-

-

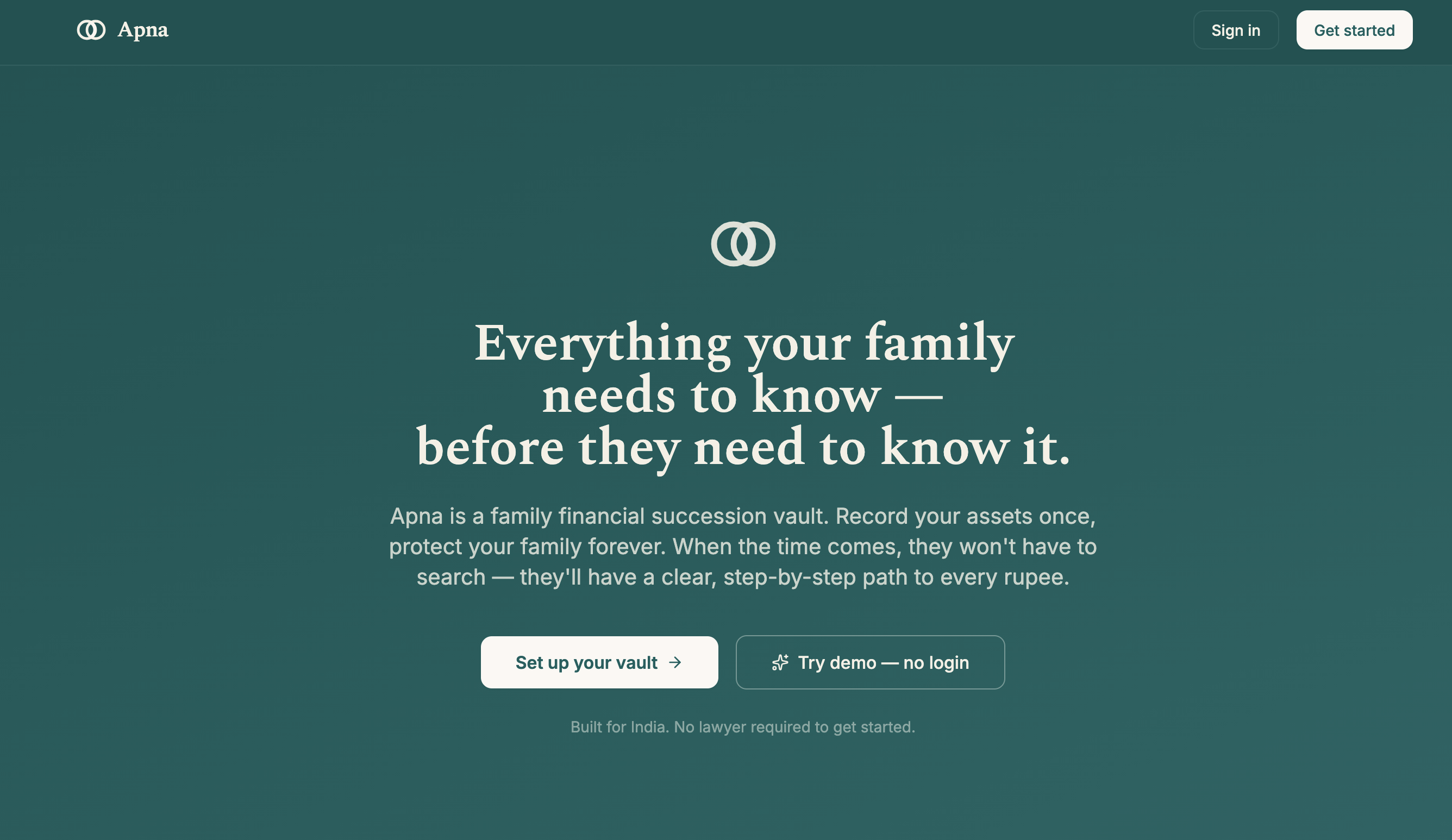

Homepage

-

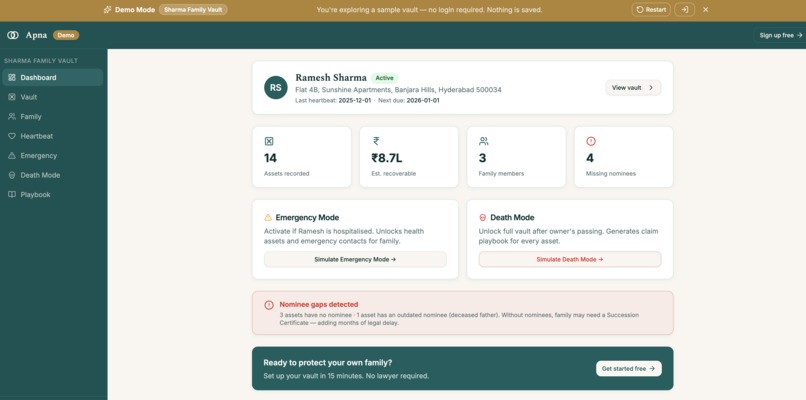

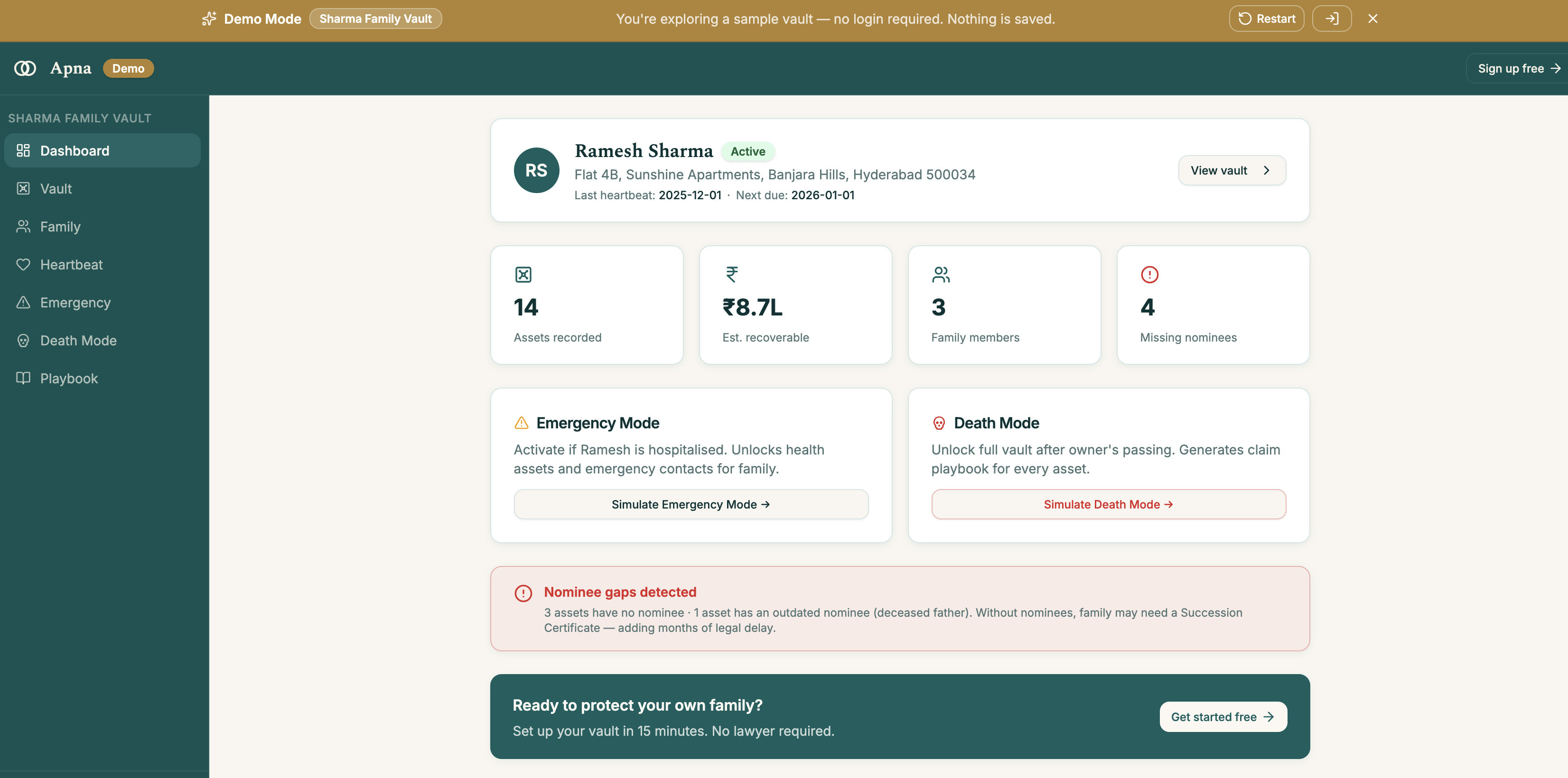

Demo Mode

-

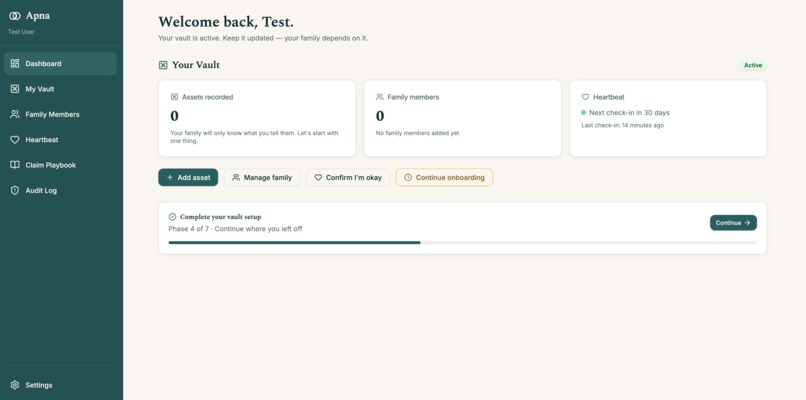

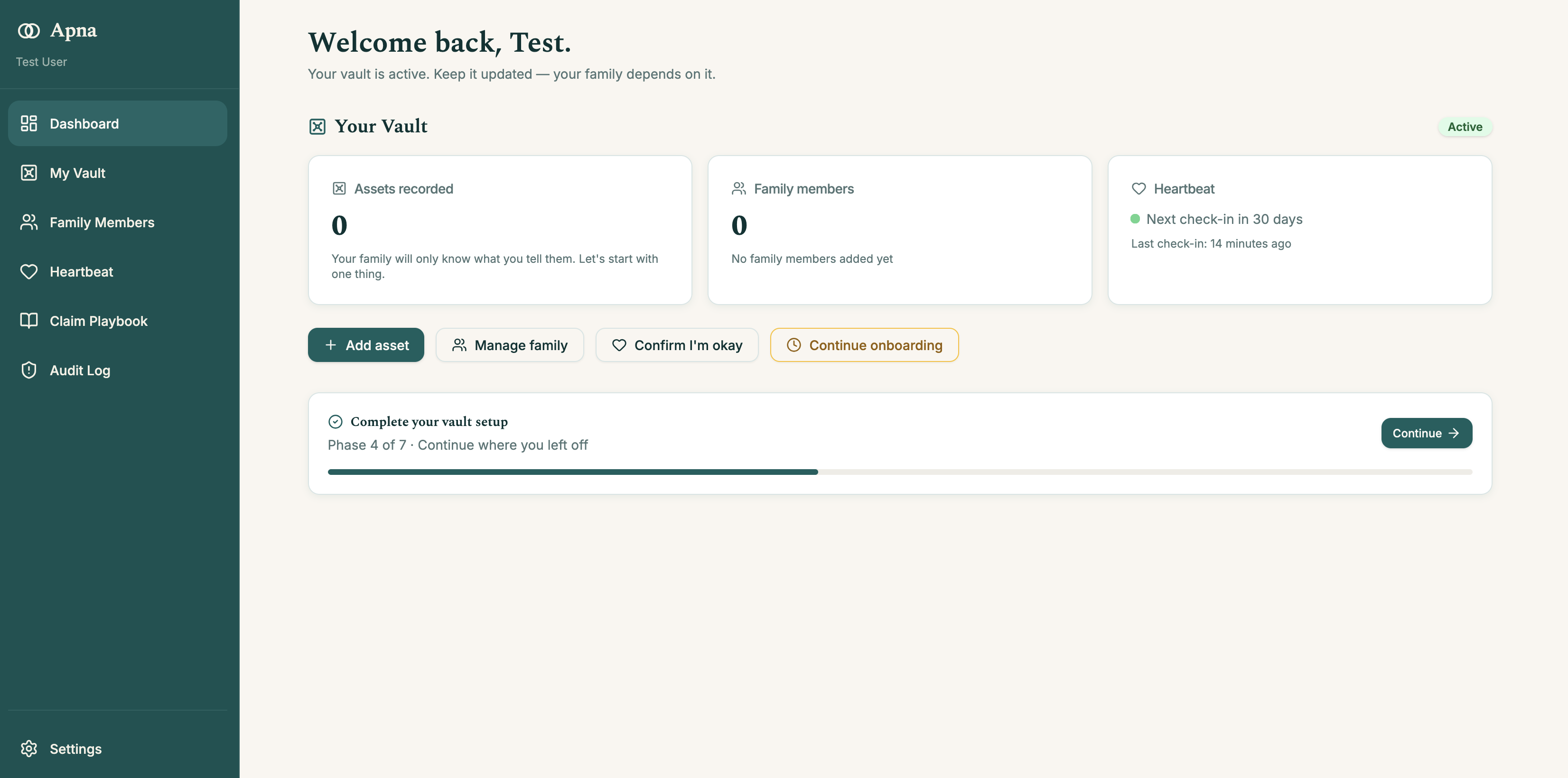

Setup mode

-

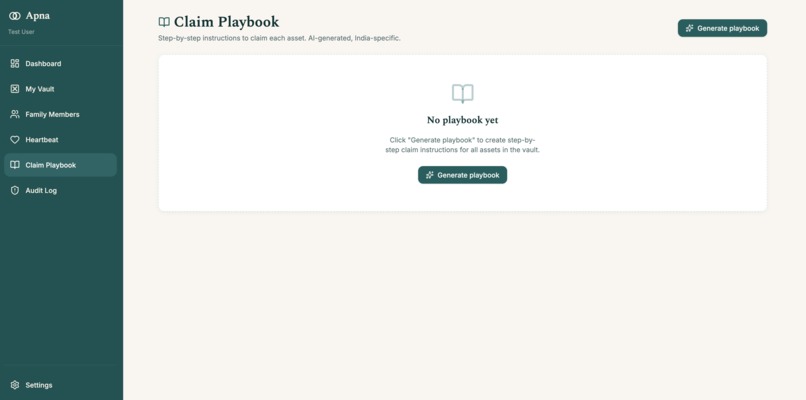

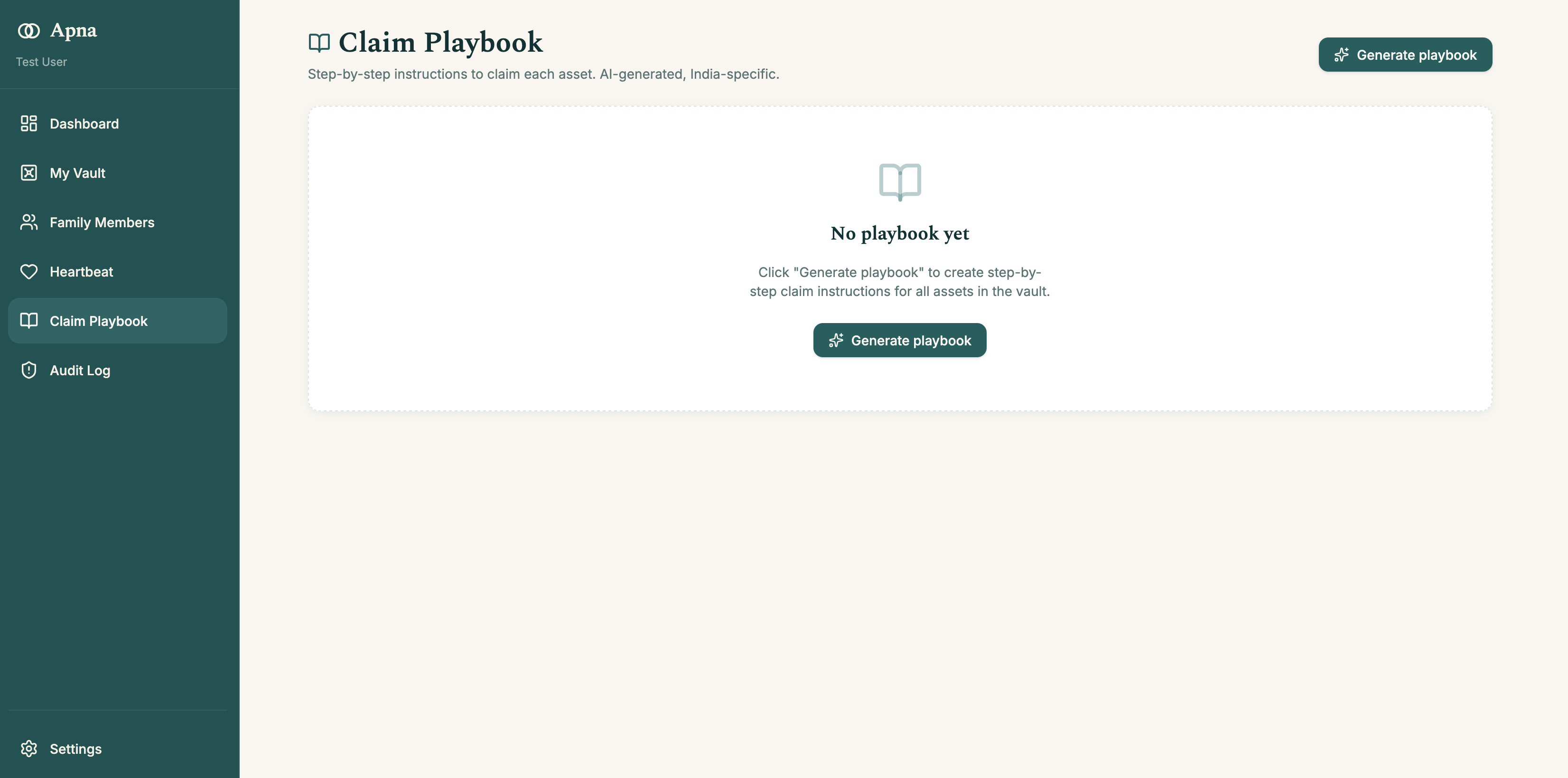

AI Playbook

The ₹1.84 lakh crore problem

In India alone, over ₹1.84 lakh crore sits in unclaimed bank deposits, EPF accounts, insurance policies, mutual funds, and dormant demat accounts. Behind that number are real families — most of whom have no idea what their parent, spouse, or sibling actually owned.

The system assumes you know. When someone passes away, the burden of remembering every bank account, every old PF from a job 20 years ago, every LIC policy, every SIP, every locker — falls entirely on the family. Banks won't tell you. EPFO won't notify you. Most discoveries happen by accident, years later, when a stray SMS arrives.

We've all watched a family go through this. They aren't fighting grief and paperwork separately — they're fighting both at once, with no map.

What Apna does

Apna is a family financial vault with three modes, designed around the moments that actually matter:

1. Setup mode — while you're alive and well.

The Owner records every asset they hold: bank accounts, FDs, PPF, EPF (UAN), NPS, LIC and private insurance, health insurance, mutual funds, demat, lockers, property, vehicles. An AI-guided interview walks them through it — and prompts for the ones they forgot ("Have you ever worked a salaried job? You probably have an EPF account. Let's find your UAN.").

