-

-

OVERVIEW

-

WORK FLOW

-

PROBLEM STATEMENT

-

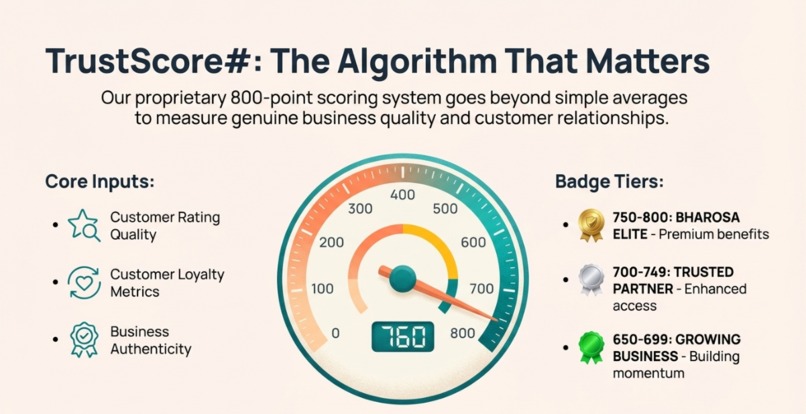

TRUST SCORE

-

TRUST POINTS

-

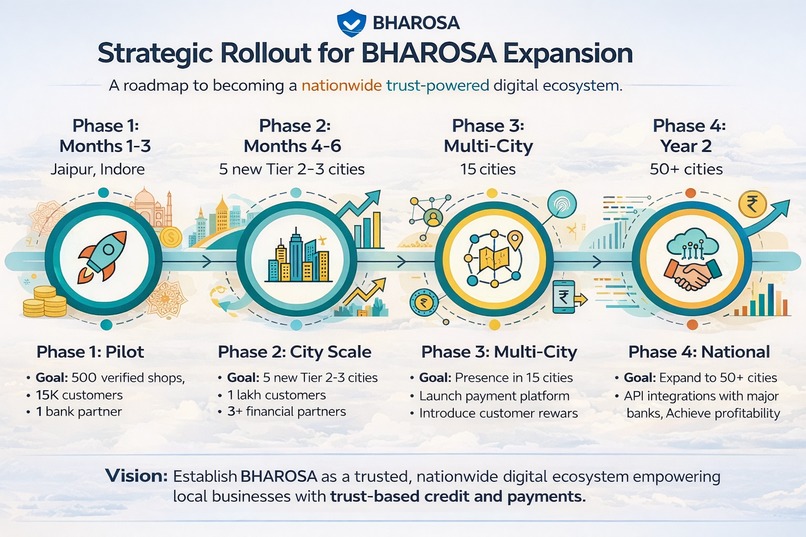

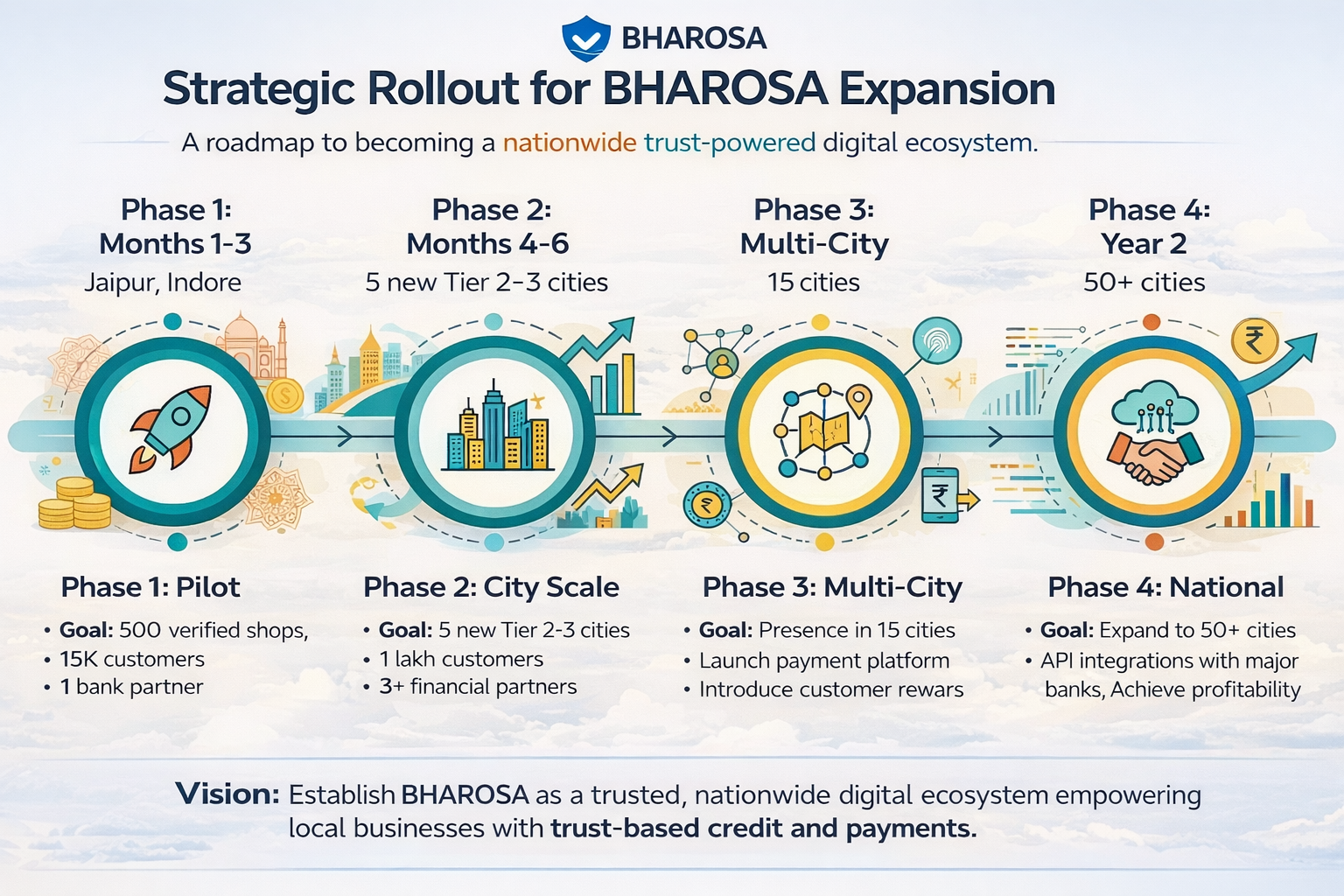

FUTURE PLANS

-

OUR FOCUS AREAS

Inspiration

Whenever a customer goes to any shop, they do not know whether the shop is trustworthy or not.

Customers are often unsure:

Is the shop selling genuine products?

Is the shop selling goods at a fair price or overcharging?

Is the quality of goods reliable, especially in small local shops like kirana stores, clothing shops, and daily-need stores?

Today, customers mostly rely on word of mouth to judge a shop.

However, word of mouth:

Does not reach everyone

Is slow

Is not available online in a structured way

There is no simple digital system where a customer can:

Check a shop’s reputation

See how other customers rate that shop

At the same time, shopkeepers face a different problem:

When they need a loan, they usually get it at a very high interest rate

Banks judge shopkeepers mainly on money and paperwork, not on customer trust

We realized that:

Customer trust already exists, but it is invisible to banks

Good shops with loyal customers are not rewarded financially

This inspired us to build BHAROSA:

A platform where customers can rate shopkeepers

Where customers can check shop ratings online

And where customer support and trust become the foundation of a shopkeeper’s credit score

The core idea behind BHAROSA is:

“A shop’s creditworthiness should depend on customer trust, not just money.”

By integrating this trust-based credit score with banks:

Shopkeepers with good customer support can get loans at lower interest rates

Honest shops are rewarded

Customers feel safer choosing where to buy

What it does

BHAROSA allows customers to rate shops based on their real buying experience.

It helps customers check a shop’s rating online before purchasing, so they can decide:

Whether the shop is genuine

Whether it provides good service

Whether it is trustworthy to buy from

Customers can:

Share their opinion about a shop

Write comments about service quality, pricing, and overall experience

These ratings and comments help future customers judge:

If the shop sells genuine products

If the shop charges fair prices

If the shop treats customers well

🔁 Benefits for Shopkeepers

Every positive customer rating contributes to the shopkeeper’s credit score.

