-

-

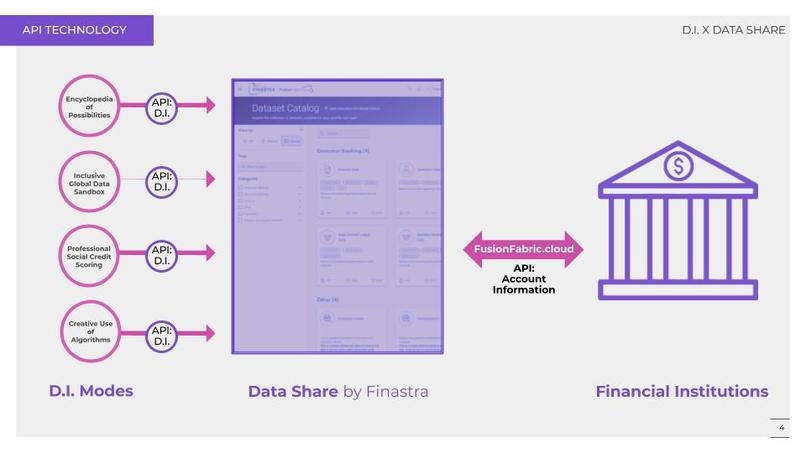

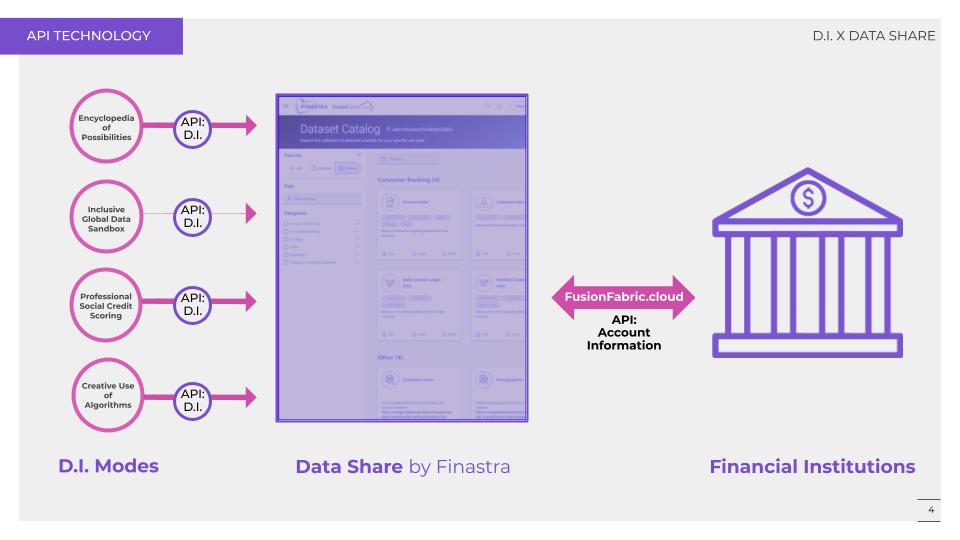

Technology - Dataset Integration

-

Technology - API Structure

-

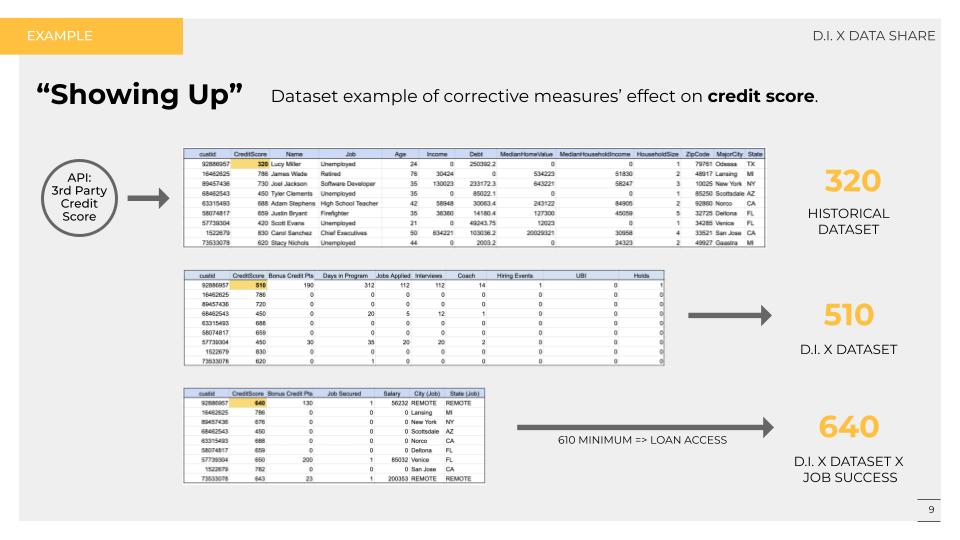

