🪙 DhanGyan — धनज्ञान

India's First AI-Powered Financial Empowerment Game

"Don't teach financial literacy. Let people LIVE it."

💡 The Spark — A Silent Crisis No One Was Talking About

India is growing at 8% GDP. Yet in the shadow of this glittering progress, a silent financial pandemic is spreading — one spreadsheet, one moneylender, one BNPL trap at a time.

We didn't find this crisis in a research paper. We found it in people.

We met Ravi — a wheat farmer in Madhya Pradesh, sharp, hardworking, deeply in debt. Not because he spent recklessly, but because nobody ever told him that the moneylender charging him 3% per month was actually charging him 36% per year — nearly 10× the rate of a Kisan Credit Card. He didn't lack intelligence. He lacked information delivered at the right time, in the right language, in a way that felt real.

$$\text{Annual Moneylender Rate} = (1 + 0.03)^{12} - 1 \approx 42.6\%$$

$$\text{vs. Kisan Credit Card Rate} \approx 4\%$$

That gap — 38.6 percentage points — is the gap we decided to close.

We met Priya — a first-year college student in Pune, swiping her first "Buy Now, Pay Later" app like it was free money. She had no idea that missing two payments would spiral into a credit score she'd spend three years repairing.

We met Arjun — a ₹1.4 LPM software engineer in Bengaluru, somehow carrying ₹45,000 in revolving credit card debt because the minimum payment UI deliberately made full payment feel optional.

And we met Lakshmi — a home manager in Tamil Nadu who single-handedly ran a ₹40,000/month household budget in her head, yet froze with anxiety every time someone asked her to "just use UPI."

Four stories. One systemic failure. Financial education in India is either non-existent, inaccessible, or so detached from lived reality that it simply doesn't work.

