-

-

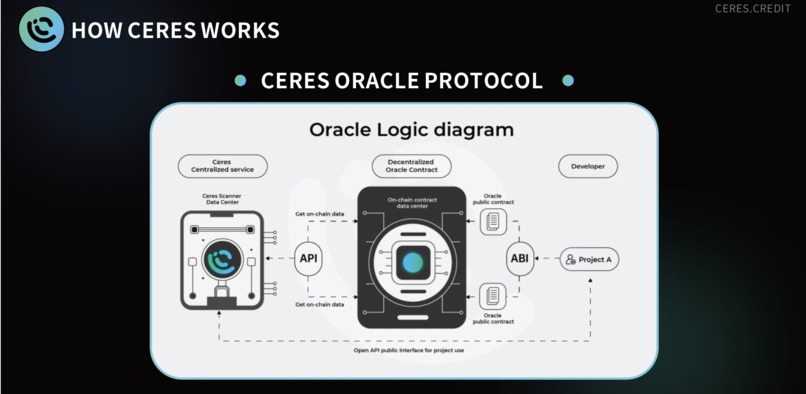

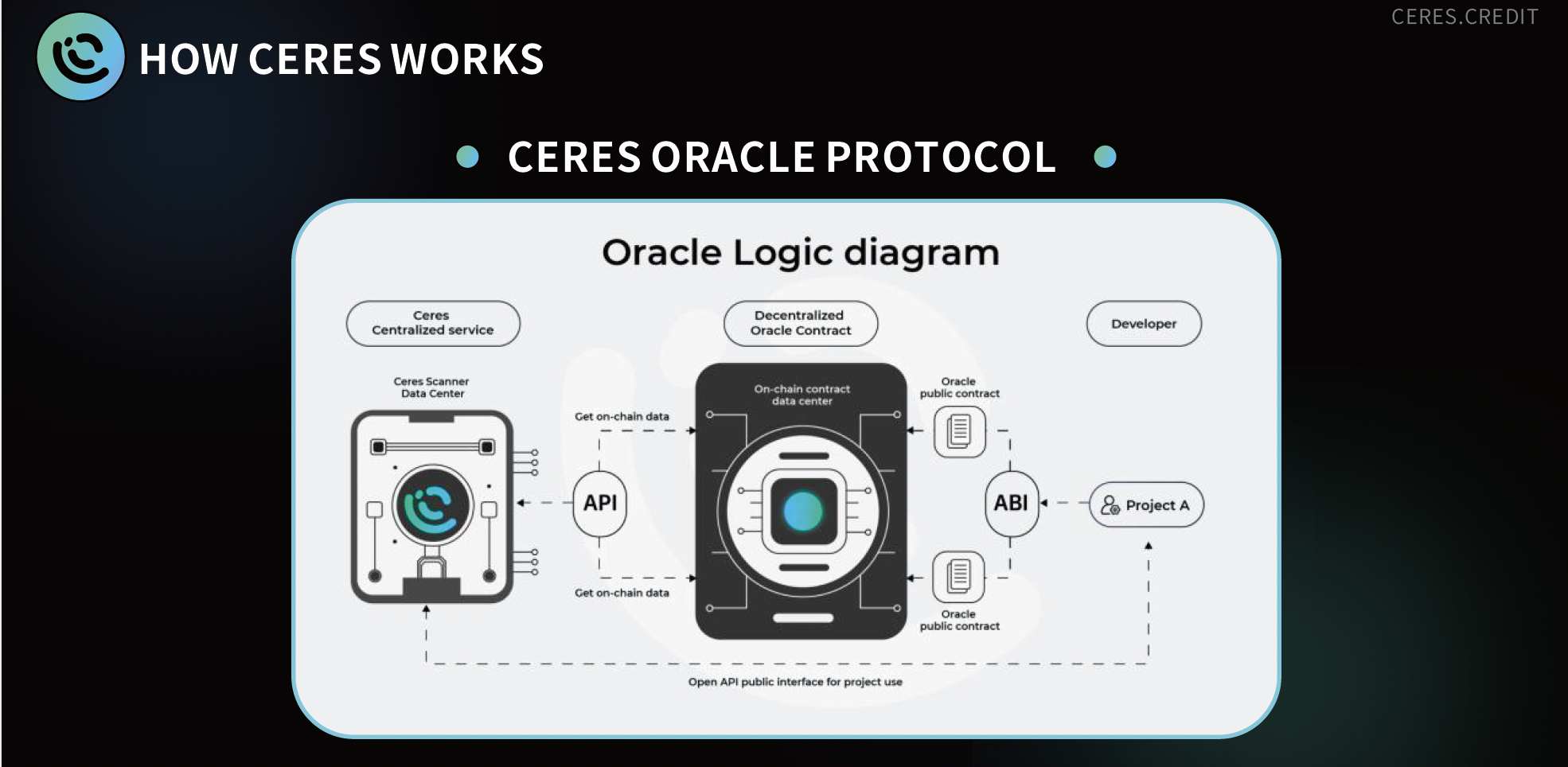

How Ceres Works - Oracle Protocol

-

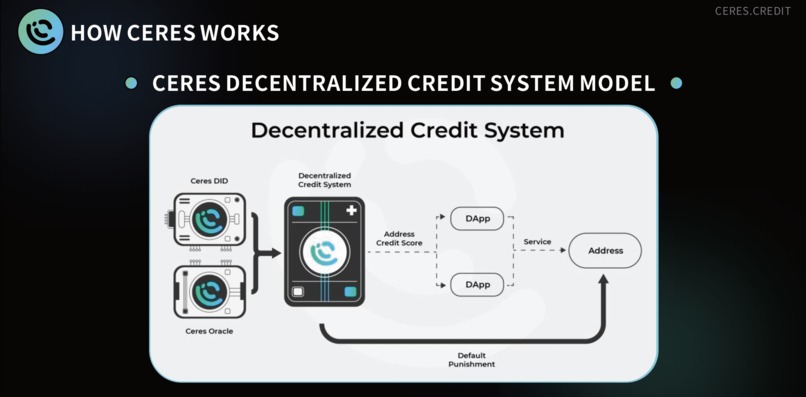

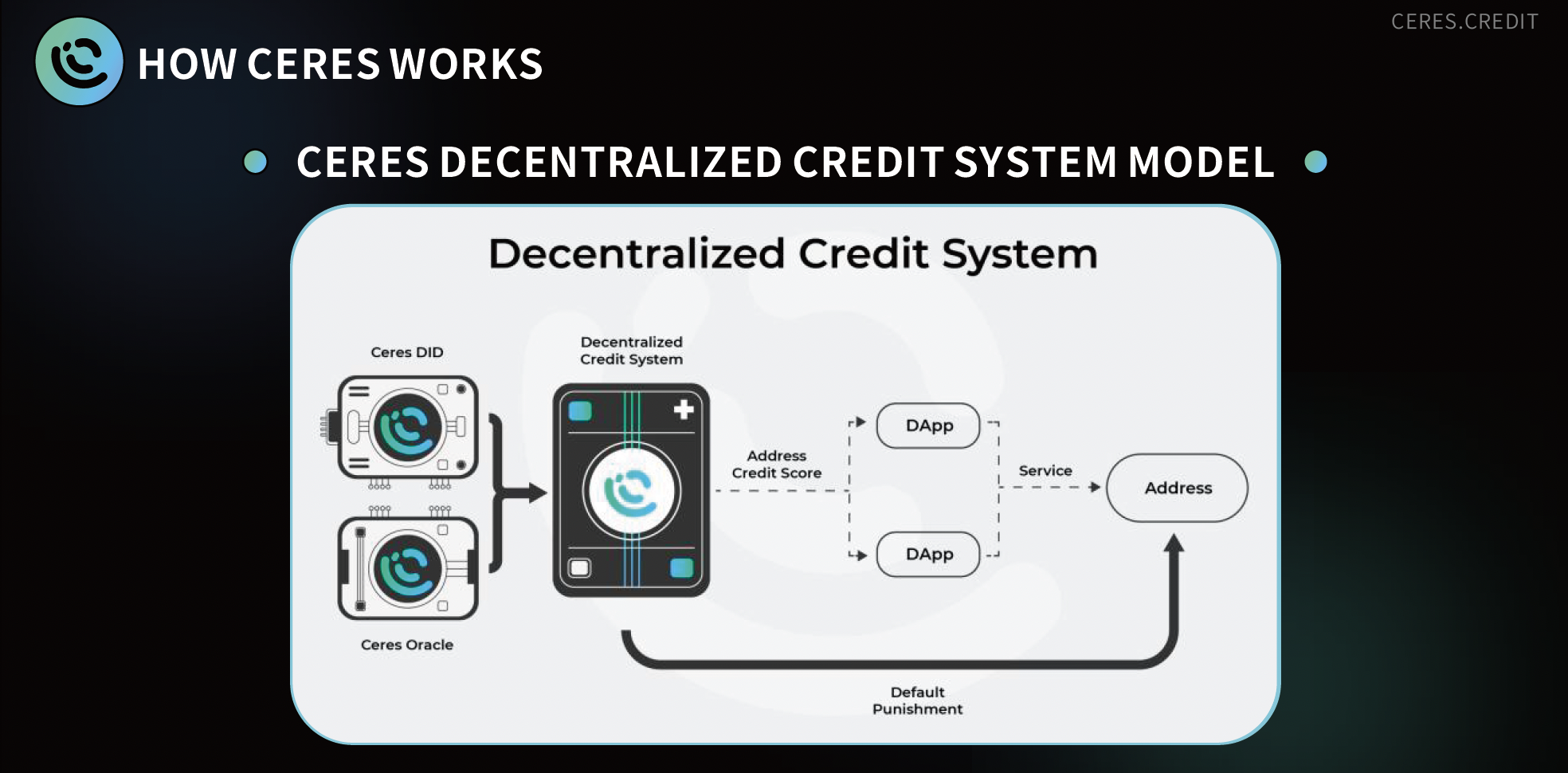

How Ceres Works - Decentralized Credit System Model

-

Ceres banner

Inspiration

I and my partner both come from traditional and FinTech industries. I entered the blockchain industry in 2015, and worked in and developed several DeFi and SocialFi projects before Ceres, which we develop since April this year. In these years’ experiences, we found out that blockchain has only collateralized lending and no credit lending, which makes the blockchain financial market very imperfect. Therefore, about May last year, we started to think and plan how to develop an on-chain credit loaning system base on a more comprehensive and accurate decentralized credit system.

What it does

Ceres, the infrastructure of the Decentralized Credit System (DCS). Ceres aims to construct the cornerstone of the future Web3 DeSoc (Decentralized Society) through a more comprehensive and fully open-source DCS.

How we built it