Then the Nominee Health Check runs across every asset. Missing nominee on your LIC? Apna flags it: "Without this, your family will need a Succession Certificate — that's 6–9 months and ₹30,000+ in court fees. Fix this in 10 minutes online." This single feature has saved households real money before any tragedy ever occurs.

2. The heartbeat — passively keeping the vault honest.

Every 30 days, Apna pings the Owner: "Quick check-in. Still active? Anything to update?" One tap confirms. Miss three pings in a row, and Apna automatically escalates to the family: "We haven't heard from [name] in 90 days. Please check on them." No false alarms — there's a snooze for travel, hospital stays, anything. But if something has genuinely happened, the family is on the case within weeks, not years.

3. Emergency Mode & Death Mode — the unlock.

In a medical emergency, the spouse can trigger Emergency Mode with a PIN. Only health insurance details, emergency contacts, blood group, allergies, and current medications unlock. Bank details stay locked. Every read is audit-logged so the Owner sees exactly who saw what when they recover.

For Death Mode, the nominee uploads the death certificate. An AI vision call validates it's a real government-issued certificate (not an Aadhaar, not a blank page, not a bank statement), extracts the name and date of death, and cross-checks against the vault's Owner. Only then does the full vault open.

The Claim Playbook — the part that makes recovery actually possible.

The moment Death Mode triggers, Apna generates a personalized claim playbook. Per asset: which portal to visit, which exact form to file (Form 20 for EPFO, Form 3783 for LIC, Form 303 for NPS, transmission form for demat), every document required, realistic timeline, common pitfalls. The AI also drafts the affidavits, indemnity bonds, and covering letters — pre-filled with the deceased's and claimant's details from the vault. The family just adds signatures and notary.

Everything renders as a Kanban board the whole family shares. Mom, son, and daughter all see who's doing what, in real time. No duplicate trips to the bank. No "I thought you were handling that."

Inspiration

The math of this problem is staggering, but what kept us in it was the human side. Every family we know has a story — a forgotten EPF account from a parent's first job, a fixed deposit nobody knew existed until a passbook turned up in a drawer two years later, an LIC policy whose nominee was a sibling who had also died.

Existing products solve adjacent problems. Sunset (US only) auto-discovers assets after the fact. Empathy bundles grief support with paperwork. Kustodian in India is a paid concierge service that recovers money once it's already stuck. Generic dead-man's-switch tools like Cipherwill and GoodTrust handle digital legacy — social accounts, crypto keys — but not structured financial succession.

Nobody combined: a family-shared vault + a passive heartbeat + AI-guided multi-country claim playbooks. That's the wedge. Apna isn't for after it goes wrong. Apna is for so it doesn't.

How we built it with MeDo

MeDo did the heavy lifting. We worked in ten conversational passes:

- Concept and visual scaffold — landing page, sign-up, role model (Owner vs Family Member).

- Data model — Users, Vaults, Assets, FamilyMembers, Heartbeats, ClaimTasks, AuditLogs.

- Onboarding interview — a conversational, multi-phase asset capture flow (banking → government-linked → insurance → investments → physical/digital → nominee health check). MeDo handled the conditional logic and the LLM-driven prompts that surface forgotten assets.

- Family invites and permission roles — granular permissions for emergency visibility, post-death visibility, and trigger rights.

- Heartbeat system — the 30/60/90-day escalation logic with snooze, soft reminders, and the automated family escalation email.

- Emergency Mode — partial vault unlock with re-auth, scope-limited reads, and an immutable audit log.

- Death Mode + death-certificate AI validation — LLM vision call to verify the uploaded document, extract the deceased's name, cross-check against the vault.

- Claim Playbook generation — for every asset type, MeDo's LLM generates the specific portal, form name, document list, and timeline, grounded in a seed taxonomy of India's institutional procedures (EPFO, LIC, IEPF, UDGAM, RTAs, NPS).