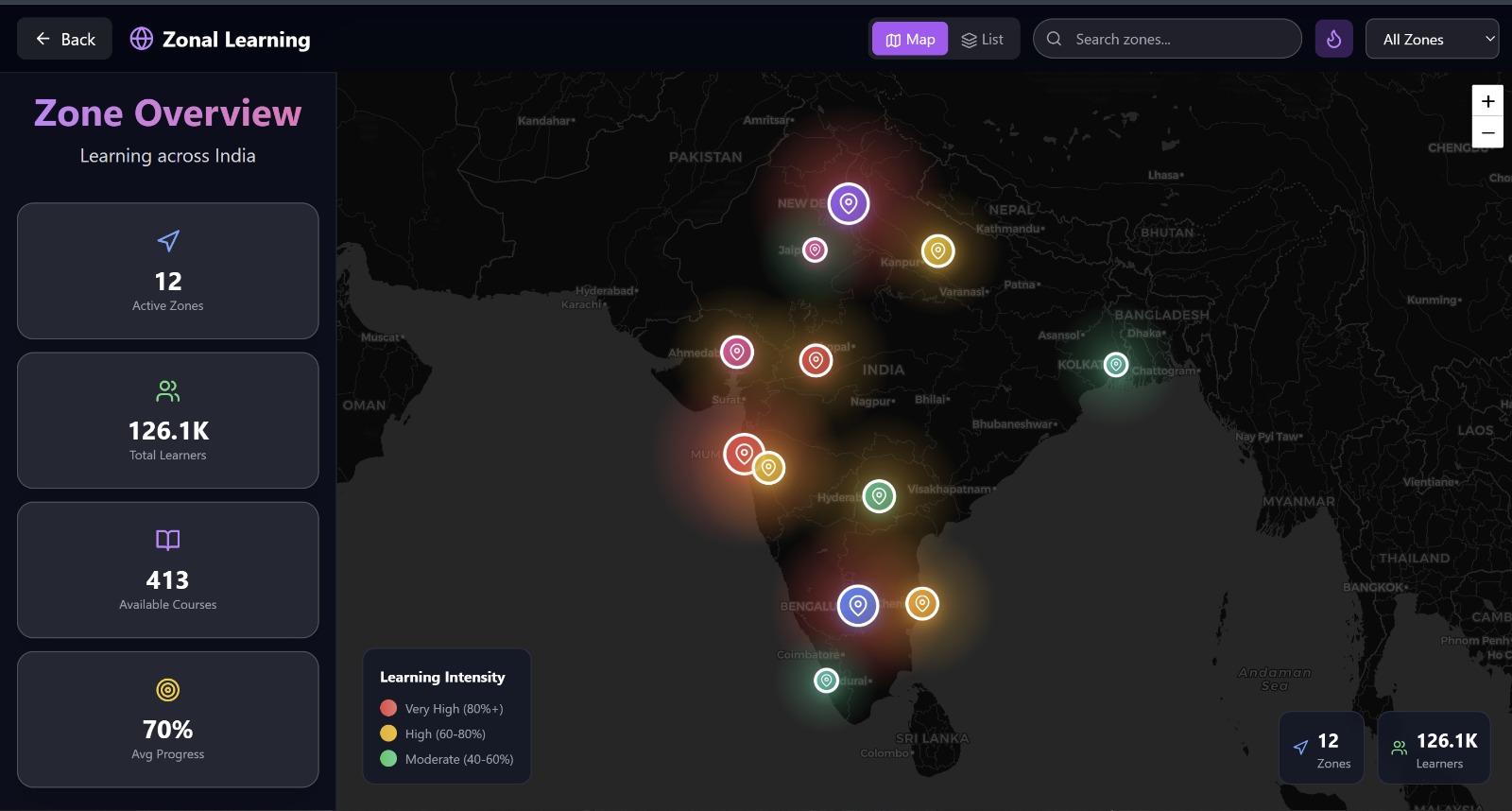

45% of India's 270 million farmers are trapped in high-interest debt cycles. 90% of students receive zero financial education before college. 60% of millennials carry debt averaging ₹45,000. 80% of women manage household finances — yet most are excluded from formal financial systems.

This is not a financial problem. This is a knowledge delivery problem. And we built DhanGyan to solve it.

