-

-

Unbanked

-

EU Initiatives

-

Solution Instruments

-

Digital Identity

-

MSME Open Banking Solution

-

Blockchain Lending Marketplace

-

Achievements

-

Next Plans

The problem your project solves

Cosmo solves the challenges of individuals and businesses towards access towards financial inclusion. However, we also understood that financial inclusion depends on several factors, which need to come together in sync for everything to work seamlessly.

Following are some of the challenges business and individuals are facing:

1.7 billion adults – are still unbanked Findex Data

About half of unbanked people include women poor households in rural areas or out of the workforce. Many more are at risk of losing their jobs because of the Covid epidemic, which has forced everyone to follow distancing and reduce physical interactions

EU Financial Inclusion Initiatives For example, consider the EU Initiatives for Financial Inclusion, which are focused towards helping Micro-Small-Medium Enterprises which provide significant contribution to GDP and job creation across the entire EU, in particular the southern Mediterranean region of the Middle East and North Africa.

Access to finance is the key pillar of EU strategy for private sector development in the region with 6 million micro, small and medium-sized enterprises in the region (MSMEs) with large potential for economic expansion and for job creation;

However, most MSMEs do not have access to funding in a timely manner from local banks, a factor that significantly limits their growth.

Access to finance for MSMEs by local banks, limited for different reasons, e.g. in Palestine 6% of total lending, in Egypt 7-8 %, in Jordan 11%, in Tunisia 15%, in Lebanon 16% and 25% in Morocco

Supply and demand side measures needed to facilitate access to finance, focus on financial inclusion

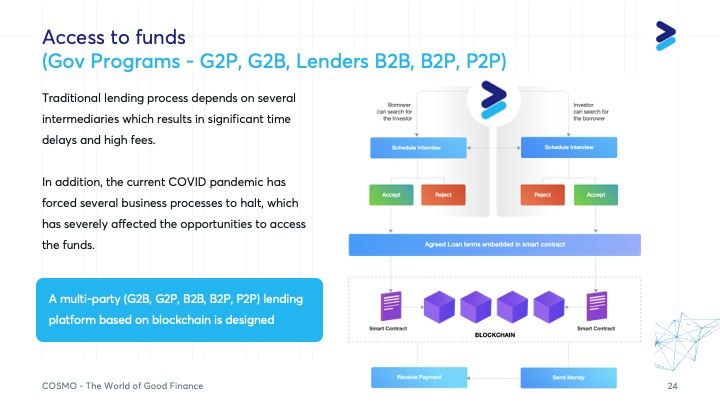

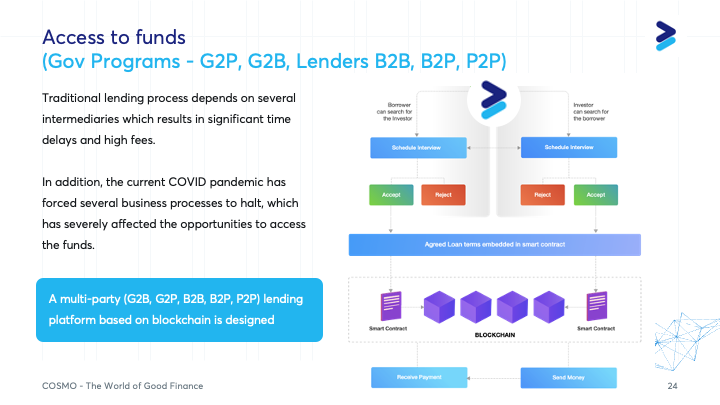

Access to funds from the Gov Programs, G2P and other institutional Lenders B2B, B2P, P2P)

Traditional lending process depends on several intermediaries like a loan officer, banks, underwriter, and loan processors to manage the screening, qualification and distribution of funds to those who are in need. This addition of middlemen and additional steps to the process of lending results in significant time delays and high fees.

Also, applying for a loan or credit can take a couple of weeks, and the rate of interests differ widely. For example, the rate of interest for lending money in different countries can vary widely.

In addition to this, the current COVID pandemic has forced several processes to halt, and institutions including financial services (banks, non banking companies and others) to stop working, to maintain lockdown guidelines and distancing. This has severely affected the opportunities to access the funds.

Lack of Digital Identity in a Digital First World

The World Bank estimates that roughly one billion people lack an official foundational identification.

These one billion people are unable to prove their identity (ID), and millions more have forms of identification that cannot be reliably verified or authenticated, resulting in exclusion from economic opportunities – such as those being created by the emerging digital economy – as well as social and political rights.

The World Bank’s 2017 Global Findex Survey found that the lack of documentation was a critical barrier to accessing financial services, cited by 26 percent of unbanked people in low-income countries.

