-

-

Introduction

-

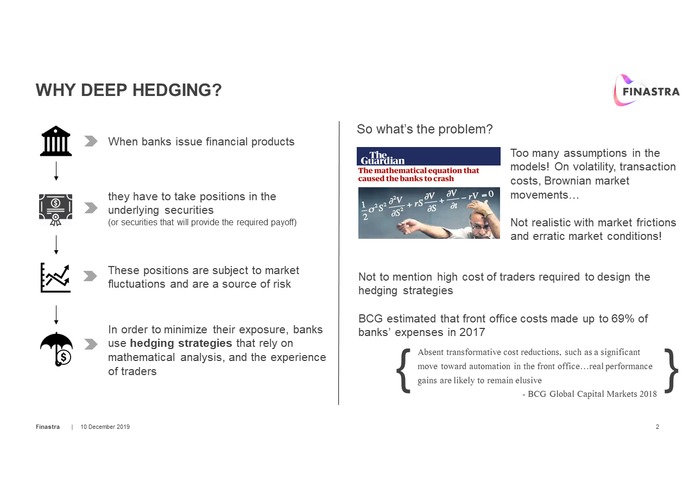

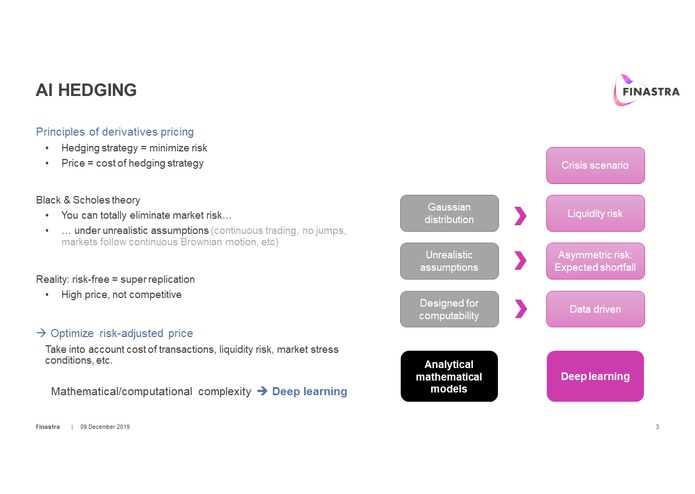

Problem statement

-

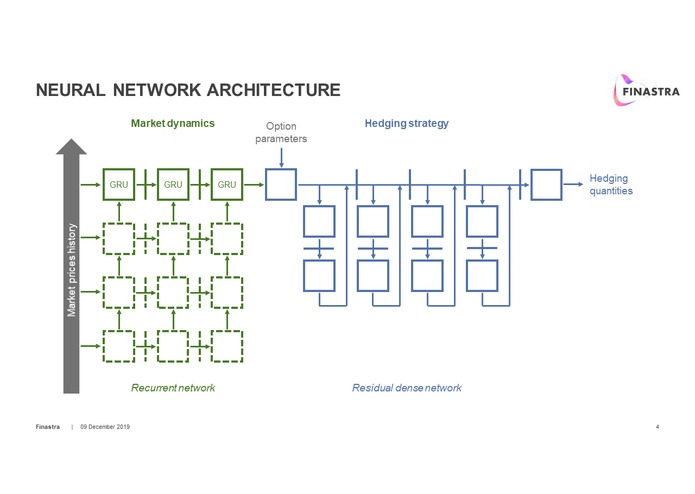

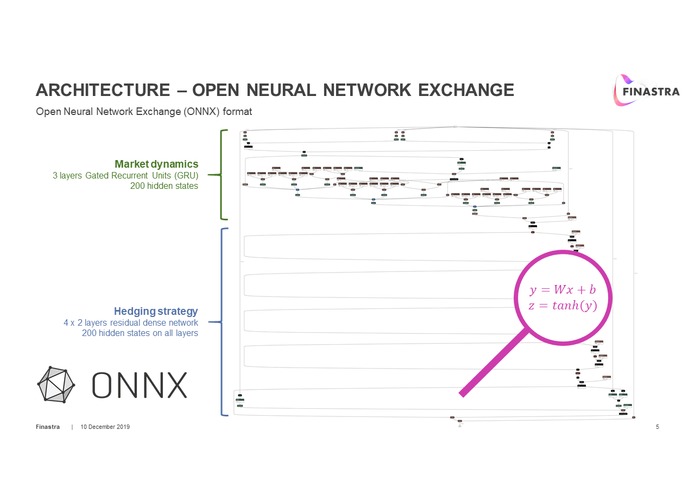

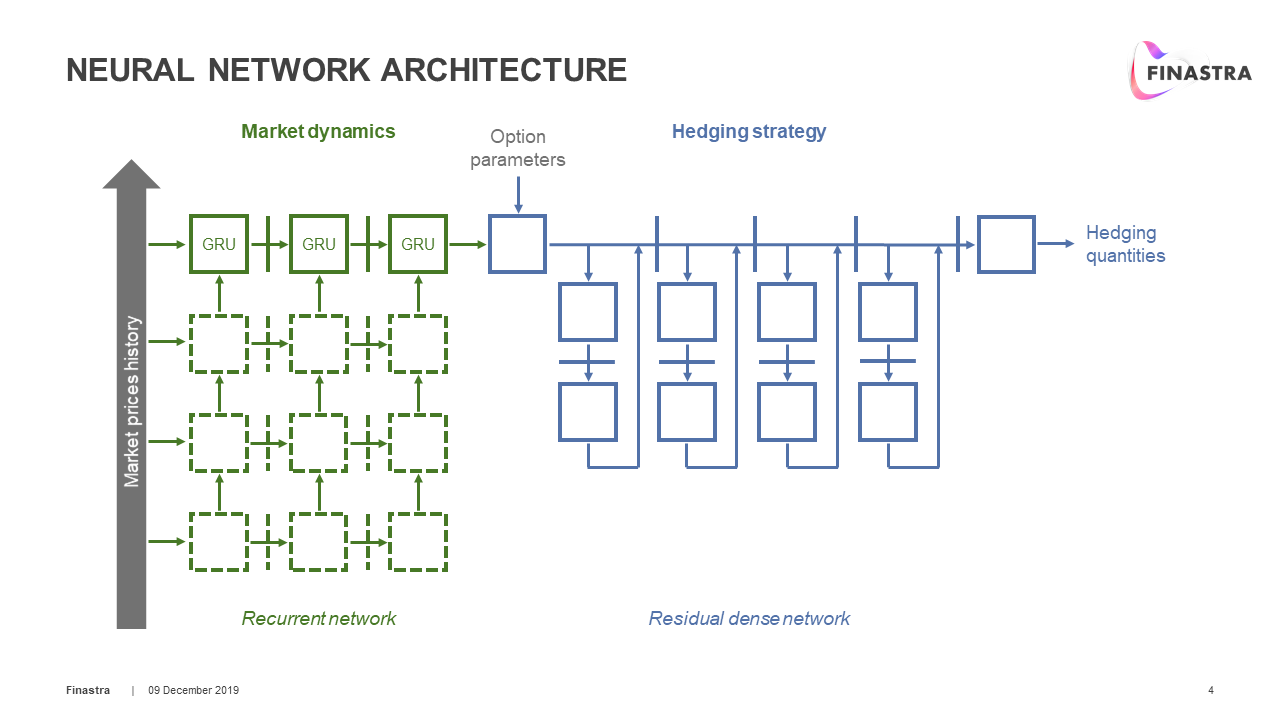

