-

-

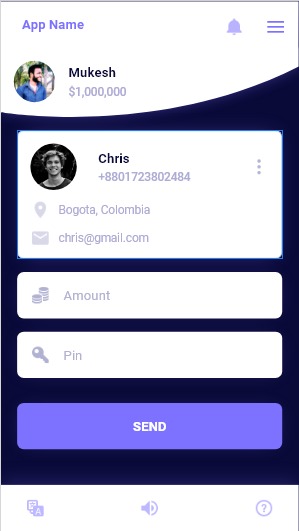

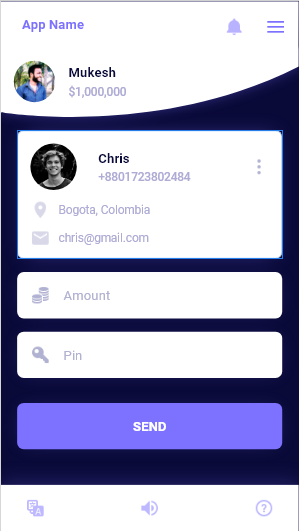

Simple App UI

-

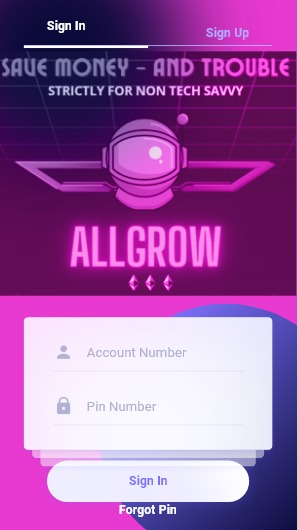

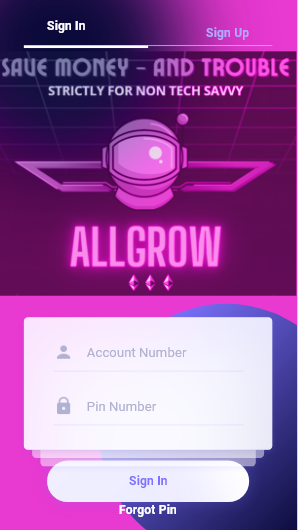

App Log In

-

Logo

Introduction

All individuals will have access to banking and financial services through financial inclusion. Its goal is to provide fundamental financial services to everyone in society, regardless of their income or savings. It focuses on providing financial assistance to those who are economically disadvantaged. The word is loosely defined as the provision of low-cost and simple-to-use savings and lending services to the poor. Its goal is to ensure that the poor and marginalized have access to financial education and make the greatest use of their money. Financial inclusion is becoming easier to attain because of advancements in financial technology and digital transactions. Financial inclusion as envisioned encompasses not just having access to or using financial services, but also the quality of those services. Financial services that are focused on quality are responsive and responsible, satisfying consumers' requirements and capacities while also being safe and user-friendly. As a result, financial inclusion is a catalyst for broad-based economic growth and resilience, better financial health, job creation, and development. Every country requires an inclusive financial system as part of its infrastructure. With up to 1.4 million migrant workers, Singapore is one of the world's largest hosting countries for migrant workers, primarily from Southeast Asian countries with fewer prospects for high-paying jobs, such as the Philippines, Vietnam, Thailand, and Indonesia. This population, as well as the remittances they bring home, is critical to the economy of both the host and home countries, not to mention the individual families that rely on the consistent wages earned abroad and remitted home. Migrant workers have historically had limited access to financial services; the majority are unbanked and rely on black market lenders that specialize in providing short-term loans and remittances to migrants. Cross-border money transfer, on the other hand, is a complex, tightly regulated business with numerous players that has recently gotten a lot of attention due to the rising number of financial transactions each year and the resulting profit possibility for anyone who can facilitate such transactions. *Average construction worker salary is 1200 SGD per month but quite a lot of standard deviation, can be as low as 500 take home after agency fees, workers usually transfer half the money back home.