This credit score is not based on money alone, but on:

Customer support

Customer satisfaction

Customer trust

A higher credit score helps shopkeepers:

Access loans from different banks

Get loans at lower interest rates

Build and expand their business more easily

💰 Monetization & Growth Support

The platform also provides monetization opportunities for shopkeepers:

Integration with creators and digital partners

Tools that help shopkeepers promote and grow their business

E-book and digital record services are available:

Shopkeepers can maintain business records

Track expenses and activities digitally

Transaction history feature helps shopkeepers:

Keep track of all past transactions

Monitor daily and monthly business activity

🤝 Customer Loyalty & Trust Management

Often, customers claim they are “regular customers” to ask for extra discounts.

This app solves that problem by:

Maintaining a record of customers who have rated the shop

Tracking how many times a customer has visited or interacted

This helps shopkeepers:

Identify genuine regular customers

Decide fairly whether to offer discounts

Avoid unnecessary losses

Future Enhancements (Planned)

In future updates:

Customers who regularly buy from a shop will be rewarded

They may receive:

Cashback coupons

Cashback offers

Payment-based rewards

These incentives encourage:

Customer loyalty

Repeat purchases

Long-term trust between customers and shopkeepers

How we built it We built BHAROSA as a prototype-first application focused on trust, usability, and real-world feasibility.

Google AI Studio was used to design and test AI-driven flows such as verification logic, rating behavior, and credit score updates.

The app was developed with a mobile-first approach, creating separate but connected experiences for customers and shopkeepers.

A QR-based identity system was implemented to link customer actions (ratings and scans) directly to shopkeepers.

Credit scores and loan eligibility were modeled using rule-based logic to clearly demonstrate how customer trust impacts financial access.

Mock data and predefined test cases were used to ensure the prototype is testable, predictable, and demo-ready.

Privacy and security were considered by design, keeping sensitive identity and biometric data hidden at all times.

Challenges we ran into

One of the main challenges we faced was integration with banks and financial institutions.

While the concept of a customer-trust-based credit score is strong, not all banks are currently open to adopting alternative credit models.

Many banks still rely heavily on:

Traditional financial documents

Income-based credit scoring systems

Getting positive responses for:

Credit card issuance

Low-interest loans based purely on customer trust required extensive discussions.

At the prototype stage, we focused on:

Demonstrating feasibility

Designing a system that banks can integrate with in the future

We are actively working toward connecting with:

Multiple banks

NBFCs and fintech partners to make this service fully operational.

Accomplishments that we’re proud of We successfully built a working trust-to-credit prototype that connects:

Customers

Shopkeepers

Financial access

Designed a system where:

Customer ratings directly influence a shopkeeper’s credit score

Better service leads to better loan opportunities

Created separate, well-defined experiences for:

Customers (simple and fast)

Shopkeepers (business-focused and secure)

Implemented a QR-based identity and rating mechanism that is easy to use and scalable.

Ensured the prototype is:

Testable

Demo-ready

Easy for judges to evaluate

Maintained privacy-first design, keeping sensitive identity data protected at all times.

What we learned Trust is a powerful asset and can be digitized and measured when designed correctly.

Small merchants need:

Access to credit

Fair interest rates more than complex financial tools.

Customer behavior and feedback can be a strong alternative credit signal.

Building real-world fintech solutions requires:

Technical innovation

Regulatory awareness

Institutional collaboration

Most importantly, we learned that:

Solving real problems requires patience, simplicity, and alignment with existing systems.

What's next for BHAROSA

Complete Payment App

BHAROSA will evolve into a full payment app where customers can pay directly within the platform.

UPI Integration

Seamless UPI payments to ensure all transactions are recorded automatically.

Accurate Credit Scoring

Real payment data will strengthen trust-based credit score calculations.

Bank & NBFC Partnerships

Integration with banks and NBFCs to enable real loans and credit cards at lower interest rates.

Customer Loyalty Rewards

Cashback, coupons, and incentives for customers who regularly shop and pay on time.

Loan Repayment & EMI Tracking

Shopkeepers will be able to track EMIs, due dates, and repayment status.

Fraud & Fake Rating Detection

AI-based mechanisms to prevent fake ratings and misuse of the system.

Merchant Business Insights

Simple analytics on customer visits, repeat buyers, and payment trends.

Unified Service Platform

One app for payments, ratings, trust, credit, and business management.

Expansion to More Local Businesses

Extend BHAROSA to medical stores, service providers, and other MSMEs.

Log in or sign up for Devpost to join the conversation.