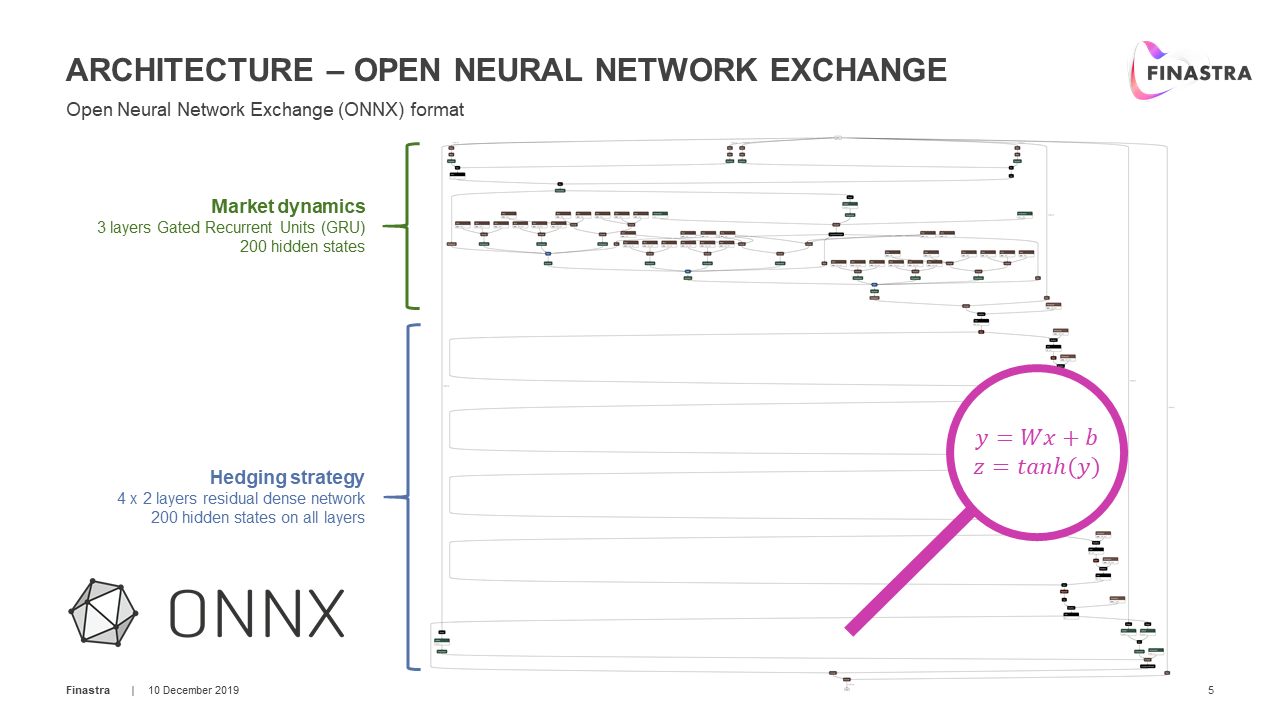

Neural network architecture - 1

-

Neural network architecture - 2

-

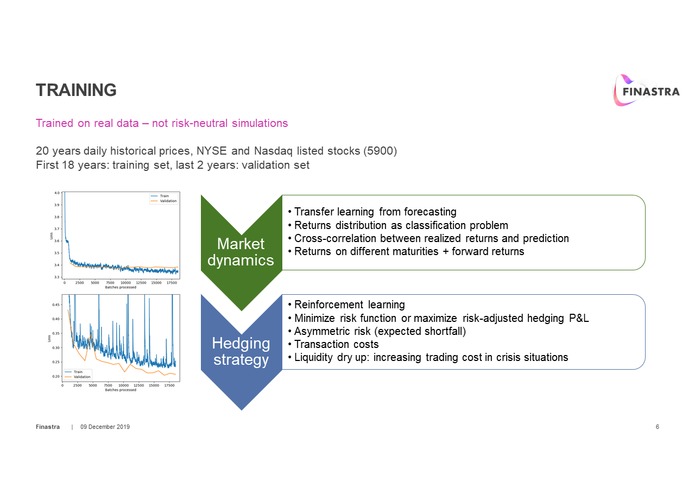

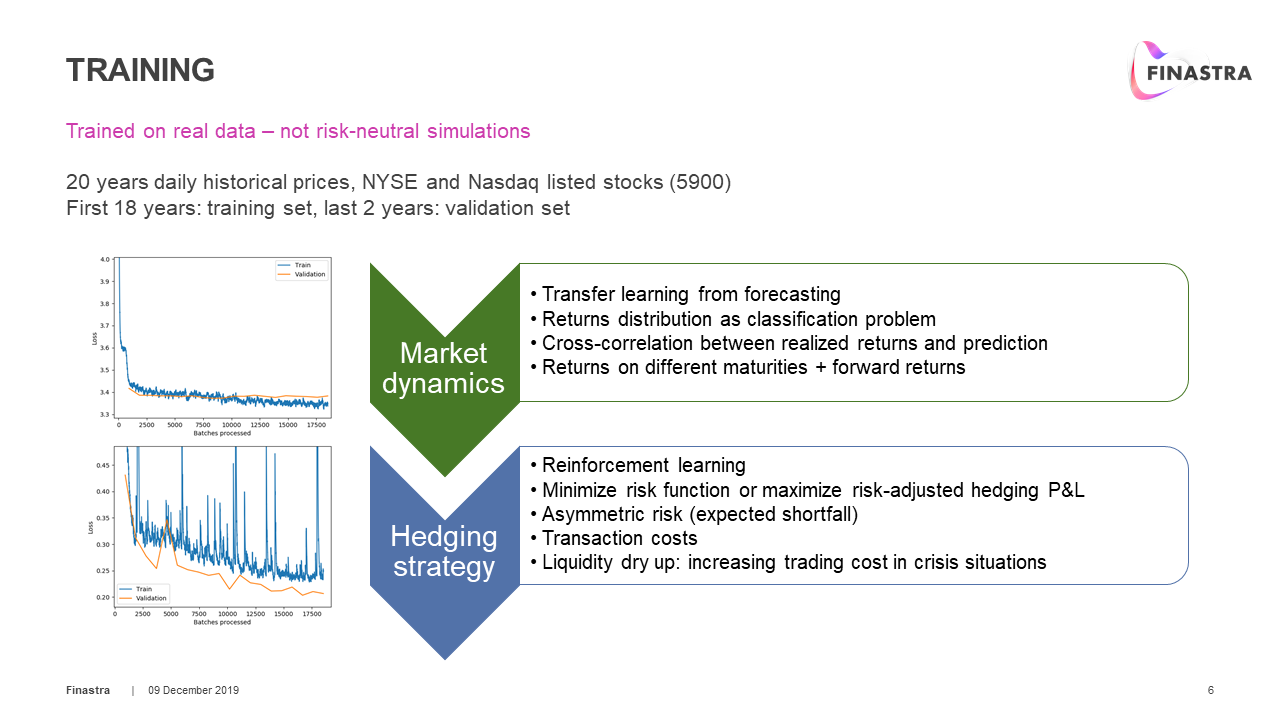

Training

-