First Principles (Survey)

For the design of our product, we decided to pursue the path of First Principles Design, where we break down the problem in hand in the most basic form, questioning every single detail relating to the solution we would provide. Fundamentally, as we referred to the previous comments as well as the problem at the most granular level is that people coming from low/middle income families residing in Singapore face extremely high fees when sending cross-border oversea payments.

So our proposed approach would be to provide a solution involving blockchain decentralization, fast transactions, and lower fees. However, the solution which would incorporate blockchain would involve extra steps which could potentially make the process unnecessarily complicated for non-tech savvy users. So ultimately we would need to reduce the number of steps to sending the payments as minimally and smoothly as possible, while still enabling safety and low-fee fast transactions.

For that reason, we compiled a survey on some of the questions we deemed as the most important for the initial steps undertaken toward the solution design. The target audience of the survey conducted is aligned with the background of the potential future users: Lower-income household families in Singapore which frequently use remittance services for cross border payments in neighboring countries. From their answers we could derive the following points:

Most of our users spend more than 5 hours per day using the phone, and from that amount they spend less than 1 hours reading financial news through the mobile phone. Their preferred language of use is English, despite being from different backgrounds having different native languages. The main use of their phone is utilizing mobile apps for buying food and other accommodation utilities. Usually the money sent back to family and relatives is less than 300 SGD / month. Most of our users have little to no knowledge about financial planning or blockchain technology. Majority have complaints about the fees, and would wish it to be lower than the standard 5 SGD.

With the following answers in mind we are ready to take the first steps towards the design of the product.

Product

Our app, AllGrow, is hoping to improve financial inclusion in Singapore by offering advanced financial advisory and education through our app. Cross border remittance services will also be available on our app. AllGrow is mainly targeted towards middle to lower income households in Singapore as well as migrant workers. Migrant workers tend to transfer their money back to their families and the international money transfer services, like Western Union, take a significant percentage of their money transfer for providing the transfer infrastructure. AllGrow hopes to reduce the transfer fees for migrant workers by providing a greener, more efficient cross border transfer infrastructure built on a low-cost blockchain like Binance Smart Chain. Migrant workers generally tend to be financially illiterate, like most of the impoverished, and AllGrow hopes to improve global financial literacy through our app. Once the mandatory financial courses are completed, based upon the customer’s financial information, they will be recommended financial products to invest in based on AllGrow’s proprietary financial advisory platform. Overall, we plan to lower costs of cross-border remittance and increase the overall wealth of migrant workers through financial education and sound investments. In cross-border remittance, there are several competitors like TransferWise, Remitly, Western Union and in financial advisory, there are competitors like Financial Alliance Pte Ltd and the local banks. However, as a full platform for financial advisory, remittance (based upon blockchain) and financial education, AllGrow believes that we will be able to outperform competitors with cheaper fees and a greater quality of service. The average cost of transfer is roughly 10 SGD for a 300 SGD transfer to Bangladesh via Western Union (~3%). Blockchain-based remittance providers like Wirex and Wyre are able to offer fees of less than 1% and this reduction in fees would be especially meaningful to highly price sensitive customers like the migrant workers.

UI/UX

Deriving from the survey and research conducted on the target audience for the application, we would need a smooth user experience which would lead to the final output (transfering the money) in the smallest number of steps possible. The audience would have little to no tech expertise, therefore we would be able to offer assistance in each step - as well as a guidance on how each service works in a prelude tutorial explaining in high level the flow of the services. The themes are modern in style, revolving around gradient purple, blue and black as the core colors - while also involving a Klarna-style type of animations. Basically, following Steve Krug’s book - “Dont make me think”, our app will try to encompass the following points:

Useful: Doing something people need to be done, which in this case is remitting money across the border. Learnable: People figuring out how to use it and also learning new concepts about the blockchain and financial investments and savings. Memorable: Having very few steps to recall each time they use the app. Efficient: Accomplishing the service within a reasonable amount of time and effort. Delightful: Using the platform will be an enjoyable and even fun experience.