- Demo Mode — a runtime mode that pre-seeds the Sharma family vault, lets you fast-forward heartbeats, and includes an Auto-Tour button that fires every state transition with on-screen captions. This is what made the demo video possible.

- Branding and copy polish — tone of voice, empty-state microcopy, the Nominee Health Check flag styling.

What surprised us was how well MeDo handled state machines. The heartbeat flow has eight distinct states (active → missed-1 → missed-2 → escalated → emergency → resolved → death → vault-closed) and MeDo correctly wired the transitions and the side effects (email triggers, suppression of further pings after death) on the first conversational pass.

Challenges

Validating death certificates without a real verification API. We don't have access to a government registry, and the hackathon timeline ruled out integrating one. We solved this with a vision LLM call that checks for the structural features of a death certificate (issuing authority, name field, date of death, registrar's signature block) and rejects obviously wrong uploads. Tested across five sample images — real PDFs from gov sites, blank pages, an Aadhaar, a bank statement, a photo of a person — two failed correctly. It's not bulletproof, and a production version would integrate with the Civil Registration System. For a hackathon demo, it's enough to prove the mechanism.

Stopping the heartbeat after death. The first version kept sending check-in emails to the deceased Owner's inbox. Catastrophic for trust. We added explicit suppression: when vault.status == death_mode, all Owner notifications are blocked at the dispatch layer.

Permission gating. Getting Emergency Mode to leak only health-insurance and emergency-contact records — and nothing else — took three iterations. We ended up writing the permission predicate as a single function (can_user_read_asset(user, asset, vault.status)) and routing every render through it. Once that was done, the UI couldn't accidentally leak anything because the data was never fetched in the first place.

Grounding the AI on Indian institutional procedure. Out of the box, the LLM cheerfully invented form names that don't exist ("Form LIC-72A for nominee claims" — there is no such form). We solved this by seeding the playbook prompt with a hand-curated taxonomy of real Indian institutions and the exact forms they require. The AI uses the taxonomy as ground truth and fills in the personalization (names, addresses, account numbers from the vault) on top.

Tone. Every microcopy choice mattered. The Owner is staring at a screen that's quietly preparing for their death. Get the tone wrong by one word — euphemistic, breathless, morbid — and the product becomes unusable. We wrote every empty state, every tooltip, every confirmation modal by hand, and stress-tested them by reading aloud to people who'd lost a parent. The line "Your family will only know what you tell them. Let's start with one thing." came out of that.

What we learned

- The hardest engineering problems in a product like this are not engineering problems. They're trust problems. The heartbeat cadence, the snooze button, the audit log visible to the Owner — none of those existed in our first design. They came from imagining how a real family would actually use this.

- LLMs are stunningly good at procedural tasks (which form, which portal, which document) when grounded with a small seed taxonomy. Without the seed, they hallucinate confidently. With it, they're better than most call-center agents.

- A "Demo Mode" that fast-forwards state machines turned out to be a feature we'd want in every product, not just for hackathons. It's the fastest way to find bugs in any time-based system.

What's next

- Multi-country expansion. UAE, US, Singapore, UK. Each country has its own institutional taxonomy. The architecture is built to plug them in.

- Diaspora-first features. When the Owner lives in India and the children are in three different countries, who can trigger what, and from which jurisdiction's KYC? This is the wedge that nobody else has.

- Real institutional integrations. UDGAM, IEPF, EPFO unified portal, Bima Bharosa, CAMS — start with read-only verification, eventually claim submission.

- Voice onboarding. For elderly parents who hate typing. A 20-minute phone call with the AI captures everything.

- Lawyer marketplace. When a Succession Certificate is genuinely required, route to a vetted local lawyer who specializes in nominee disputes.

Apna is a product we'd want our own families to use. That's the bar we built it to.

Built With

- ernie-llm

- javascript

- medo

- node.js

- postgresql

- react

- rest-api

- tailwind-css

- vision-llm

Log in or sign up for Devpost to join the conversation.