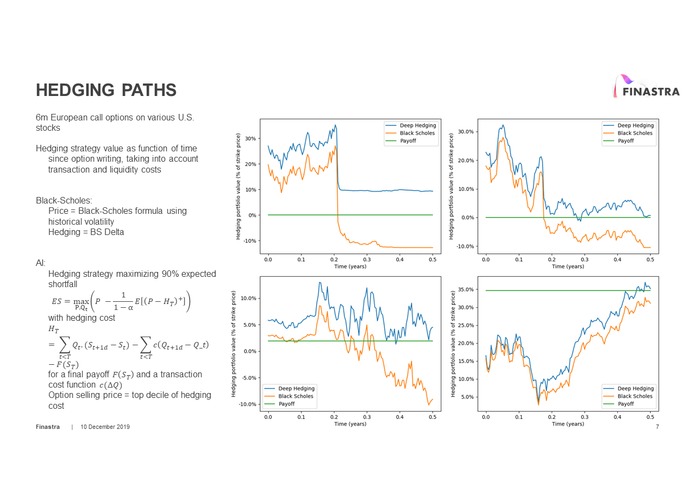

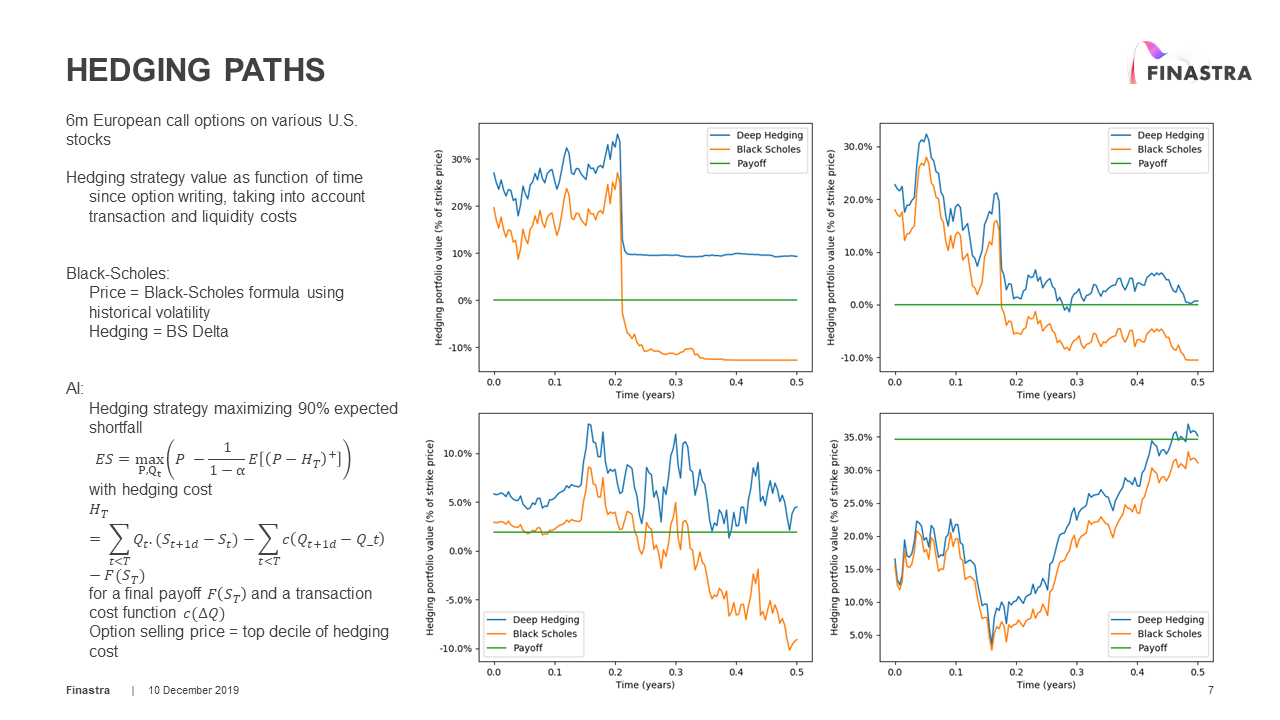

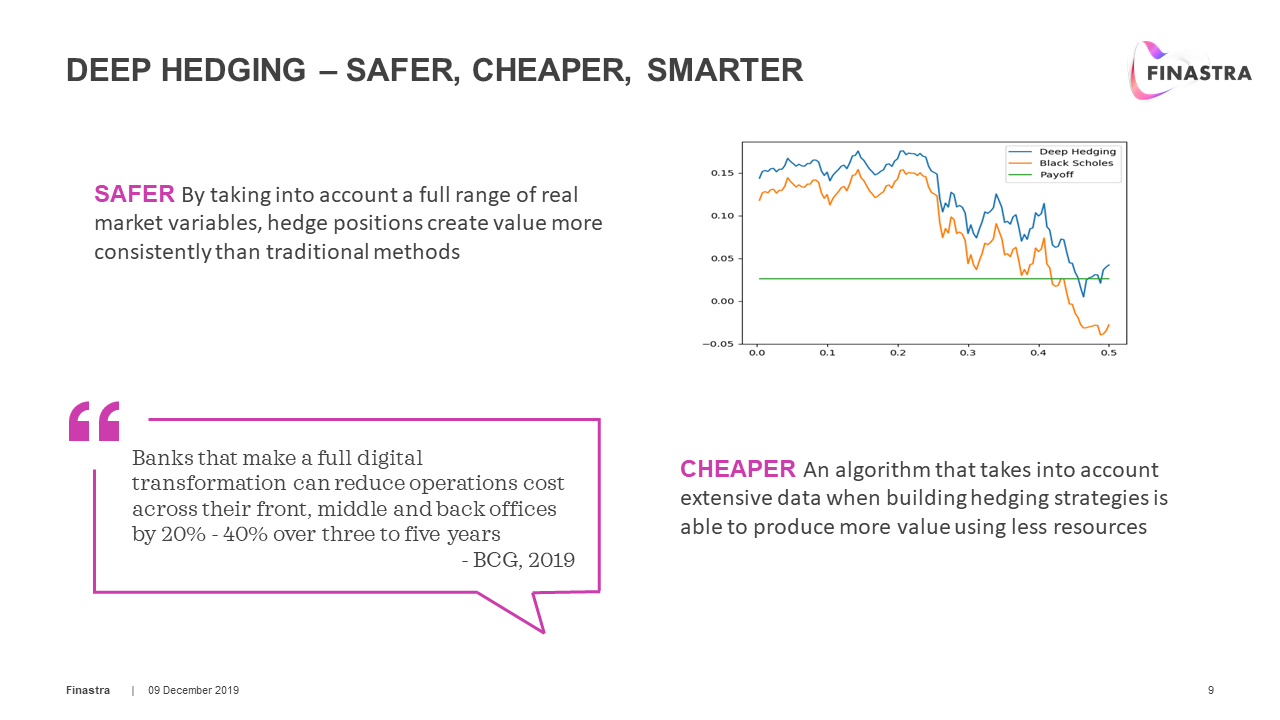

Hedging results

-

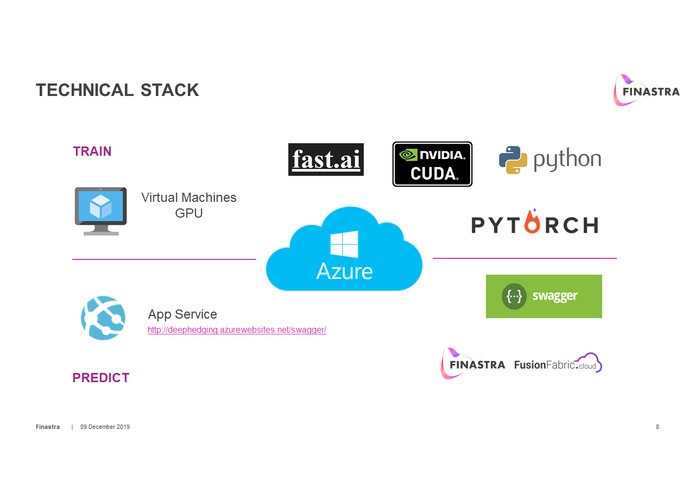

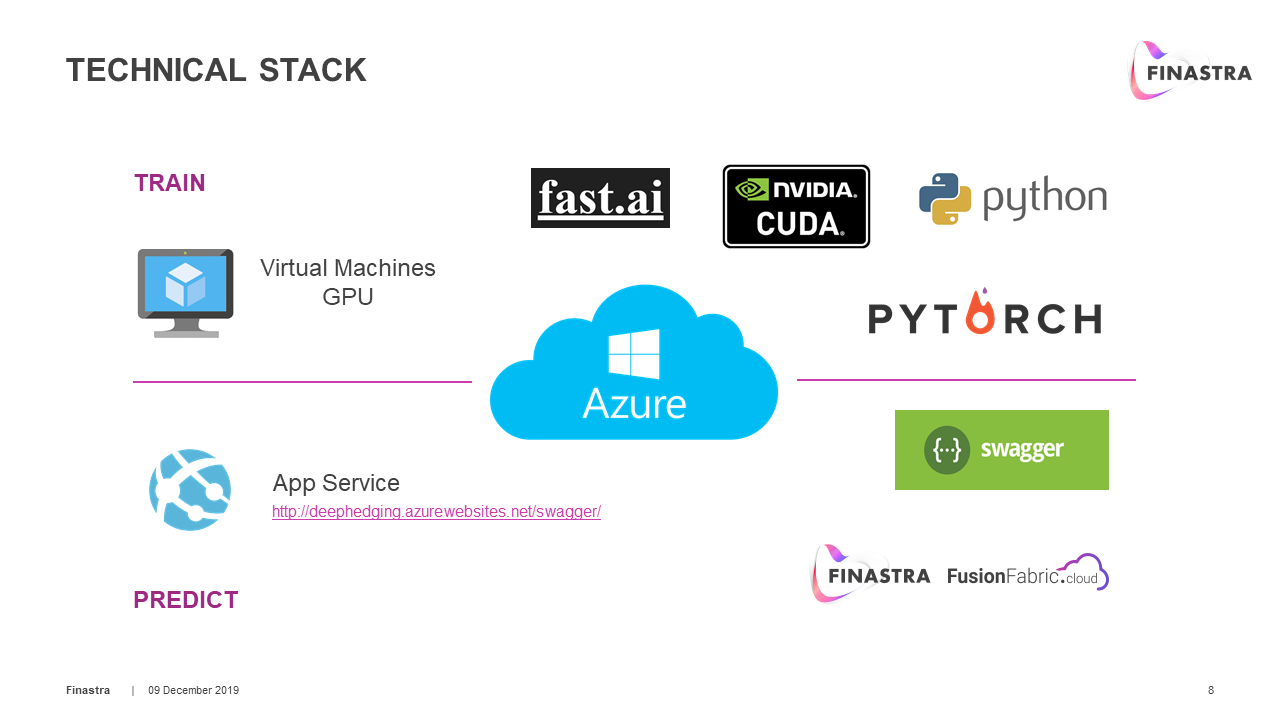

Technical stack