Basically, the main tenet of the book is “Don’t make the user think”!

In this case we tried to accomplish that in a combination of Adobe XD & Photoshop which we show in the demo - below is a screenshot on how the app would look like:

Competition Below we reviewed the pricing of players in the same market of cross-border fund transfer and financial product selling platform. Cross-border fund transfer Service Provider Fee for 500-1000 SGD transfer to Bangladesh Remitly 3.99 SGD Wise 6.47 SGD + 0.5% conversion cost Western Union 9.81 SGD Current blockchain technology ~2% of conversion cost, expected to reduce drastically in the future

*All transfers take place within minutes. Blockchain Service Provider Fee for 500-1000 SGD transfer to Bangladesh Circle 2.9% + $0.3 Wirex 1% Wyre 0.75% Bitpay 1%

Financial products - competition (to check)

Technology & Infrastructure

A remittance transfer is an international electronic money transfer that has proven extremely important for friends and relatives to send money quickly and effortlessly across borders. Individuals must follow the global economy as it grows and as work possibilities spread across borders. There are already several competitors in the market. So how is our remittance service different from others? Our network uses the blockchain technology to transfer funds across the country with higher speed, lower price, and better convenience. Blockchain features that we’ll leverage to use in our network are increased capacity, better security, immutability, and faster settlement.

The most difficult part is not the cryptocurrency transfer itself, but it is how to convert cash to crypto and back to cash again with the lowest fee and highest speed. The best solution is to link our solution to the largest exchange in the world, Binance. The volume and liquidity in Binance helps keep the exchange rate stable and true to the market. Existing features such as P2P Express and Binance Pay makes this system free and instantaneous. We will build an API that will use the P2P function to transfer fiat into a stable coin such as USDT, then use Binance Pay to transfer the USDT to a Binance wallet located in the respective country that we want it to be. Then, we can use P2P again to transfer to the bank account that we want.

A limitation with this system is that the maximum amount of USDT that can be exchanged at a time is 5,000 USDT through the P2P Express, but it shouldn’t be a problem since our target group is for middle-low income. Another problem is to find a way to transfer money in countries where Binance is banned or there isn’t a P2P with the countries’ fiat currency. Countries that Binance is banned in include Canada, China, Europe, Malaysia, Japan, and the UK. A way to mitigate this problem is to use cheap and fast chains such as BSC, Solana, or Tron in order to transfer the stable coins into the locally available crypto exchanges in the respective country. All these chains will require no more than $1 USDT for each transfer with arrival time around 5 minutes. An alternative to using Binance is to use Kraken, eToro, Coinbase, Huobi, or Gemini. Though, there will be fees while transferring USDT because it will be from one platform to another. Another limitation with using other platforms is that the transfer will not be immedient. There will have to be a wait time for the transfer of the cryptocurrency itself as well as the processing time to transfer fiat currency into the bank account.

Let’s take a look at the process of setting up a remittance network for migrant workers who're working in Singapore and want to transfer money to their friends and family who live in countries such as India, Bangladesh, Indonesia, and Philippines. The first step is to set up a company’s bank account with a local bank in Singapore, such as DBS, to which our users will transfer SGD. Next, we’ll link that bank account to a crypto exchange platform that has an SGD/USDT pair available for trade such as Crypto.com. Once we know where our target customers will transfer the money to, we will create an account in the locally available crypto exchange platforms in order to convert the USDT to the desired fiat currency. Then, we will establish a relationship with the local banks and create a company’s bank account with them in order to be able to transfer the money to our customer’s friends and family. In order to establish offline trust, it is beneficial for our company to have local offices. It would be possible to open a business bank account if we have our branches in that country.

It would be preferable to do all this process within one application such as Binance because all the processes could be done with an API for just one application. Unfortunately, using only Binance is not possible because Binance does not have SGD/USDT pair available due to regulatory issues. For this case, India, Bangladesh, Indonesia, and Philippines all do have USDT pairs available for their respective currency. The trading fee for Crypto.com to trade SGD to USDT is 0.4% and the withdrawal fee using the BEP20 network is $0.8 USDT. The exchange fee from USDT to rupee, taka, rupiah, peso is free through the P2P feature in Binance. The exchange rate is usually better than the true exchange rate due to the high demand of USDT in these markets. This provides an opportunity for our company to further decrease our fees for our customers.