Technology - Dataset Models

-

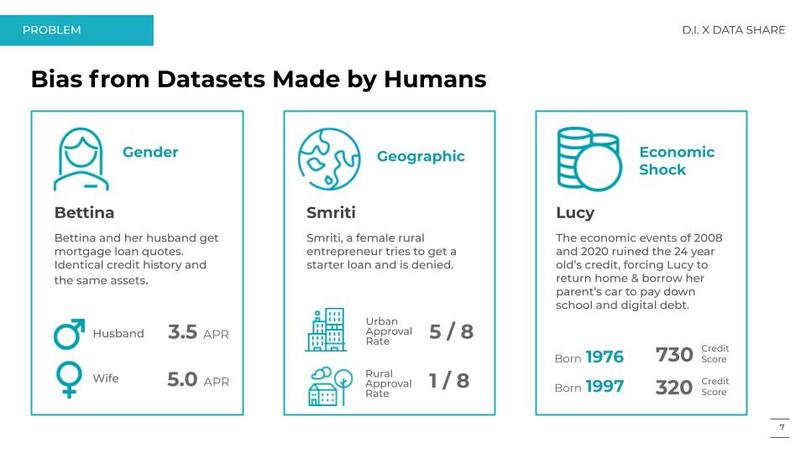

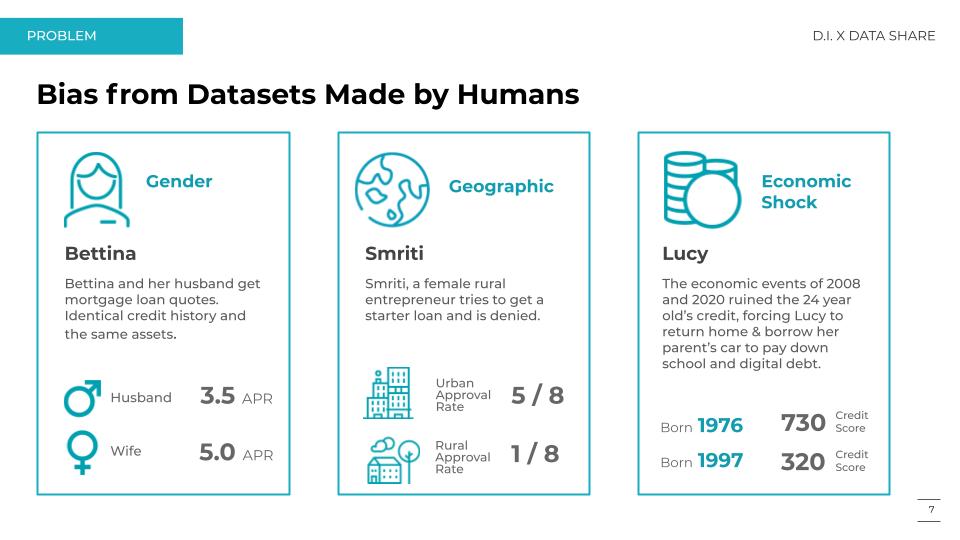

Human - Bias Problem

-

Human - One D.I. Solution

-

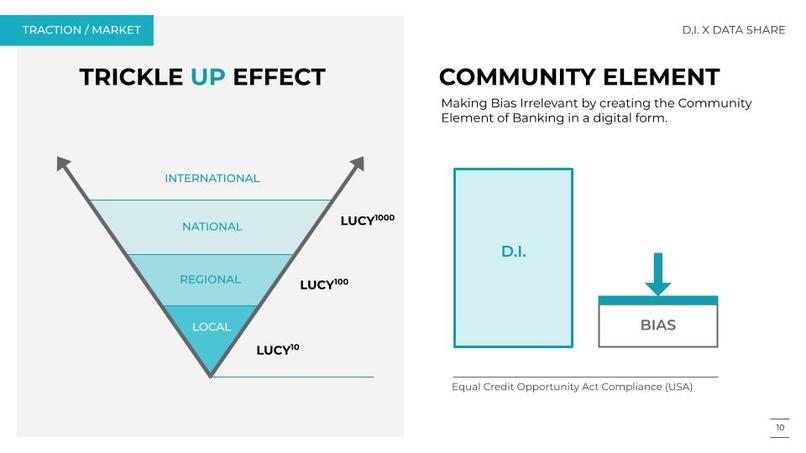