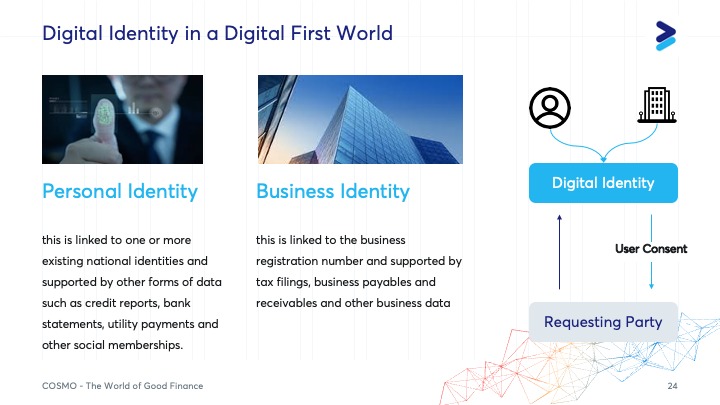

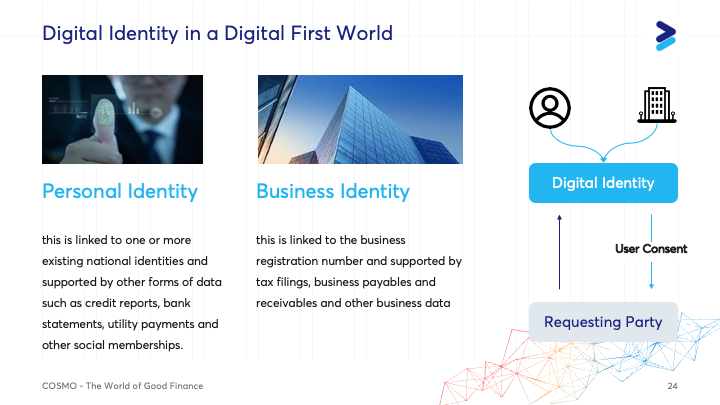

Personal Identity data has been well understood in the recent years, however, the concept of business identity is less understood and used.

The approach creates a digital identity for an entity (person, business) which can be easily shared - without exposing additional information.

Personal Identity – this is linked to one or more existing national identities and supported by other forms of data such as credit reports, bank statements, utility payments and other social memberships.

Business Identity – this is linked to the business registration number and supported by tax filings, business payables and receivables and other data

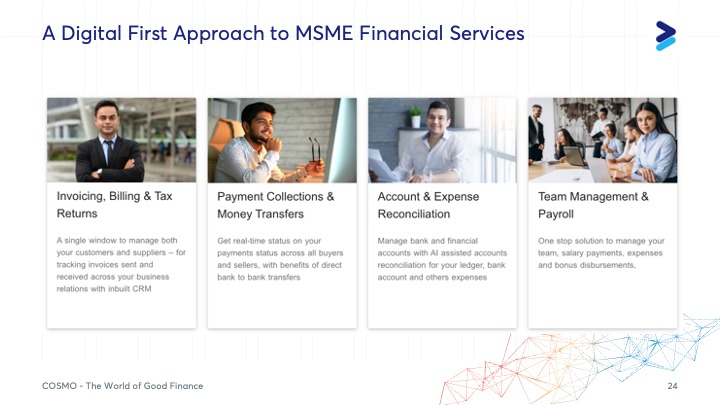

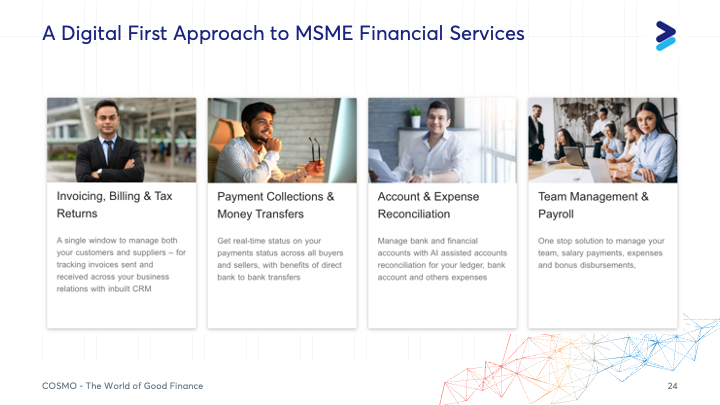

Disintegrated Business Solutions to Manage Business Financial Activity

Businesses have to navigate multiple applications for financial tasks.

A single business has to handle multiple types of business transactions. These include

- Payment Collection from Customers

- Payment Remittance to Suppliers

- Salary and Bonus Payments

- Utility Payments

- Managing expenses

- Account transaction tasks via Banking Portal

All of this leads to a significant loss of time and resources. At the same time this does not provide real-time visibility into the financial status of the business with respect to collection and payment delays.