-

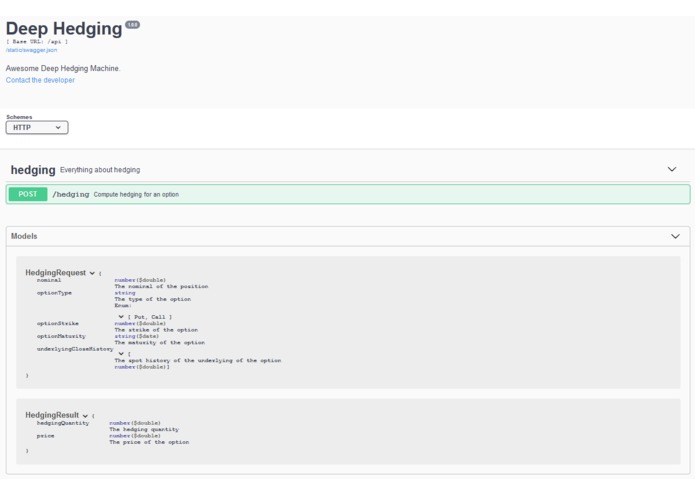

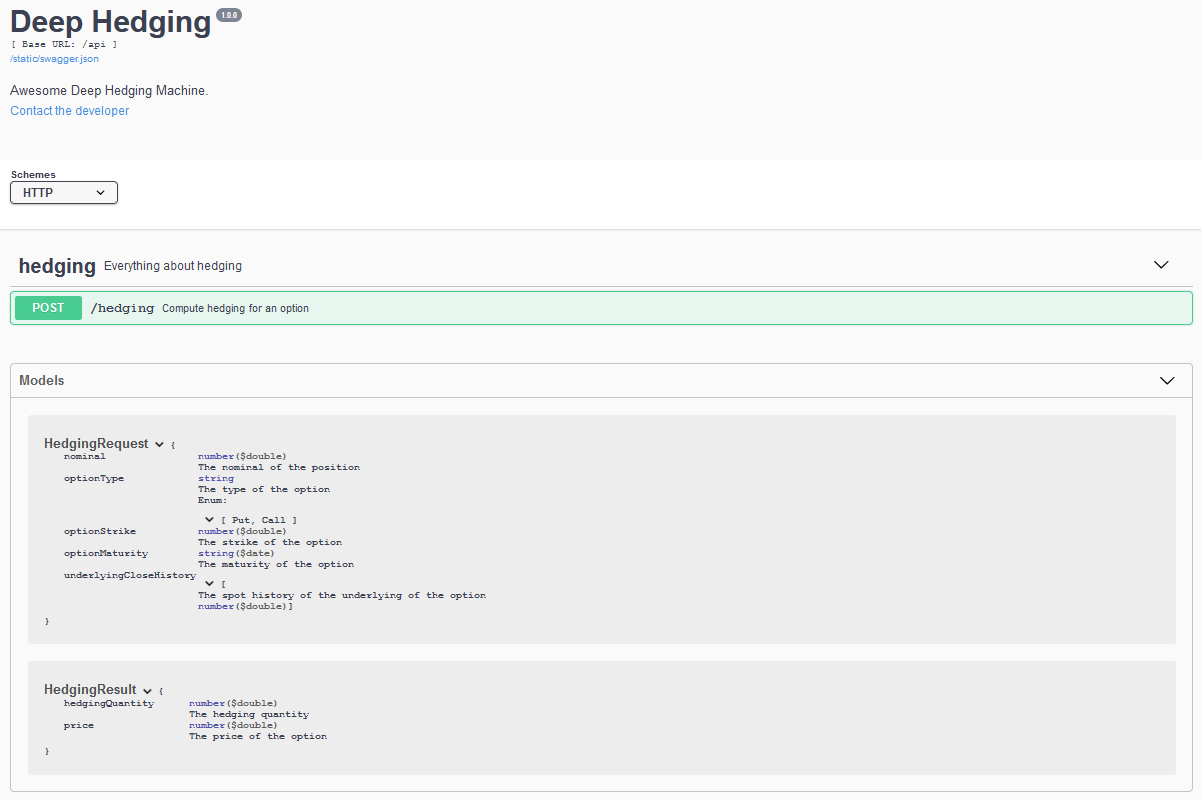

API

-

Conclusion

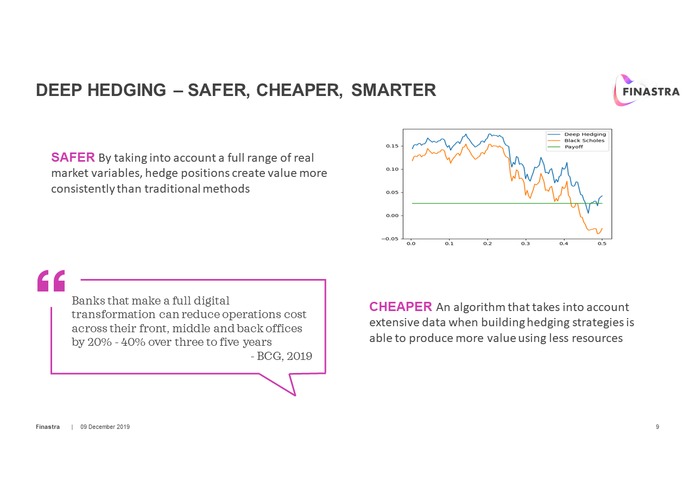

The objective of 'deep hedging' is to integrate a wide range of realistic market conditions