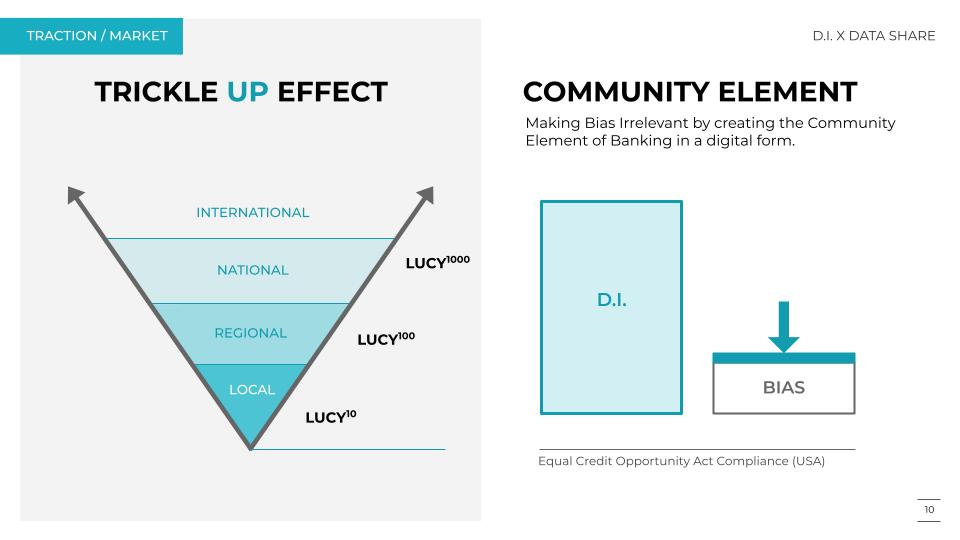

Business - Traction/Market

-

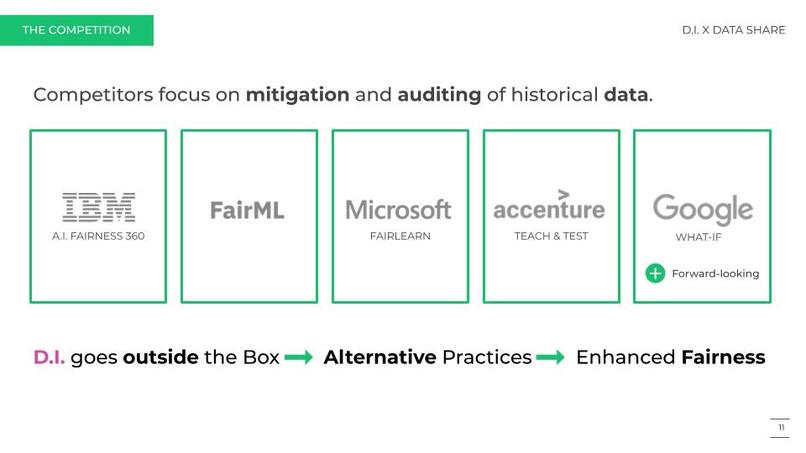

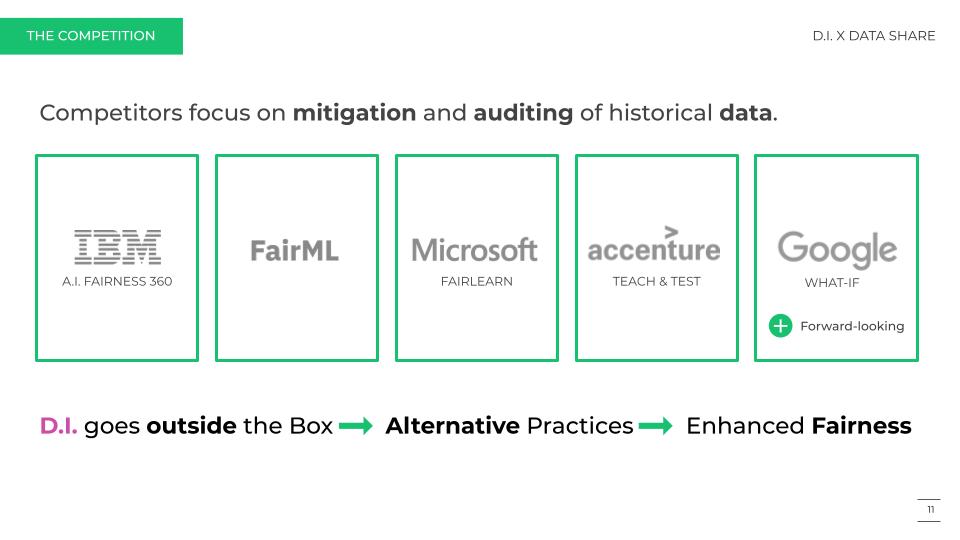

Business - Competition

-