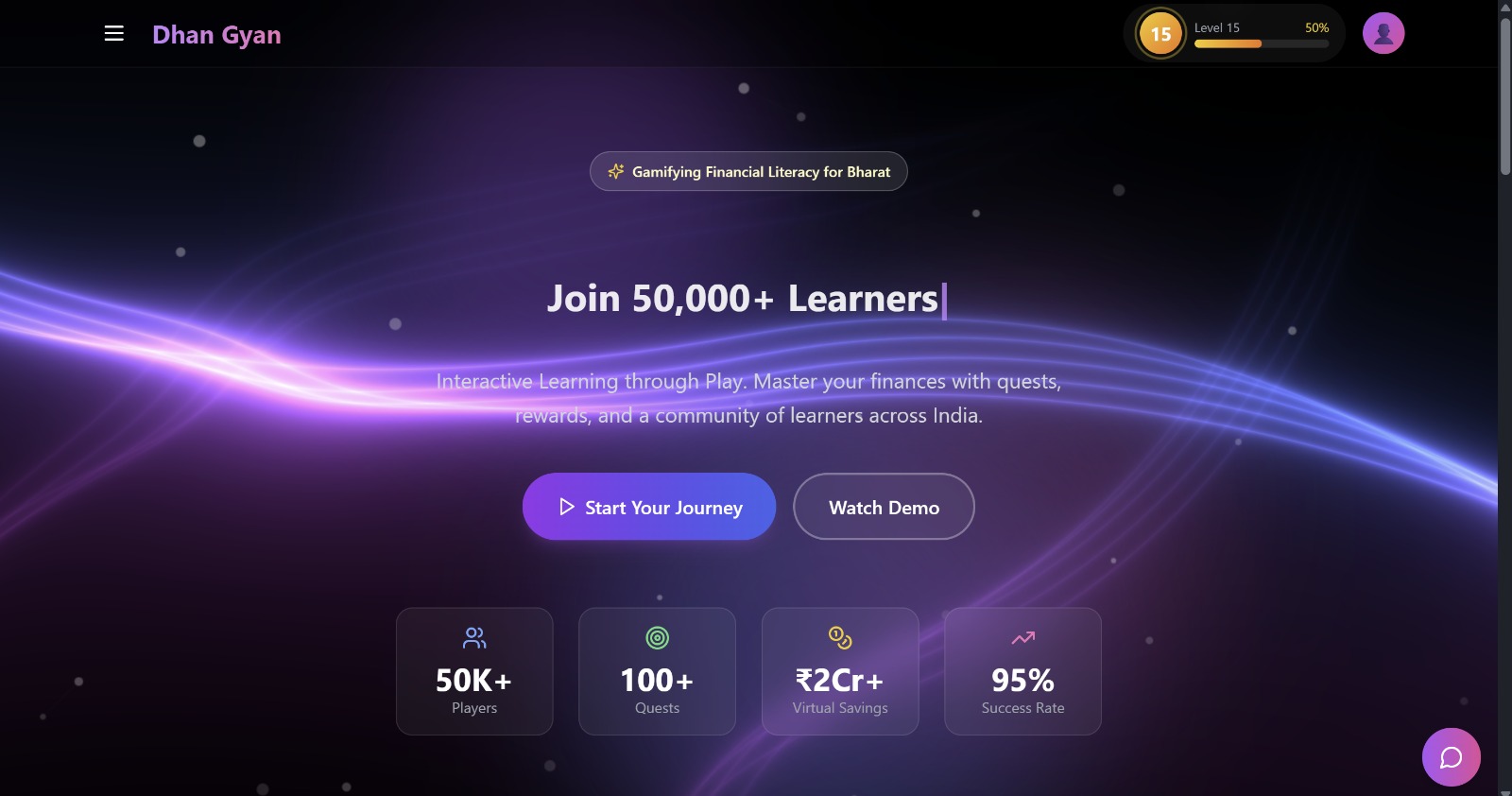

🔥 What We Built — A Financial Empowerment Ecosystem

DhanGyan is not a course. It's not an app. It's a living, breathing financial simulation — an ecosystem where users step into the financial life of someone just like them, make decisions, face consequences, earn rewards, and emerge transformed.

We built it around one radical belief:

The best teacher is not a lecture. It is a consequence you survive in a safe environment.

The Four Pillars of DhanGyan

🧠 Pillar 1 — AI-Personalized Life Paths

Every user begins by choosing their Financial Avatar — Ravi, Priya, Arjun, or Lakshmi. The platform immediately calibrates to their reality: language, income level, risk profile, and the specific financial traps most likely to affect them. The Gyan Assistant (powered by Google Gemini API) acts as a personal financial coach — not a chatbot that recites definitions, but an intelligent advisor that reasons, detects emotional cues, and meets users at their exact level of understanding.

