit scoring accuracy and fairness.

- Global Accessibility: Adapting the system to serve underbanked populations worldwide, especially in developing nations.

- Education and Awareness: Launching financial literacy programs to help users better understand and improve their credit scores.

- Policy Advocacy: Working with policymakers to promote alternative credit scoring as a recognized standard for financial inclusion.

Log in or sign up for Devpost to join the conversation.