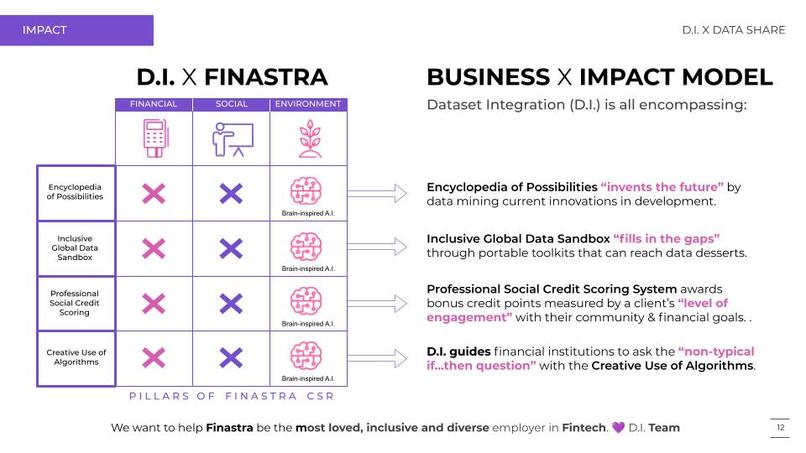

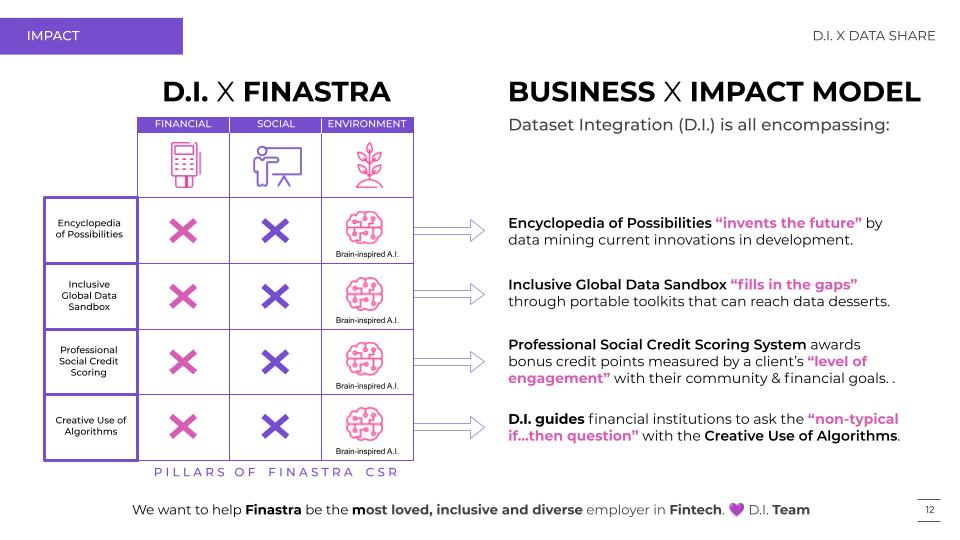

Business - Impact Model

Vision

In Weapons of Math Destruction, Cathy O’Neil writes:

Big Data processes codify the past. They do not