in the designing of hedging strategies.

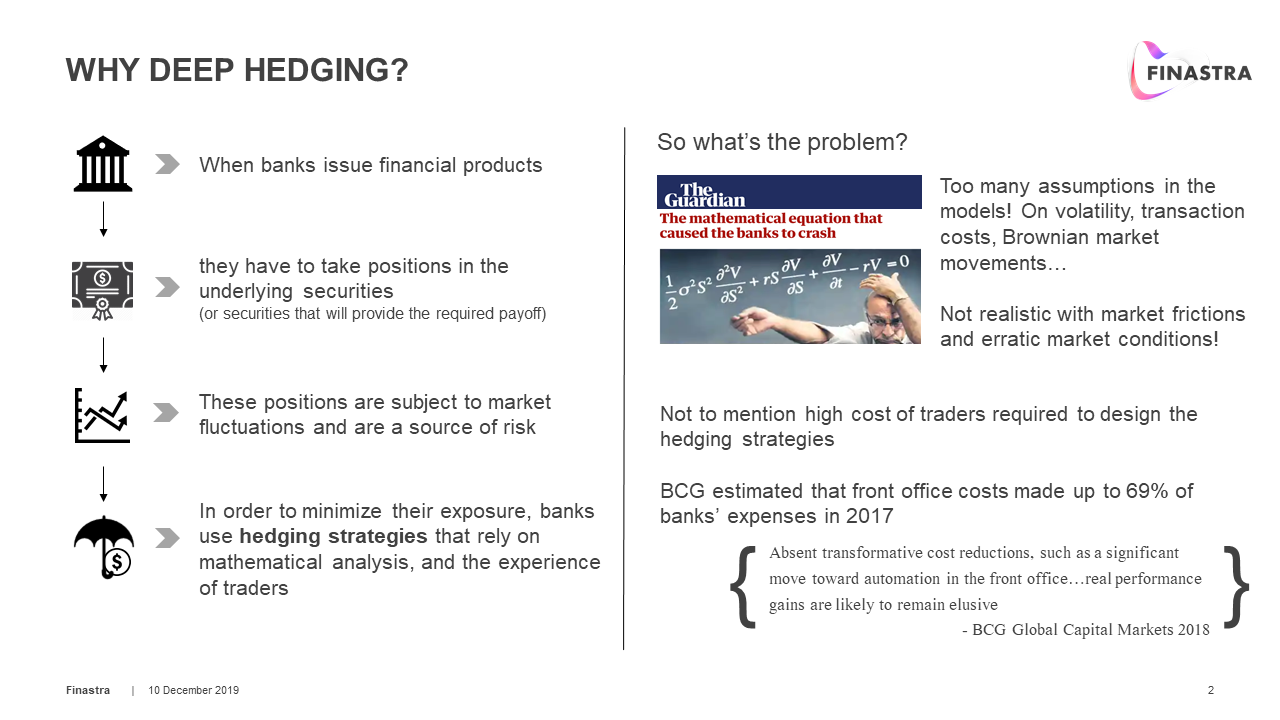

Banks rely on hedging strategies to cover their risk in the products they issue, thus making the business model safer. However, the traditional mathematical models used to design these strategies are limited in their ability to take into account multiple market frictions such as transaction costs and liquidity. Furthermore, the models tend to be over simplified, and are incapable of capturing erratic market conditions. The experience and skills of traders are still required in order to make judgement calls, but large teams of traders are not only expensive, they are also susceptible to costly mistakes in times of crisis.