Our application also offers investment service through the use of blockchain. Since our customers may not have access to investment opportunities, we will integrate the popular borrowing and lending platform called Anchor Protocol into our app. Investors can lend out money to borrowers while getting a return of 19.5% APY. The currency used in this system is a stable coin called UST. Borrowers must provide either ETH or Luna as collateral and they will be able to borrow a certain percentage of the value of collateral that they put in. If the value of their collateral assets were to drop below the limit, their assets will be liquidated and unable to be redeemed. This provides a safety net for lenders knowing that the borrower's assets value will be enough to pay them back. There will be a trading fee of 0.1% in Binance in order to get from USDT to UST and a transfer fee of $1 UST to the Anchor network. There will also be a deposit and withdrawal fee of $0.25 UST for each process. Our investors will be able to withdraw the money whenever they want.

Cloud Infrastructure of RemitApp: A typical AWS Fintech Blueprint

The main cloud services we aim to utilize to keep hold and track of the data are the following:

AWS Client VPN used to access AllGrow resources from any location using an OpenVPN-based VPN client. AWS Config enables us to assess, audit, and evaluate the configurations of the AWS resources utilized by AllGrow. Config continuously monitors and records your AWS resource configurations and allows us to automate the evaluation of recorded configurations against desired configurations. Amazon Route 53 is a highly available and scalable cloud Domain Name System (DNS) web service. It is designed to give developers and businesses an extremely reliable and cost effective way to route end users to Internet applications. Amazon S3 used for storing the data retrieved from all the transactions occurred within AllGrow ecosystem - (for future analytics and predictive modeling) Amazon Aurora will be our main relational database built for the cloud usage of our data. Amazon Redshift uses SQL to analyze structured and semi-structured data across data warehouses, operational databases, and data lakes, using AWS-designed and will be used in complement to Amazon Aurora for storing the data Amazon Lightsail is an easy-to-use virtual private server (VPS) that offers simple management of cloud resources such as containers. AWS Glue is a serverless data integration service that makes it easy to discover, prepare, and combine data for analytics, machine learning.

Tech Stack: Main Programming Languages and Frameworks for Remitapp

Below we are including a list of potential programming languages, cloud services, and other frameworks which we could utilize for our project. Since it highly depends on the chain we would keep the door open for changes - however the core pattern will be the same.

a) Programming Languages (HTML / CSS / Javascript, Node JS. Redux – Front End) (Python, Erlang, Java, Solidity, Haskell, Rust) – Back End) (Kotlin, Swift, Java, Objective C – Apps) b) Cloud AWS (Using Redshift , EC2, Lightsail, S3, Aurora, Glue) c) Analytics and Big Data PySpark, Redshift, Sagemaker, TensorFlow & Keras d) Testing Environment (Ganache, Truffle, Infura)

A potential integration between the mentioned components on a very high level would follow a similar structure as below:

The list however is not inclusive, since there could be many other potential libraries and frameworks being experimented on and utilized under the team at different times in hidden repositories. From an engineering perspective, the tech stack appears solid, incorporating many reliable languages, modern frameworks and libraries (which of course account for the seamless user experience).

Financial Education and Investment Products Before we go into the details of the product, we will first discuss the challenges migrant workers have with the existing financial services, what their actual needs are and then how our app will approach them.

Financial inclusion for the low income group is our vision, and promoting financial education, better financial planning and access to financial products is the way to achieve that. However, since migrant workers have very little money, traditional banks and wealth management advisors wouldn’t serve them in-person because it is unprofitable. Besides, from traditional wealth management advisors’ perspectives, earning management fees from client’s investments is the priority, rather than helping clients to do financial planning with a more holistic view.