The solution you bring to the table

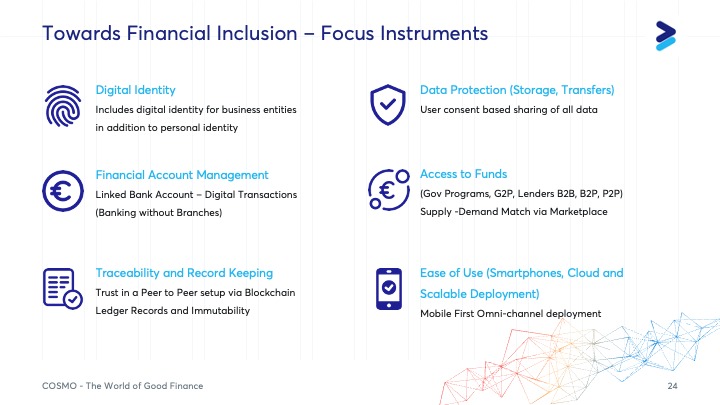

The solution is composed of three interlinked applications, which focus on the following instruments -

- Digital Identity and Data Protection

Account Management (Open Banking)

Access to Funds enabled via a Blockchain Marketplace Cosmo brings together Lenders and Borrowers on a common page. This creates an open market where Lenders can create opportunities or financing the requirements and needs of borrowers. They can provide finance at different terms and risk appetite.

Borrowers can choose from various available funding options and select the one which is prefereable to them for their requirements, interest payment abilities and duration.

What you have done during the weekend

The project is built with Blockchain as a key technology, where Lenders and Borrowers engage in financial transactions via use of Smart Contracts. This ensures that such a system can function without interference, in a distributed manner and with low chances of fraud.

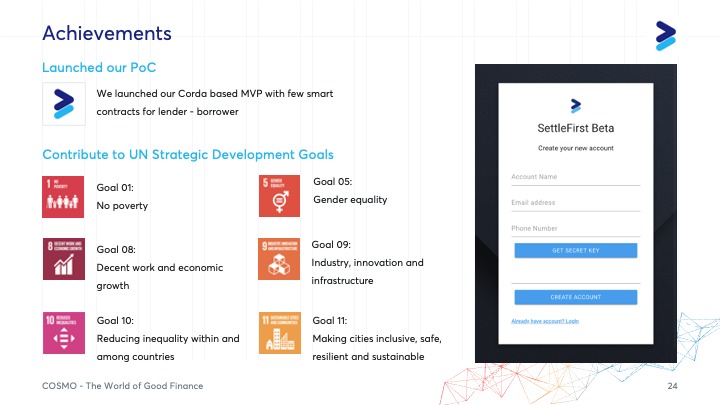

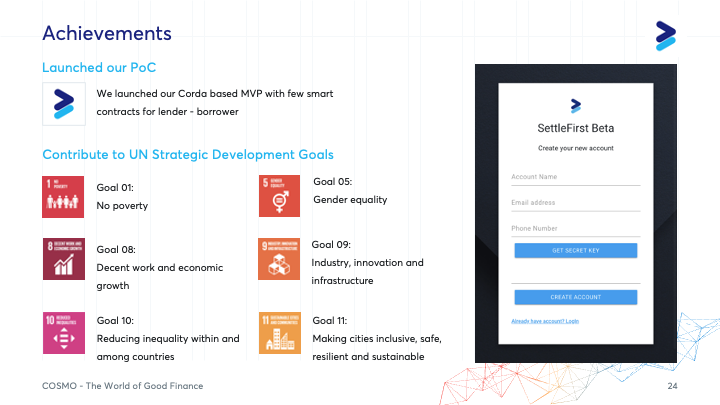

- Built and deployed our first blockchain solution using R3 Corda

- Review of UN Strategic Development Goals

- Review of EU Financial Inclusion Initiatves

- Mentor Discussions, Deedback and advise

The solution's impact to the crisis

The solution has a great potential impact on the crisis, especially in a situation where we are forced to maintain distance and work remotely. The use of diigital technologies acts as an enabler and provides opportunities to those who did not have it earlier.

With Digital ID and smartphones, they can access several programs very easily, manage their financial accounts remotely, complete transactions and participate in the marketplace to get access to funds.

It keeps the money in flow and hence removes several challenges for those who are not yet part of the formal banking system, as well as those who are at risk of losing jobs and are unable to work.

The necessities in order to continue the project

To continue with the project, we will need to increase our team and build technical and industry partners. A key component is to partner with a banking services provider to enable fund transfers and settlements. Partnership with a banking service / financial service provider for Fund Transfer APIs, KYC Checks, Credit Worthiness, Analytics for Risk Intelligence

Next we will need to raise some funds to be able to meet or costs of development, team and technology deployment.

We also need regulatory and legal support for maintaining regional compliance.

The value of your solution(s) after the crisis

The solution lives beyond the current crisis and in support to implement the UN Strategic Development Goals.

Goal 01: No poverty

Goal 05: Gender equality

Goal 08: Decent work and economic growth

Goal 09: Industry, innovation and infrastructure

Goal 10: Reducing inequality within and among countries

Goal 11: Making cities inclusive, safe, resilient and sustainable

Demo Video

Contact

Saurav Raaj, email: saurav.raaj@gmail.com

Log in or sign up for Devpost to join the conversation.