invent the future. Doing that requires moral imagination. And that’s something only humans can provide.

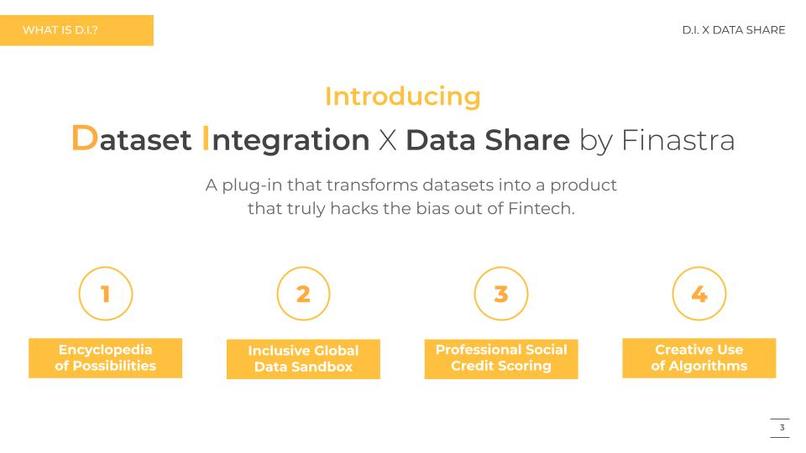

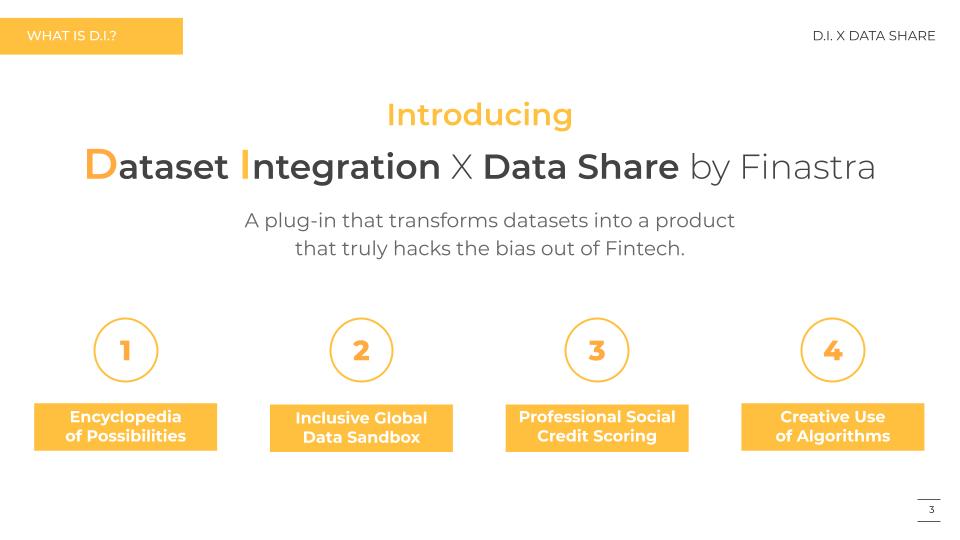

What is D.I.?