In the current market, robo-advisors solved part of the issue above by automating portfolio management with AI and thus lowering the cost to serve. Though they have been getting popular among the young middle-income group and a few platforms actually allow low investment amounts, they are totally not popular among migrant workers. We interpreted the reason as follows - firstly there are a variety of platforms available and each has different minimum investment requirements and fees, which are not easy to compare. Secondly the investment algorithm sounds like a blackbox. While for the educated middle-income group, they could easily read and understand those details, then feel comfortable about them; for migrant workers though, having little knowledge and inability to understand the investment products and mechanism behind would discourage them to embark and trust them. This means that they need clearer and easy to understand platform and products to start with, and gradually acquire financial knowledge in order to go further.

Another characteristic of migrant workers is they tend to have low income, low savings and some are in debt. If one has very little money and is working to make ends meet, he cannot afford risky investment products and any investments have to be liquid for any life emergencies. Since they are more likely to withdraw the money to meet emergency needs, this hinders financial ‘planning’. First, more education can solve part of the issue if the withdrawal is due to reckless spending. Secondly, the investment product needs to allow a very low amount of investment and be flexible to fit their liquidity needs.

We explored whether a full-fledged financial planning tool which gives automated financial advice would be suitable for them. In the market, there are numerous apps for financial planning, from banks or in app stores. Many of them encourage users to set goals, record assets, liabilities, income and spending. While having an up-to-date picture of the financial status is a prerequisite for effective financial planning and for the app to generate useful advice, not many people actually have the stamina to record and track personal finances continuously. This applies to migrant workers as well if they are not even aware of the value of this. Therefore, a full-fledged financial planning tool is not exactly effective for them. Instead, again, first they need more education to see the value of financial planning and feel comfortable about financial products. Secondly, a simpler tool that tracks and incentivizes savings and investments could help.

Our approach

To sum up above, the approach in our app is to provide financial education and the suitable financial product options that in general could suit their needs. Products need to be safe, and knowledge and trust needs to be established. Rather than giving them the options of many fancy funds that targets middle or high net worth group, fixed deposits or low-risk funds, for example money market funds or government bond funds of high ratings, and that give a little higher rate of return than fixed deposits and are allowed to pause payment and withdraw more flexibly, would be more suitable for them. We could partner with reputable banks or asset management companies to design funds that meet such requirements of being low risk, low funding requirement and high flexibility. There is a business opportunity in this as the low income group primarily kept their money in savings accounts or even in cash. As targeting to be a popular app for them to move funds, functions can be made available to set aside funds for savings and investments at the same time.

Investment products and platform

The products and platform have the following features:

Promotion of low-risk funds investments that are tailored to low-income group to the app users.

Both money sender and recipient who have downloaded the app could choose to set money aside for the funds at the time when they send and receive money. The option is easy to click, which aims to let you set aside a part of the money before you spend it for the rest of the month.

During app on-boarding, money sender and recipient are encouraged (perhaps motivated by discount in fund transfer) to download the app and complete several goal-setting questions. For example -

Goal-setting questions are meant for the app to provide the user information of how much money you need for those goals. The goal headline serves as an incentive to promote regular savings (and investing). For example, for childhood education, if the user indicated his/her child is in age of 7 and wants to study til university in a certain country, the app is able to generate useful information of how much it would cost, in a simple breakdown. Another example, for housing, if the user indicated he wants to buy a house, the app could provide an approximate value based on his chosen location, house size and type.

Clear dashboard of your investment amounts. User can choose the family view option, with which all the family members having connected within the app can view the fund changes and goals progress. Transparency and put financial planning as a family effort. Below is an example dashboard from SG government CPF app. (we draw our own)

Partner with reputable banks or asset management companies to design suitable funds that target this low-income group. The funds are low risk, low funding requirement and high flexibility in withdrawal. Low management fees The fact that they are with well-known financial institutions enables trust.

Insurance and other products From current research it is not apparent that there is huge demand for insurance products among migrant workers. However, our platform is open to the possibility of extension to other financial products.