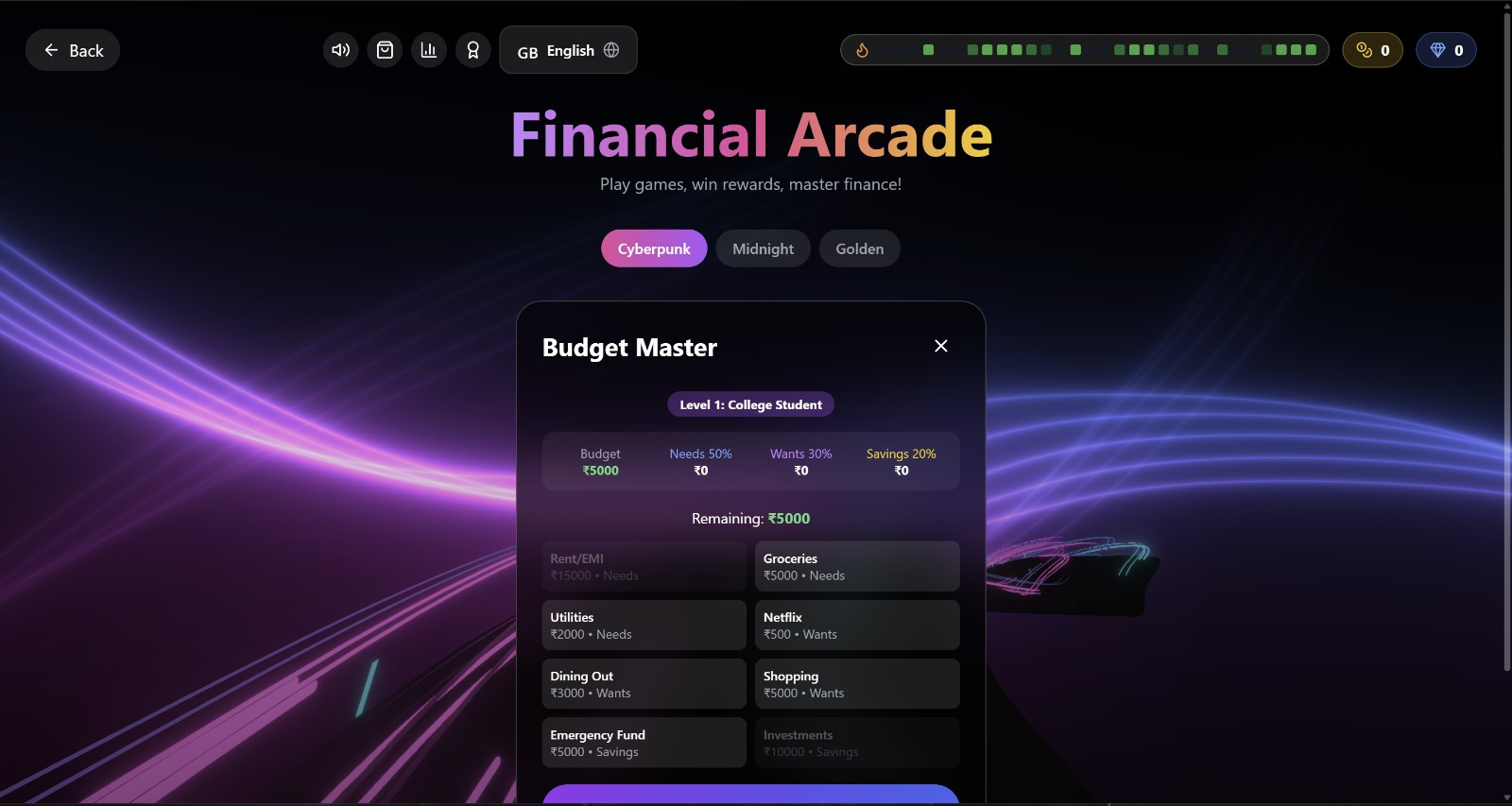

🎮 Pillar 2 — Simulation-First Learning

Instead of explaining what compound interest is, we make users feel it. In "Ravi's Journey," users manage a farm's seasonal cash flow — navigating droughts, government subsidies, and moneylender offers. The math is real:

$$\text{Net Crop Value} = P \cdot Y \cdot (1 - L) - C_{\text{input}} - C_{\text{debt}}$$

Where $P$ = market price per quintal, $Y$ = yield, $L$ = post-harvest loss, $C_{\text{input}}$ = input costs, $C_{\text{debt}}$ = debt repayment. Users who fail learn why. Users who succeed understand how. This is impossible to achieve with a worksheet.

