-

-

-

-

-

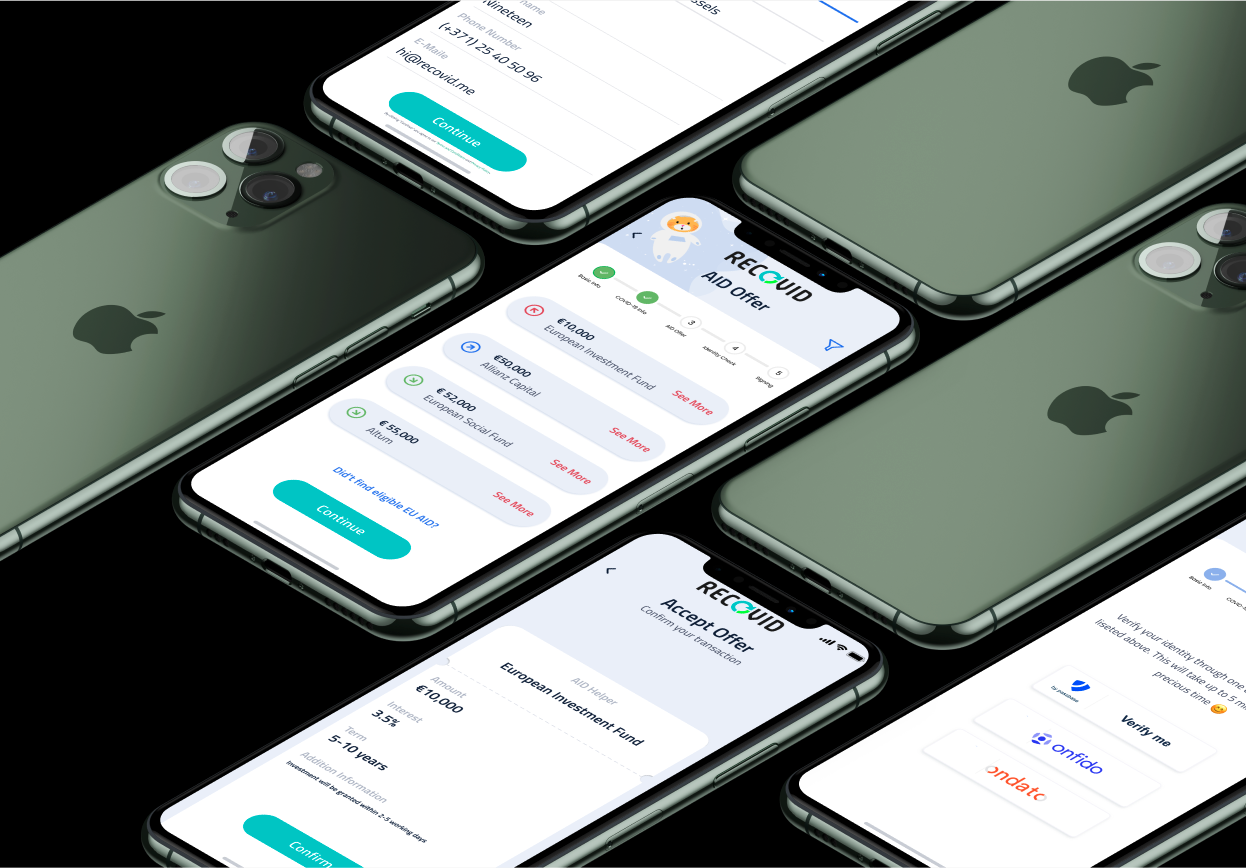

UI

-

Ideation

Inspiration

SMEs and self-employed people form the backbone of the European economy. Over two thirds of Europeans are employed by SMEs*, so are vital to the health of the EU economy. Many European nations have identified the urgent need to ensure SMEs will remain financially secure, but have implemented solutions with varying success.

Small business owners and freelancers do not have access to the fast and seamless finance options generally available to large companies, resulting in SMEs being at the centre of the economic crisis brought on by the COVID-19 pandemic and containment measures. The severity and speed of the damage to SME finances are much worse than during the 2007-2010 financial crisis.

Due to the extreme speed and severity of the onset of the crisis, moral hazard in providing financial assistance is an almost non-existent problem - all SMEs in almost all sectors require urgent assistance. Vulnerability to the simultaneous supply- and demand shocks has instantly dried up liquidity for a large proportion of SMEs. Without urgent and targeted action, many companies will not make it through the coming 6 months, even if the economic shutdowns are lifted within the next few weeks.