Currently, there exists several low-cost investment products in the market, such as Singlife Account, GIGANTIQ and Dash EasyEarn, details summarized in the table below. Beside those three, in Dec 2021, UOB asset management and Singtel announced to set up active and passively managed funds on ESG theme with very low investment requirement (S$1). The funds are part of the robo-advisory investment service provided to Singtel mobile wallet platform. Here meant to illustrate the possibility of creating suitable low-cost investment products, and to bring out that, in terms of product structure and return, we would have to ensure the products we offer are competitive in terms of return and fee. Final point is that, as our app is targeting to be a popular app for migrant workers to move funds, the investment products could be made accessible to them much easier.

Singlife Account GIGANTIQ Dash EasyEarn Interest Rate 2% / 1% p.a. 1.8% / 1% p.a. (Note 1) 1.8% p.a. (Note 2) Guaranteed Tenure N/A 1 Year 1 Year Maximum Amount (higher rate) $10,000 $10,000 $20,000 Maximum Amount (lower rate) Next $90,000 Next $190,000 N/A Minimum Amount $100 $50 $2,000 Withdrawal Any amount Any amount ($0.50/$0.70 fee) Multiples of $100 (0.70 fee) Death Benefit (insurance) 105% 105% 105%

Note 1: 1% p.a. Guaranteed for first year + 0.8% p.a. Bonus Note 2: 1.5% p.a. Guaranteed for first year + 0.3% p.a. Bonus Source: Nerfed: GIGANTIQ Reduces Rate to 1.8% p.a For New Sign Ups; How Does It Compare Now? - Sethisfy

Financial educational content

The objectives of setting the content are:

Enhancing financial literacy among low income group is a key step in getting them to adopt financial services with more confidence and trust. It is a way to attract people to use our platform as well.

Features of educational content: A short questionnaire for users to fill in regarding/her financial and digital literacy for the app to recommend education programs of a suitable level and relevance. Content targets both the income-earning individual and his/her family members overseas because financial budgeting and planning should involve all members who earn and spend money within the family. In the form of short videos and concise summarized key points. Available in multi-languages. Some could target kids and teenagers as well to encourage family members' involvement. The education program could provide some form of incentives (points, rewards, discounts) if the person completed them. Topics to cover included at least the following: Financial planning and budgeting Basic financial products and services, such as savings, credits, and insurance Intermediate financial knowledge and investments, such as behavioral biases, forexes issues Remittances Income taxes and government assistance Fraud, scams, and identity theft Introduction to entrepreneurship, how to set up your own business Use of smartphone and digital technologies

Trust

Trust is crucial when it comes to financial technologies. You wouldn't offer your wallet to a complete stranger, and you wouldn't share your financial information with just any digital app. In fact, according to a January 2020 Nerdwallet survey, one out of every five US individuals (21%) does not utilize mobile payment apps. 42 percent of those who don't say they don't trust Fintech applications say it's because they don't trust their security.

AllGrow users are of the same mind. They want to know if they can trust a fintech service before they use it. What protections are in place to ensure the safety of my funds? Will AllGrow make amends if it makes a mistake? Firms are undoubtedly delighted to tell customers about a new feature when it's released. When the news is terrible, transparency becomes more difficult — but also more vital. To address this issue, if AllGrow suffers a security breach, we owe it to your consumers to inform them. Customers deserve to know what data we gather and how it will be used, even if there isn't a data breach.

To further establish our credibility, AllGrow will be pursuing accreditation from the Monetary Association of Singapore. We will also be partnering with DBS Bank. The partnership will be mutually beneficial as DBS is a forward-thinking technologically driven back that seeks to reduce remittance fees to be more competitive. AllGrow’s remittance solution will help reduce DBS’s remittance fees while improving AllGrow’s credibility.

As a large portion of AllGrow’s customer base are foreign workers, we will be establishing offline counters in worker dormitories and a 24/7 customer hotline, serviced by personnel who speak foreign languages. This will help improve trust as the workers would be more likely to choose firms that communicate with them better. Any queries issues they face on the app can also be directly solved by the offline counters.