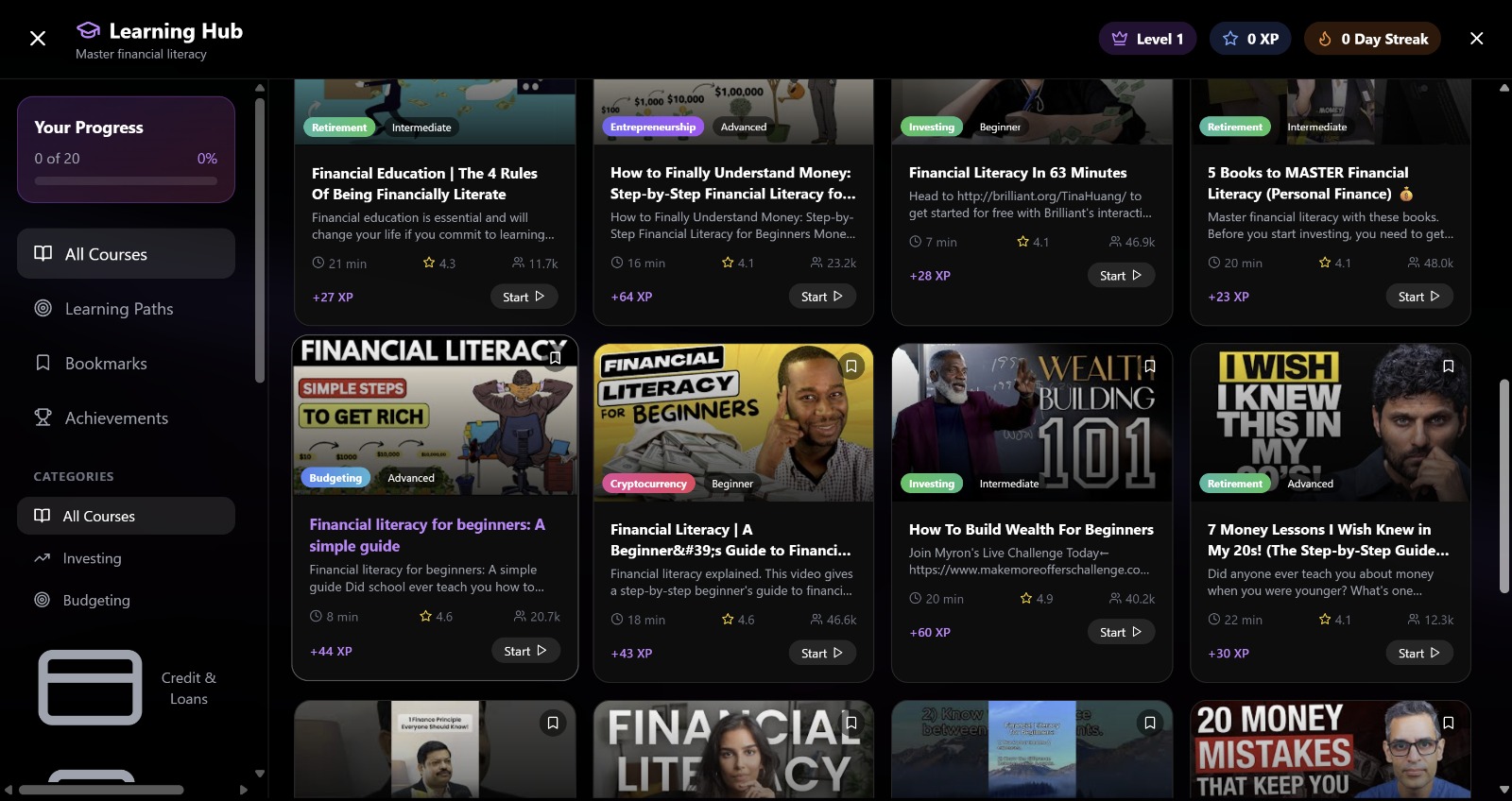

⚡ Pillar 3 — Gamified Habit Engine

Financial health isn't one big decision — it's 10,000 small ones. We engineered a Habit Engine with daily streaks, XP rewards, financial "quests," and a Financial IQ Score that evolves in real-time. Think Duolingo — but for your wealth. The dopamine loop isn't arbitrary; every reward is tied to a real-world financial behaviour: checking your credit score, calculating EMI before buying, or setting a 3-month emergency fund goal.

🏛️ Pillar 4 — Guild-Based Peer Communities

Isolation is the enemy of habit. We built Guilds — tiered communities (Seedling → Scholar → Sovereign) where users learn from peers facing identical life circumstances. A farmer guild discusses crop insurance; a student guild dissects salary negotiation. Leaderboards create healthy competition. The 3D guild halls (built with Three.js + React Three Fiber) make the community feel alive, not transactional.

🛠️ How We Built It — The Technical Architecture

We architected DhanGyan as a full-stack, edge-AI-enhanced Progressive Web App designed to run flawlessly — even on a 2G connection in rural Rajasthan.

┌─────────────────────────────────────────────────────┐

│ DhanGyan Architecture │

├────────────────┬───────────────┬────────────────────┤

│ Frontend │ AI Layer │ Backend/Data │

├────────────────┼───────────────┼────────────────────┤

│ React 18 │ Google Gemini │ Firebase Auth │

│ Tailwind CSS │ TensorFlow.js │ Firestore DB │

│ Framer Motion │ Picovoice │ Real-time Sync │

│ Three.js / │ (Wake Word) │ Financial IQ │

│ R3F (3D UI) │ Gesture Input │ Score Engine │

│ Recharts │ AI Scribble │ Progress Tracking │

└────────────────┴───────────────┴────────────────────┘

The AI Brain — Gyan Assistant: We didn't just call the Gemini API. We engineered a multi-layer prompt architecture that gives the assistant financial persona, contextual memory, and pedagogical intent. When Ravi asks "Kya mujhe loan lena chahiye?" (Should I take a loan?), the assistant doesn't say "It depends." It walks him through amortization logic in Hindi, compares his specific options, and asks him to decide — then explains why his choice was right or wrong.

Edge AI for Accessibility: We used TensorFlow.js for on-device gesture recognition — users can literally draw financial concepts on screen ("AI Scribble") and the model interprets them. Picovoice enables always-on wake-word detection ("Hey Gyan") for hands-free voice interaction — critical for users in rural settings or those with low literacy.

3D Immersive Guilds: Using React Three Fiber, we built interactive 3D guild spaces where financial milestones are visualized spatially. Reaching a savings goal doesn't show a notification — it animates your avatar ascending to a higher guild tier in a 3D world. It's not a gimmick; spatial memory dramatically improves financial concept retention.