Neither the sources of funding, such as fiscal stimulus and taxpayer-funded payments, nor the distribution methods (commercial bank loans and very slow government payments) used until now, as part of the 2020 emergency funding packages, have achieved the required results to save SMEs from extreme financial distress. This temporary distress may soon lead to financial ruin. The interdependencies of SMEs in different EU member states means that if a small company in Italy fails, a small company in Denmark could fail, bringing further failure to a small company in Poland. Urgent, co-ordinated EU-wide action is indeed required.

Fast central bank interventions, though not completely flawless, helped to improve some of the impacts of the 2007-2010 financial crisis. To date, mostly fiscal stimulus and government tax-payer funded assistance has been provided. Direct central bank (ECB and national EU member state central banks) injections via the payment networks of commercial banks have not yet been implemented.

Distribution of loans through commercial banks is an outdated system because:

- Processes are bureaucratic and slow by design

- Loans are not granted to companies in severe financial distress

- Banks are risk averse and their approach of avoiding moral hazard during ‘normal’ economic times (i.e. they are designed to avoid giving money to companies that are failing) means they are ill suited to make the correct choices to assist companies in distress

What it does - the problem that our RECOVID solves

RECOVID addresses the emergency need of efficiently conveying liquidity in the form of rescue packages to huge numbers of SMEs and self-employed due to the Covid-19 crisis.

RECOVID is a EU-wide scalable platform that aims at serving millions of interactions simultaneously. It will make SMEs and self-employed rescue packages application process easy and secured thanks to:

- Seamless onboarding

- Latest authentication techniques to minimise fraud (KYC & AML)

- Fast access to financial data through open banking (PSD2)

- Fast payment

On their end, European institutions (European Commission and European Funds) will benefit from an efficient dashboard to assess the overall economic situation - by sector, company size etc. - in real time. Such dashboard will provide European institutions with advanced data analytics to:

- Assess the overall economic situation in real-time

- Assess the performance of rescue packages in real-time

- React to a fast-changing environment by quickly implementing missing rescue packages where and when needed

- Allow a fair, secured and efficient allocation of funds to the most impacted throughout EU

*https://ec.europa.eu/eurostat/web/products-eurostat-news/-/WDN-20180627-1

What is the expected impact of RECOVID on the crisis

- RECOVID is the “intensive financial care” that European SMEs need to go through the crisis.

- RECOVID will ensure that no SME or self-employed who were up and running before this crisis occurred go bankrupt because financial support came too late.

- Overall RECOVID not only tackle the current crisis but shall have brought the EU Commission to reengineer its funding allocation process.

How we built it

Front-end: Built using FIGMA

Back-end: Will be developed in Python

Integrations: => Open banking API thanks to the BANKIO team of this hackathon (https://www.obanky.com/) => Company information APIs => AI for cash flow analysis

Design thinking session were facilitated by Moonlab using Miro

Challenges we ran into

ECB and EU member state central banks need to authorise liquidity operations

Accomplishments that we are proud of

- Collaborating as a strong and diverse team of driven professionals from 8 nationalities in several time zones driven by the same cause

- Setting the basis for a new EU rescue packages allocation process over a hackathon weekend

What's next for RECOVID, and what we need in order to continue the project

- Get green light from the European Commission to develop the technical solution

- Showcase the dashboard solution to local authorities, funds and legacy

- Sign partnership agreements with Aggregators, Data providers and APIs companies

- Promote and make the platform operational for all EU SMEs and institutions shortly

- Further developments to be considered Digital currency and smart contracts to precisely target allocation and use of rescue funds thanks to our partner Keyko (please see gdoc attached for your reference)

The value of the RECOVID platform after the crisis

- Remain the unique and easily actionable financial rescue platform to react fast to any future crisis and always keep the EU economy afloat

- Leverage on the data to allow EU fintechs to build fit for purpose solutions to the crisis and augment this platform over time

Built With

- api

- figma

- python

![Jana [theoryforce.com]](https://avatars1.githubusercontent.com/u/62735423?height=180&v=4&width=180 "Jana [theoryforce.com]")

Log in or sign up for Devpost to join the conversation.