Deep Hedging circumvents this issue by training the neural network with real market data. For the prototype, actual historical data of a wide range of stocks spanning almost 20 years were taken into account, allowing the neural network to gain more experience than any human traders. This enables it to not only take into account market frictions but also build safer hedging strategies especially in times of crisis, thanks to a model that is more robust to market shocks.

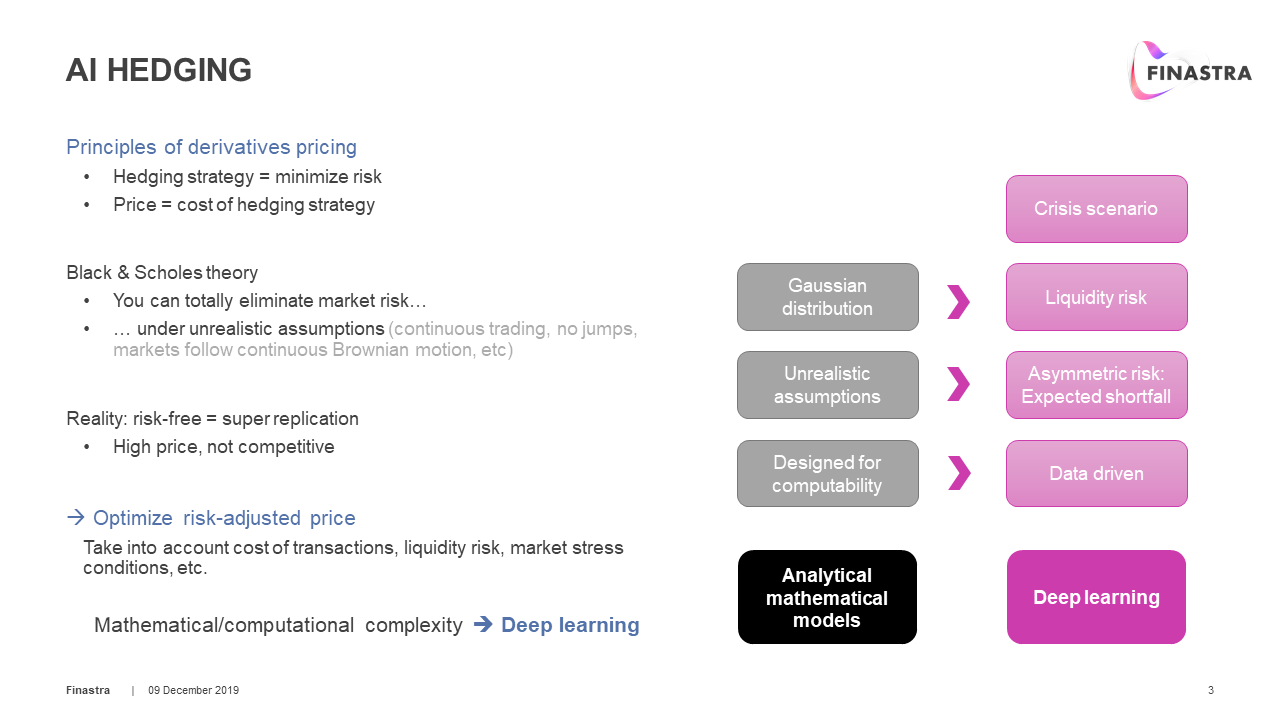

• The state is the bank portfolio (asset + hedge) as well as the stochastic diffusion of market data which can be learned from historical time series with statistical estimators. It allows full flexibility on the probability law used to model the market. In particular, it does not restrict to log-normal diffusion, which does not correctly capture the correct market movement and has been largely blamed for the miscalculation of the risk by the banks during the 2008 financial crisis.

• The reward function is the profit & loss of the bank (including the asset return, the hedge as well as all the transaction cost) adjusted by the capital cost of the risk as measured by the banking regulator (expected shortfall). It allows to reflect the profitability for the bank and its shareholder entirely. It is very different from the traditional Black & Sholes paradigm, which assume perfect hedging and therefore, risk-free cash flow discounting.

The neural network is trained on Azure Cloud and eventually, it will be made accessible via FusionFabric.cloud, making a strong addition to the portfolio of applications available on the platform.

Academic reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3355706

Log in or sign up for Devpost to join the conversation.