Inspiration

In Peru, approximately 55% of the population is banked (around 15 million people). This percentage of banked individuals is primarily concentrated in urban areas. In rural areas, the rate of banked individuals drops to around 20%, according to statistical data from the Peruvian government.

These banking statistics are closely related to the poverty that exists in most rural areas. In fact, according to the latest survey conducted by the Peruvian government, around 23.3% of the population in the country lives in poverty and extreme poverty. This translates to more than 7 million Peruvians who are unable to afford a basic food basket.

Due to extreme poverty and consequently low levels of banking access, the inadequacy of transferring benefits or bonuses granted by the Peruvian government to the most affected areas was evident during the COVID-19 pandemic. As the primary method of transfer was through national banks, nearly 60% of individuals were unable to successfully claim the received bonuses. This money went unused for its intended purpose and could have represented an opportunity for survival or development for individuals within the community and the community as a whole.

While the poor effectiveness of bonus transfers has been criticized for not accurately classifying vulnerable populations, another significant problem has been the inefficiency in the transfer process itself. This is due to the challenges posed by low banking access and a financial sector that has not actively integrated these segments into their service offerings. Additionally, the unclaimed money could have been used to continue offering communal benefits instead of remaining dormant, waiting to be claimed.

An important point to note is that despite the high levels of poverty as of 2021, around 90% of the country's population owns a mobile device. This presents an incredible opportunity to utilize this technological platform as a means of financial inclusion.

Why Ayllu?

The term ayllu designated an Inca social organization based on kinship ties, common origin and common properties, such as being linked to a territory. In an ayllu, extended families shared responsibilities and worked together for the benefit of all.