DATASET INTEGRATION.

D.I. uses a four-prong mode to enrich historical datasets, they are:

- Encyclopedia of Possibilities

- Inclusive Global Data Sandbox

- Professional Social Credit Scoring System

- Creative Use of Algorithms

These four modes tackle historical biases in different ways. Together they act as an antihistamine to human bias, generating antibodies to counteract its damage.

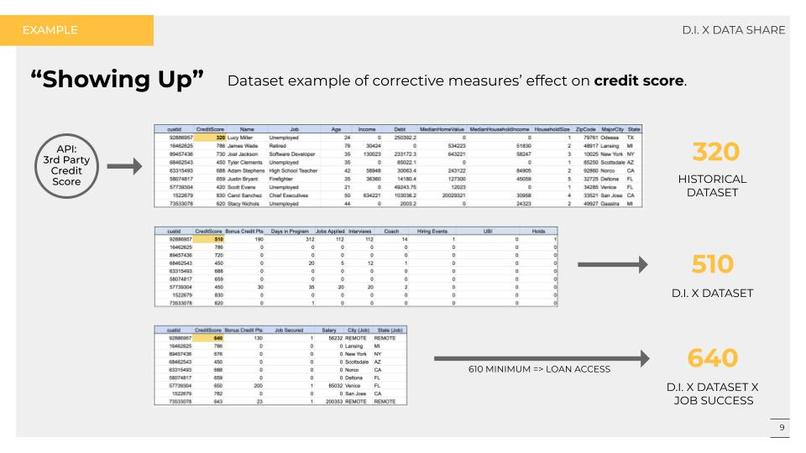

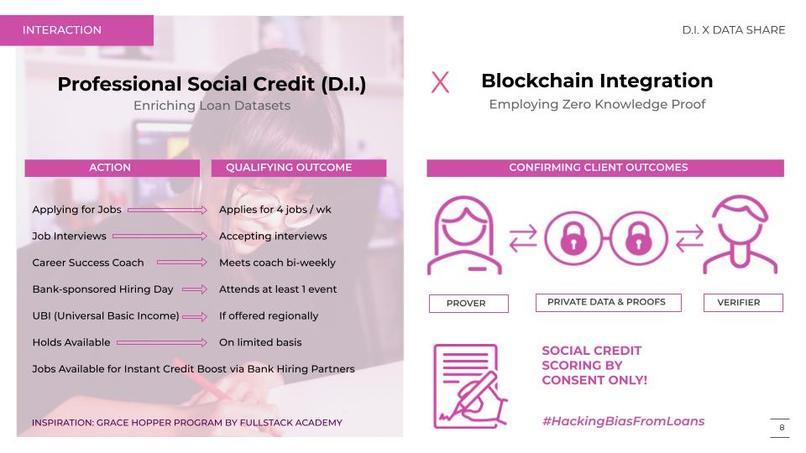

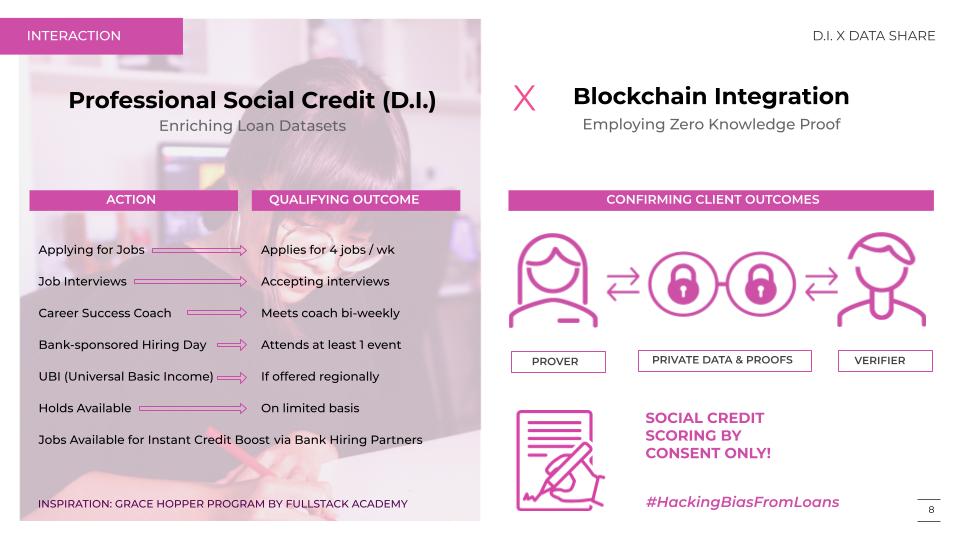

PROFESSIONAL SOCIAL CREDIT SCORING SYSTEM.

This submission will go deeper into the third listed mode, the Professional Social Credit Scoring System (PSCSS). PSCSS generates a "Community Element" credit score to be merged into the traditional "Number-Driven" credit score.

Landscape

THE NEOCLIENT. Born in the 21st century, neoclients are coming-of-age at a time when the ownership economy is shifting back to a sharing one. Thus the idea of risk calculations based on ownership loans is becoming less relevant. These neoclients are also interested in value-focused investing in socially-driven missions that insure their well-being and survival. Millennials alone surpass the total Baby Boomer population by 4 million. Banks need to pay attention to this young growing giant client base and their needs and wants.

IN-PERSON BANK TO DIGITAL BANK. The term “bank” has transformed from a noun to a verb. More clients demanding convenience will expect to be “banking at a bank” versus “going to a bank”. Thus the shift to online banking must happen as supply must meet demands.

THE RISE OF NEOBANKS X SUPER APPS. Neobanks do not have physical locations, which is leading to increased churn. Super Apps that offer a frictionless bespoked all-encompassing experience for clients ensure that their clients don't leave to bank elsewhere.

ARTIFICIAL INTELLIGENCE. Companies are using Artificial Intelligence (A.I.) to create their Super App.

ECONOMIC SHOCK FREQUENCY INCREASING. The news talk about the continued proliferation of new super viruses which have the potential to create repetitive economic shocks..

