algotrade_score

Motivation

From a historical perspective, Mercantilism was prevailing in the 18th century because Great Britain—“The World Factory” accumulated tremendous wealth from heavily relying on exporting and avoiding importing. Trading was not proved effective until Adam Smith’s 1776 classic publication “The wealth of Nations” first introduced the concept of the absolute advantage. After 40 years, David Licardo improved the theory of labor value by detailing the concept of the comparative advantage in his classic publication “The Principles of Political Economy and Taxation”. Under the Richardian model, international trade was proved better off for both nations. Our team aims at algorithmic trading for social good, providing liquidity and eliminate mispricing in the stock market as much as we can. Another reason of the idea is inspired by the book "The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution". We are all fascinated by quantitative finance.

Takeaway

Get equipped with different kinds of programming language and statistic model as well as some classic research paper in interdisciplinary domain.

How we built it

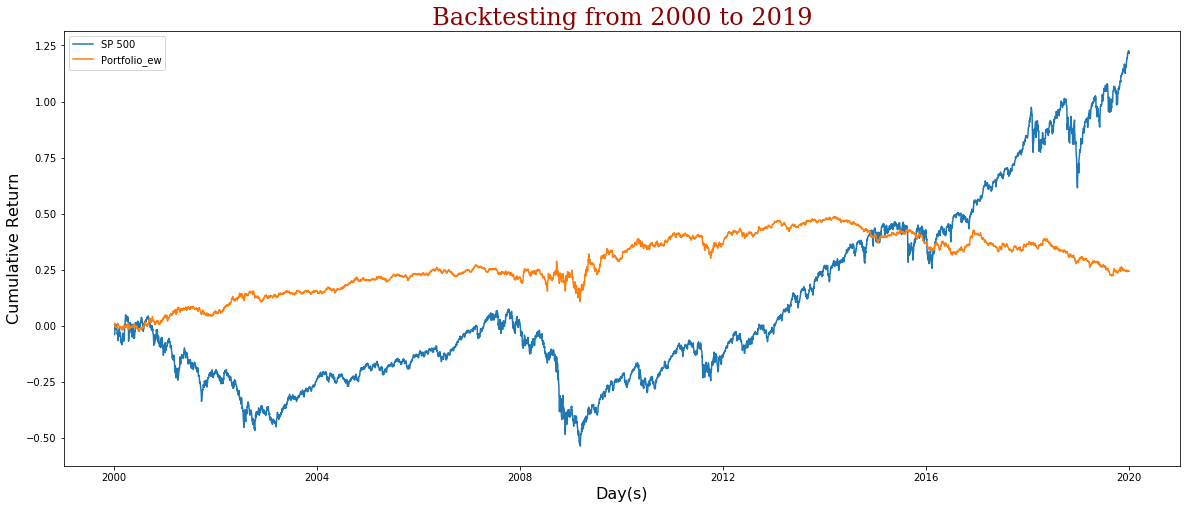

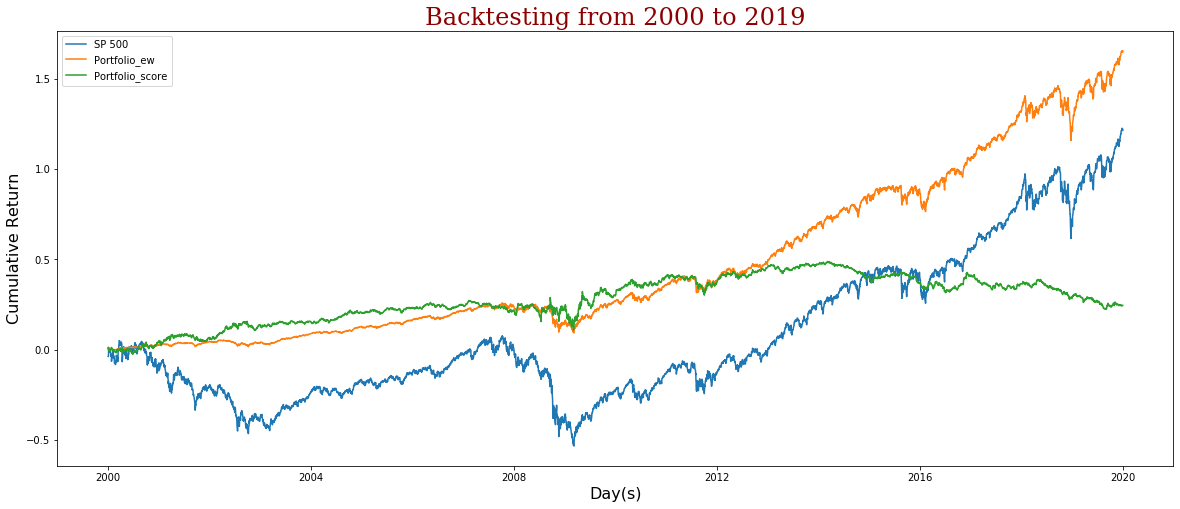

First, we import our factor data from Fama French/Carhart 4 Factors. Second, we use Markowitz's Mean-Variance Optimization Model to identity the optimal weights. Finally, we demonstrate our results via Python and Node.

Challenge

Limited access to API, and not available requests for an available API.

What's next for Algotrade_score

Get financial indicators from 10-K, 10-Q via Bloomberg Terminal as factors. Using Octopus scraping data from seekingalpha.com and implementing sentiment analysis in order to improve the trading stratrgy.

Log in or sign up for Devpost to join the conversation.