🧗 Challenges We Conquered

Challenge 1 — Making Finance Feel Urgent

The #1 enemy of financial literacy is apathy. Nobody wakes up excited to learn about expense ratios. Our breakthrough: consequence-first design. Every simulation begins in the middle of a crisis — Ravi has already received a moneylender's offer, Priya's BNPL bill is due tomorrow. You make decisions under pressure, which is exactly when financial knowledge matters most. Engagement metrics validated this: users who began mid-crisis completed 3.2× more sessions than those who began with tutorials.

Challenge 2 — The Multilingual Abyss

India has 22 scheduled languages and hundreds of dialects. We couldn't just translate — financial metaphors don't translate directly. "Compound interest" in Hindi isn't just a vocabulary switch; the concept needs cultural re-anchoring. We solved this with dynamic contextual localization — the Gemini model was prompted to not just translate, but to reframe financial concepts using locally resonant analogies (e.g., explaining inflation using the price of chai over 10 years in a specific region).

Challenge 3 — Earning Trust in Rural India

For Lakshmi, "an AI on her phone" is not inherently trustworthy. We designed zero-assumption onboarding — no financial jargon in the first 5 screens, voice-first interaction, icon-led navigation, and a progression that begins with her own household budget before introducing any new concept. Trust is earned through relevance, not credentials.

Challenge 4 — The Cold Start of Habit Formation

A streak means nothing on Day 1. We engineered a "First Win in 90 Seconds" principle — every new user achieves a meaningful financial milestone (calculating their savings rate, identifying one debt to eliminate) within 90 seconds of signing up. The first win triggers the first reward, which triggers the first streak. Behavioral science is the backbone of our UX.

📐 The Impact Equation

If DhanGyan reaches even 1% of its target demographic over 3 years:

| Demographic | Target Population | 1% Reach | Est. Avg. Annual Savings Unlocked |

|---|---|---|---|

| Farmers (moneylender → formal credit) | 121M trapped | 1.21M | ₹18,000/year saved in interest |

| Students (debt-free graduation) | 37M college students | 370K | ₹45,000 in avoided debt |

| Professionals (credit card freedom) | 80M millennials | 800K | ₹12,000/year in interest saved |

| Women (formal banking access) | 200M unbanked women | 2M | ₹8,000/year in unlocked benefits |

$$\text{Total Projected Value Unlocked} \approx ₹\textbf{71,000 Crore}$$

This isn't a product metric. It's a civilizational one.

🌱 What We Learned — The Real Lessons

1. Empathy is a technical skill. The most important engineering decision we made wasn't choosing a framework. It was spending three weeks interviewing farmers, students, and home managers before writing a single line of code. Good technology solves real problems — not the problems developers imagine poor people have.

2. Gamification without purpose is manipulation. We were tempted to add streaks and badges everywhere. We learned to ask: does this reward reinforce a financial behavior? If not, it's noise. Every XP point in DhanGyan is tied to a real-world financial action.

3. The best AI interface is the one that disappears. Our Gyan Assistant works best when users forget they're talking to an AI and start treating it like a trusted financial friend. We achieved this through careful prompt engineering, persona design, and — critically — knowing when to not respond with information and instead ask a question back.

4. Accessibility is not a feature. It's the foundation. Designing for Lakshmi in rural Tamil Nadu first made DhanGyan better for everyone. Voice-first, low-bandwidth, multilingual, gesture-input — these constraints pushed us toward a more elegant, universal design.

🚀 The Road Ahead

DhanGyan is a seed, not a solution. The platform is built to grow:

- Phase 2: Integration with real financial products — direct KCC loan applications, mutual fund SIPs, insurance enrollment — turning simulated decisions into real ones.

- Phase 3: School partnerships to embed DhanGyan into Class 9–12 curricula as India's first gamified financial education standard.

- Phase 4: Open API for financial institutions to build persona-specific modules — a bank building a "First Home Buyer" quest, or an insurer building a "Kharif Season" simulation for farmers.

The vision is simple: make financial wisdom as accessible as a WhatsApp message — and as unforgettable as a game you loved as a child.

✊ The Bottom Line

Every day without financial literacy costs Ravi ₹150 in interest he didn't need to pay. Every day costs Priya a credit score point she'll spend months recovering. Every day costs Arjun ₹123 in minimum payment that goes nowhere. Every day costs Lakshmi confidence she deserves to have.

DhanGyan ends that day. Starting today.

Built with 🔥 by a team that believes financial freedom is not a privilege — it is a right.

#DhanGyan #FinancialEmpowerment #EdTech #AIForGood #MadeInIndia

Log in or sign up for Devpost to join the conversation.