The new town square is social media. Fintech firms that want to be a part of the debate must make good use of it. Users are more likely to trust firms that make an effort to foster community. Quality material, on the other hand, is required to create an online community. AllGrow strives for a decent balance of text, image, and video content. Fintech is the way of the future, but it still has to attract a large number of new customers. Rather than focusing on regaining trust after it has been lost, AllGrow intends to be proactive in establishing trust early and often.

Customers care about the security measures implemented to protect their data. Even if no money is taken, reclaiming a stolen identity might take years. On our website and social media, AllGrow will emphasize our security features. Customers seeking information are naturally drawn to FAQ sites. Hence, AllGrow will utilize this space to describe our cybersecurity technology, including end-to-end encryption and two-factor authentication, and how it protects AllGrow's clients.

There are parallels among 80 successful Fintech startups, according to a recent analysis that looked at the revenue strategies of 350 Fintech startups that inspire client trust. Among them include companies' increasing willingness to be honest about their price, as well as a greater emphasis on value-added. These Fintech companies demonstrated how their services may make people's lives better.

As a result, AllGrow will be completely transparent about the pricing of our services. Users don't want to be surprised by unexpected charges after only two months of using our technology. allow will explain the whole cost of ownership to consumers and undermine the app's unique selling point. More importantly, AllGrow will describe and quantify the advantages that our app provides to our users, such as the cost savings compared to Western Union.

Compliance

The Payment Services Act 2019 regulates both payment service providers and payment systems in Singapore ("PS Act"). The PS Act requires payment service providers to be licensed in order to perform specific payment services. Payment systems assist the transmission of funds between or among participants, and they may be designated for closer control under the PS Act.

It is against the law in Singapore to operate a money transfer business without a valid license from the Monetary Authority of Singapore (MAS). Domestic money transfer service providers and remittance agents are regulated by the MAS. Larger money transfer service providers (such as DBS) are expected to safeguard the funds the customer had authorized them to move. That implies that the customer should be able to get your money back if the service provider's firm collapses. Small money transfer service providers (such as AllGrow) are not required to protect their customers' funds, but the firm must advise the customers of this fact.

To achieve hypergrowth and not go through the long process of attaining a MAS license, AllGrow plans to take advantage of Singapore’s Fintech Regulatory Sandbox to circumvent current MAS regulations. Blockchain technologies, like cryptocurrencies, are still not completely regulated in Singapore as the law slowly catches up to the rapid changes in the technological landscape. The FinTech Regulatory Sandbox framework allows financial institutions and FinTech firms to test new financial products or services in a live setting, but only for a limited time and in a controlled environment. MAS will give appropriate regulatory support based on the experiment by waiving specified legal and regulatory obligations that the sandbox entity would otherwise be subject to for the duration of the sandbox. The sandbox will include necessary safeguards to contain the repercussions of failure while maintaining the financial system's overall safety and soundness. The sandbox entity must completely comply with all relevant legal and regulatory requirements after successfully completing the experiment and departing the sandbox. Despite being the quickest option, the Sandbox Express option is unavailable for AllGrow. Sandbox Express is no longer available for remittance business as of 7 January 2020, as the Money-Changing and Remittance Businesses Act ("MCRBA") was repealed on 28 January 2020, when the Payment Services Act 2019 ("PS Act") took effect. Thus, AllGrow will be pursuing the standard Sandbox option and then pursuing the MAS license if the sandbox were a success.

Conclusion

AllGrow aims to increase financial inclusion for migrant workers in Singapore with blockchain technology. Our remittance service integrates with the Binance Smart Chain to provide a simple solution for users to transfer money across the borders at a low cost, with fast speed and trusted transactions. We offer an investment service that allows our users to have a higher interest rate for their savings account through the use of the Anchor Protocol. Our goal is to increase the wealth of migrant workers by providing them with these services.

Log in or sign up for Devpost to join the conversation.