Problem

Arguably in ten years, any company without a contribution to their community’s future, may itself be without one.

INCREASED COMPETITIVE FINANCIAL INSTITUTION ENVIRONMENT. As blockchain technology reduces the revenue of Financial Institutions (FI), FIs will need to aim for volume by serving all niche clients. Human bias is an obstacle to this.

HUMAN BIAS IN ARTIFICIAL INTELLIGENCE. A.I. is built by humans, so human error in A.I. is unavoidable and can create bias. Human biases limit a bank's ability to loan to historically written off populations.

UNI-DIMENSIONAL CREDIT SCORING. Credit Reporting Agencies (CRA) like Experian, Transunion, and Equifax pool/buy their data from financial-like sources such as banks and utility billing companies. They calculate their scores based on these numbers. But people are human and there is another side that needs to be considered, a side we call the “Community Element”.

Key Benefits of a Professional Social Credit Scoring System

NEOCLIENT. Increased access to loans.

COMMUNITY BANKS | CREDIT UNIONS. As part of their mission to serve the community, basing loans on a credit score that does not reflect the "Community Element" would run counter. PSCSS digitizes the "human aspect" of community banking, so that community-focused FIs do not need to sacrifice their core values when transitioning to a digital platform.

NEOBANK. With banks hungry to do proper risk calculations of individuals and businesses affected by Covid-19, the digital community element score becomes an important risk-controlled path for banks to give loan access to many more by bypassing inherited biases.

FINASTRA. PSCSS and D.I. as a whole, can help support Finastra’s CSR goals, in addition to many others.

What is next for D.I.

The D.I. Team would love the opportunity to meet with Partners interesting in developing Dataset Integration in an altruistic and sustainable way.

Update: This project is being converted into a white paper with the help of a research institution. Stay tuned.

#ChoosingToChallenge Bias in Fintech

Log in or sign up for Devpost to join the conversation.