What it does

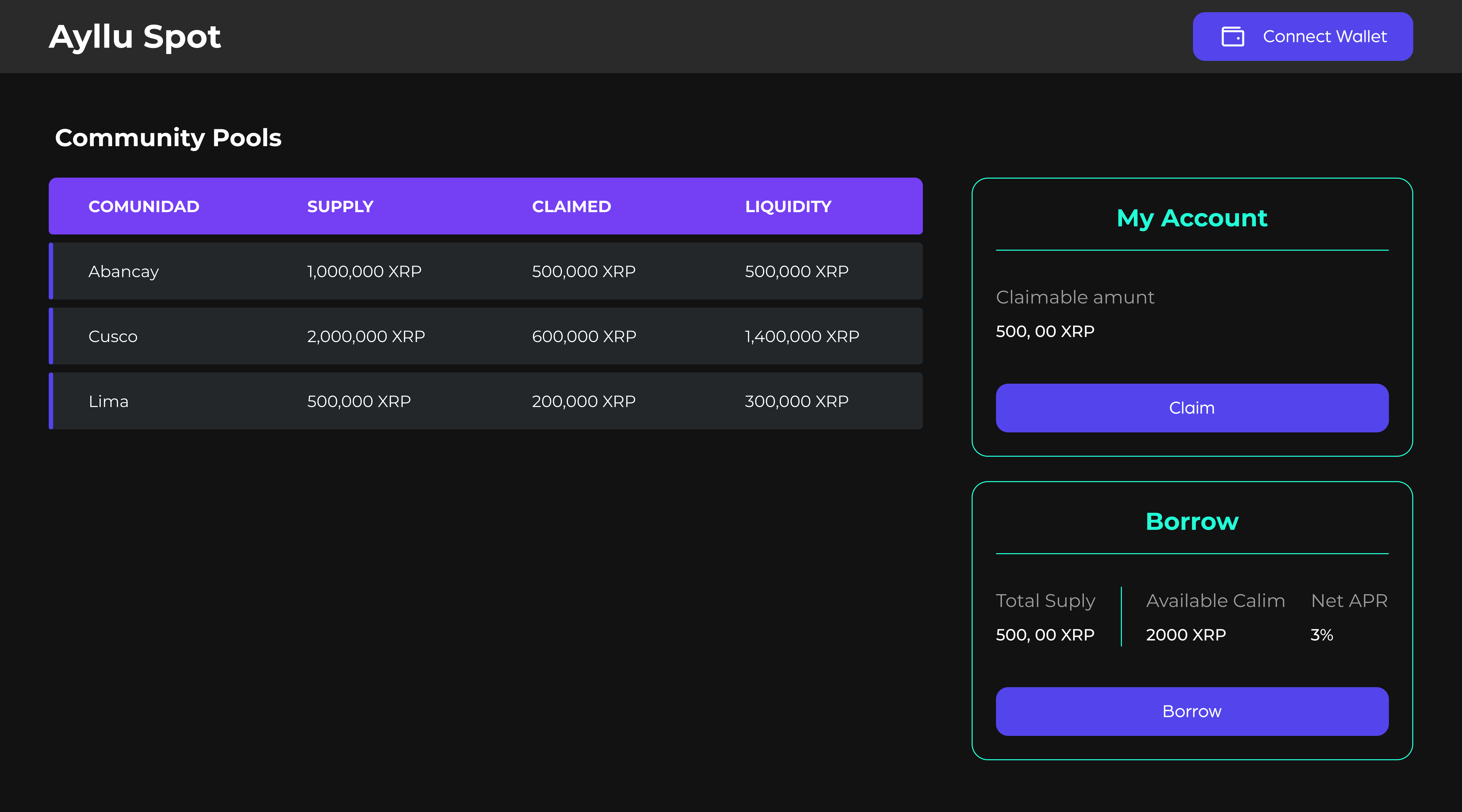

"Ayllu Spot" is the application that allows citizens of a community to obtain credits from community funds distributed as social assistance by the government that have not been spent. In this way, from their wallets, they can not only receive the CBDC (Central Bank Digital Currency) from social programs of which they are beneficiaries, but also have access to this community "liquidity pool" and request microloans that are overseen by the other members of the community.

How we built it

Platform for the Central Bank A web application that enables the Central Bank to do the following:

- Create one or multiple Liquidity Pools per Community.

- Define the wallet addresses that have permission to claim from the Pools.

- Set minimum or maximum token quantities that can be claimed.

Community Platform A web application that allows the following:

- Visualize the created Liquidity Pools.

- For each Community, two Pools will be created: one for bonuses and another for loans.

- Total allocated token amounts for each Pool can be viewed, along with the claimed token quantities and remaining token balances.

- The most recent users who have claimed the available tokens can be seen.

- A decentralized voting system will be integrated, allowing platform members to vote in favor or against proposed proposals. This will decide the utilization of unclaimed funds that belong to the community.

Mobile Application

- Users create a wallet associated with their national identification number.

- Through the mobile app, users can access their CBDC, perform transactions, or vote on proposals presented by the community for fund usage.

