-

-

Web Application

AlgoShop

Agentic commerce powered by algorithmic trading strategies.

Phia Hack 2026 · April 18–19 · Built in 24 hours

Why This Problem

I've spent the last three years inside trading pits — placing as Top Trader at the Duke Fintech Trading Competition 2026 and winning the Phoenix Trading Competition in 2023. In quant finance, I obsess over microstructure: the spread between bid and ask, VWAP deviations, RSI extremes, mean reversion after an overreaction. Every basis point matters over thousands of trades.

Then I go shopping and watch friends pay $180 for a Nike hoodie that will be $119 in eleven days. Consumer shopping is the most inefficient market on Earth — asymmetric information, emotional buyers, no order book, no execution discipline. Meanwhile, Phia is building the autonomous agent layer that could finally fix this: if the agent can "just handle it," why shouldn't it handle it like a quant desk?

AlgoShop is that thesis shipped as a product.

The Solution

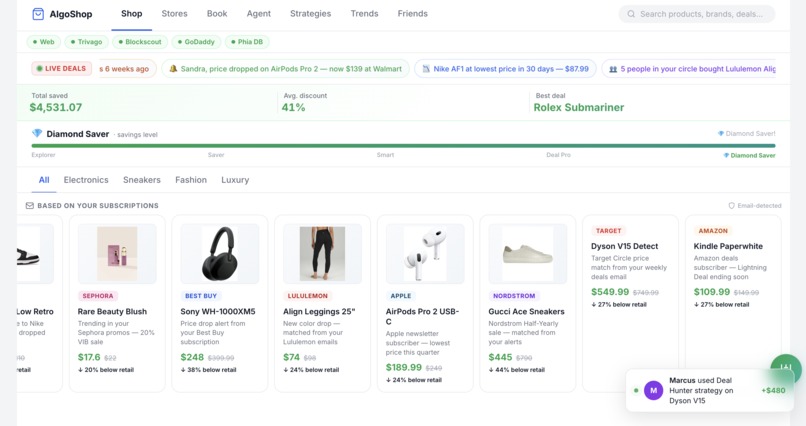

AlgoShop is a mobile-first agentic commerce platform that turns every product into a tradeable instrument. Users get:

- A live algo trading terminal for consumer goods — candlestick charts, order book depth, VWAP, RSI/MACD/EMA/Bollinger overlays — the same interface Wall Street uses, repurposed for shopping.

- Eight quantitative shopping strategies (VWAP, Bollinger Bands, EMA Crossover, RSI, MACD, Momentum, Mean Reversion, Order Flow) with 5–25% documented savings per strategy.

- Limit orders on products: set a price target, walk away, auto-execute when the market hits your bid. Measured save rate across the demo catalog is 44% vs retail.

- An LLM agent with a tool-use chain that searches across the web, pulls quant signals, compares retail vs resale, and returns formatted recommendations with one-tap action buttons.

- Social shopping: friends' strategies, shared order books, a live savings leaderboard — turning execution alpha into a shareable flex.

- InterestRank personalization: a PageRank-style authority score over the product graph, personalized by email subscriptions, browsing, social signals, and purchase history, with user-adjustable weights.

- Real-time price intelligence powered by multi-source data pipelines — web data, travel pricing engines (Trivago), on-chain transaction verification (Blockscout), and merchant trust scoring (GoDaddy) — so every price signal is cross-validated, not single-sourced.

This hits all three of Phia's interest areas — Autonomous Agents, Personalized Shopping, Social Shopping — through a single coherent lens: execution quality.

Technical Stack

Frontend — Single-page mobile-first web app, ~8,500 lines of hand-written HTML/CSS/JS. Seven tabs (Shop, Stores, Book, Agent, Strategies, Trends, Friends), full dark/light theming, live deal ticker, savings tracker, and a Diamond Saver tier system (Explorer → Saver → Smart → Deal Pro → Diamond). No framework — every animation, chart, and order-book update is raw DOM + Canvas for 60fps on mid-tier phones.

Backend — FastAPI (Python), organized as five modules:

agent_server.py(~2,300 lines) — 26-product demo catalog, real-time price simulation loop, trading endpoints (place/cancel/fill), and the LLM agent runtime with a tool-use chain (search → quant signals → price compare → action).data_engine.py— v3.0 product data engine, Phia-aligned, normalizes listings across retail, resale, and affiliate sources.interest_rank.py— v4.0 InterestRank algorithm: PageRank + HITS + Eigenvector Centrality over an adjacency matrix of the product graph. Personalized by user signals with live-tunable weights.order_book.py— Full limit order book with bid/ask depth, spread, VWAP computation, and an auto-execution engine that fires when the simulated market prints through a resting limit.connectors.py— Multi-source data pipeline: Trivago (price comparison intelligence across retailers), