-

-

cover

-

App mobile A.I Customer Care

-

App mobile A.I Customer Care

-

App mobile A.I Customer Care

-

App mobile A.I Customer Care

Category

Professional Services Access

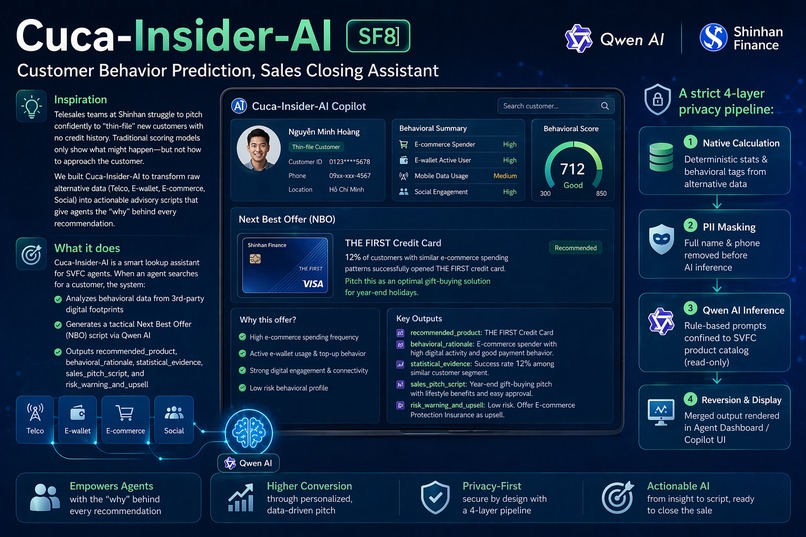

What you built (text description, 500-1000 words)

CUCA is an AI-native Relationship Operating System designed for sales professionals — real estate agents, insurance advisors, wealth managers — who manage 500 to 5,000 contacts but can only naturally maintain about 150 meaningful relationships (Dunbar's Number). Beyond that limit, trust decays, context is forgotten, and referral opportunities slip away.

The core insight: relationship management at scale is impossible for humans alone, but it's a perfect job for AI agents that never forget and never sleep.

How AI operates the business:

CUCA is not a CRM with AI features bolted on. AI agents run the core operations:

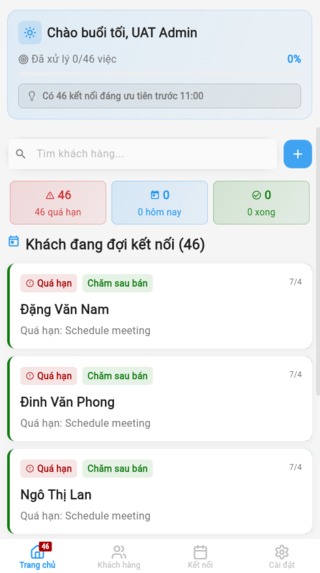

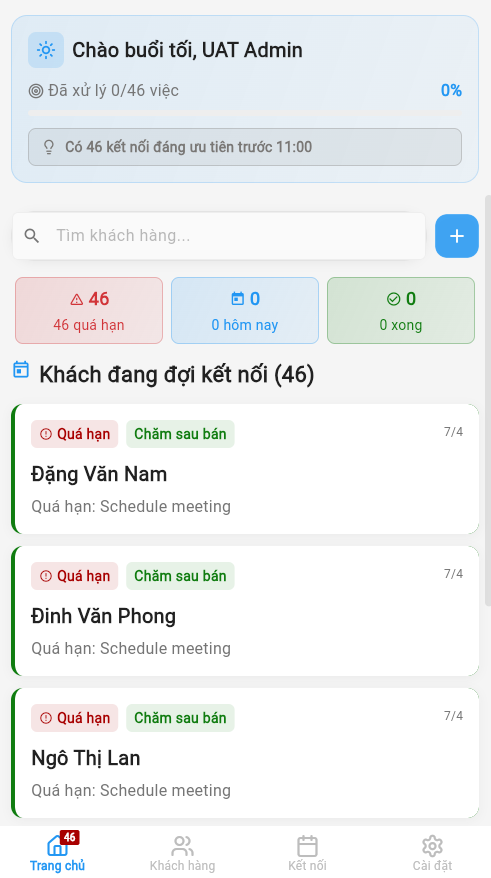

Morning Briefing Agent — Every day at 5AM, the AI scans all contacts, identifies the top 5 people who need attention today, and delivers a personalized briefing: who, why now, and what to say. The AI decides priority, not the user.

Ghost Writer Agent — Overnight, the AI drafts 2-3 personalized message options for each contact on today's list. It uses the full relationship context — past interactions, notes, family details, opportunities — to generate sincere, non-generic messages. The user reviews and approves; the AI does the creative work.

Retention Agent — The AI continuously monitors interaction gaps at 30/60/90-day thresholds. When a relationship is going cold, it sends a pulse alert with a suggested re-engagement message. The AI proactively prevents relationship decay before the user even notices.

3-Second Capture Agent — When a user inputs free text ("Met Hung from Vinhomes. Daughter in grade 3. Looking for a villa."), the AI extracts structured data automatically — name, organization, family context, opportunity signals. Zero-friction input.

Technical architecture:

- Frontend: Flutter (mobile + web), Riverpod, Clean Architecture

- Backend: Node.js, Fastify, TypeScript

- Database: Supabase (PostgreSQL) with Row Level Security

- AI Layer: Model-agnostic provider registry with Gemini as primary provider (satisfying XPRIZE requirement), plus Z.AI as fallback. Business logic never depends on a specific LLM.

- Google Cloud: Google Cloud Storage for file attachments and data exports; Gemini API for all LLM operations

What existed before the hackathon:

The core CRM/relationship management functionality (contact storage, interaction logging, basic reminders) was built before May 19, 2026. During the 90-day XPRIZE window, we built:

- The AI Agent system (Morning Briefing, Ghost Writer, Retention Agent)

- Gemini API integration as the primary LLM provider

- Google Cloud Storage integration

- The payment and subscription system (pricing tiers, VNPay/Momo, invoicing)

- The Referral Graph feature

- Agent execution logging infrastructure

- The entire go-to-market execution (real paying customers, real revenue)

Real business, real revenue:

CUCA serves sales professionals in Vietnam, starting with real estate agents. We have paying customers on Starter (79,000 VND/month), Pro (199,000 VND/month), and Lifetime V1 (1,500,000 VND one-time) plans. Revenue is traceable through bank transfers and payment gateway records.

Category impact — Professional Services Access:

Sales professionals in emerging markets like Vietnam lack affordable tools to deliver high-quality professional services at scale. CUCA bridges the gap: instead of forgetting client details and missing follow-ups, every sales professional now has an AI relationship strategist that ensures no connection fades and every interaction is sincere and contextual. This redefines how relationship-based professional services operate — from memory-dependent to AI-assisted.

Log in or sign up for Devpost to join the conversation.