Tech Implementation Proposal

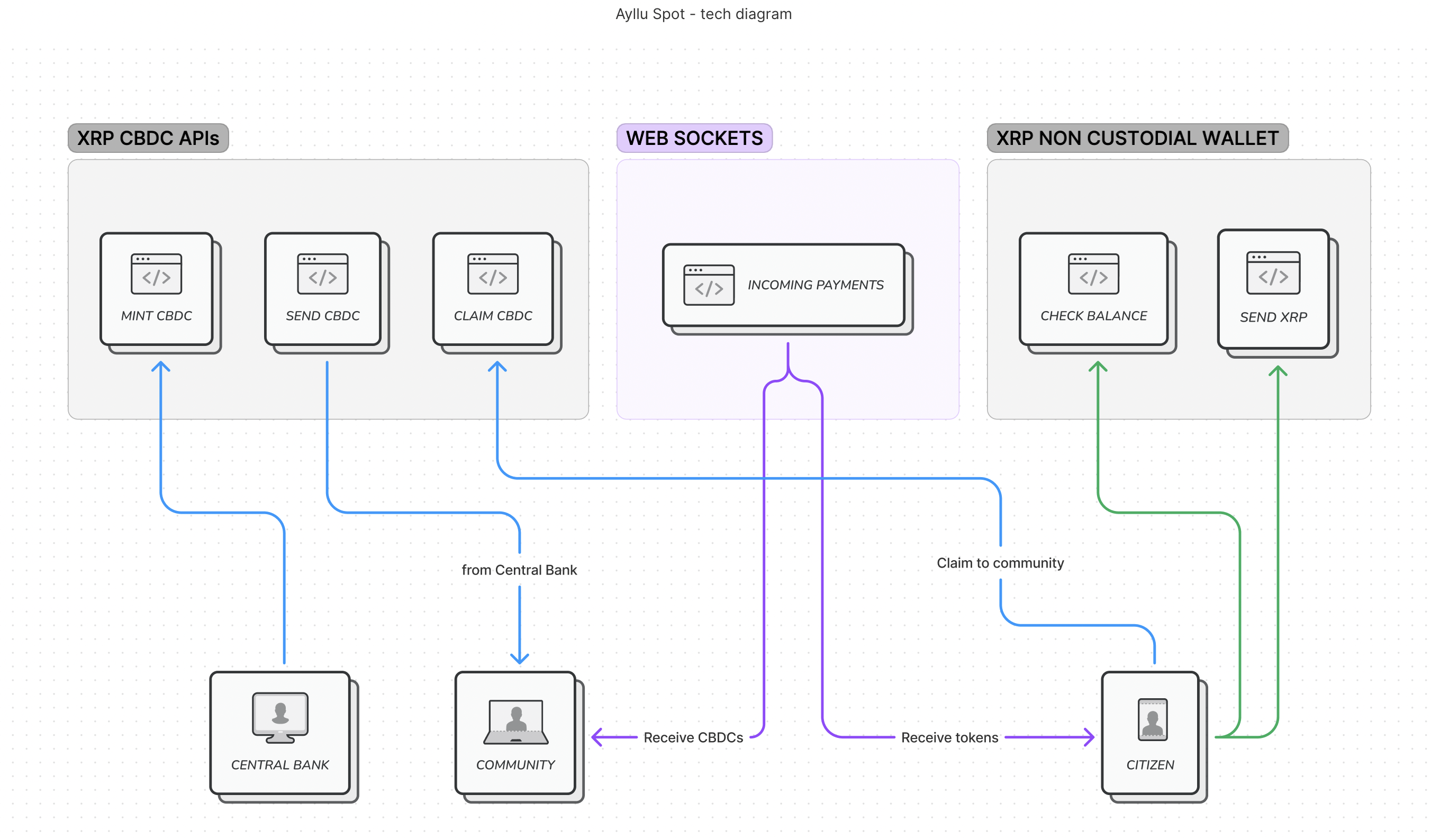

Architecture Diagram v2

As you can see in the following proposal we have 3 actors:

- Central Bank

- Community

- Citizens

Where the Central Bank will be able to mint CBDCs for each Community for send them on demand. Each community will receive a realtime notification each time the Central Bank send the tokens. Once the community receive the CBDCs their Citizen will be able claim those through their non custodial mobile wallet. We will implement a non-custodial wallet for citizens in order to provide a specific features like check account balance, show history payments or pay their loans. We will use the WebSocket protocol to watch for incoming payments.

Sources:

- https://ripple.com/solutions/central-bank-digital-currency/

- non custodial wallet - Sample code

- Payment Channel - Sample code

- Monitor Incoming Payments with WebSocket - Sample code

Legal Basis

In Peru, the State stimulates the creation of wealth, the freedom of work and the freedom of business, commerce and industry.

The financial system is a fundamental pillar for people to access credit and develop their life project.

In the last 20 years, Peru has seen its economy consolidated. However, in crisis situations, the limited management capacity of financial institutions for the recognition and granting of bonds and/or credits by the state has become visible, especially to those people who live in rural areas and remote areas.

Ayllu arises as a solution to this problem, guaranteeing the right of people to be able to access credit and be able to carry out their objectives and goals with the resources not used or distributed by state entities.

Thanks to Ayllu, the Peruvian State can fulfill its role as a promoter of wealth, boosting the economy and contributing to the reduction of poverty, especially in those areas where access to capital is quite remote due to the lack of state infrastructure.

Log in or sign up for Devpost to join the conversation.