The core of Ceres is its Oracle Protocol. The Oracle Protocol is specifically designed to allow users/DApps/developers to write in their (including their users/ fans) on-chain social address networks, which may be authorized to other addresses, and through this authorization, we can bind them together in the Oracle Protocol, thus creating a decentralized address network. When these addresses participate in certain DApps/DAOs/communities Ceres works with, those addresses would be incentivized to enable user fission. And incentives are distributed through the smart contracts in Ceres Oracle Protocol, which is fully decentralized, transparent, and censorship-resistant. In doing so, we can track and analyze the controllable financial/interaction on-chain behavior of these addresses.

Based on the characteristics of blockchain, it is very difficult to change your on-chain social relationship/ networks, and if you change your address, it is equivalent to your social data being gone. When you have an on-chain social relationship with certain addresses, have an invitation relationship, or have a binding network, you can actually use Ceres’ smart contracts to record them, which can make you leverage your data to liquidate and monetize.

Let’s say if one of the addresses, Ceres might grant it credit in the future. In case the address defaults or triggers a risk, Ceres can hedge credit risk by managing the benefits to the address which is estimated and generated from its entire on-chain social network.

Challenges we ran into

We found that in the blockchain world you can hardly apply traditional finance to it because the data of each address, the transaction records of each address, and the on-chain assets of each address do not represent users’ future cash flow. We understand very clearly that if you want to do the decentralized credit loaning, unlock and monetize one’s on-chain influence and data, must tackle the bottleneck of constructing a brand new system and algorithm to estimate and measure users’ on-chain discounted cash flow. DID system as a potential credit scoring solution, the infrastructure of it is slow to advance, still cannot solve the bottleneck in the development of the on‑chain credit market, i.e., the problem of large-scale

Accomplishments that we're proud of

Ceres now has 250,000 users already, since we launched Oracle Protocol V1 in April 2022.

What's next for Ceres

We plan to reach 2,000,000 users by Q2 2023. We will launch the credit model then.

Built With

- aliyun?aws

- bnbchain

- distributed-system

- ethereum

- graphql

- heco

- mysql?elasticsearch

- optimism

- solidity?javascript?html?java?assemblyscript

- spring-boot

- spring-cloud

- vue

- web3.js?ethers.js?nginx?ecdsa

- zksync

Log in or sign up for Devpost to join the conversation.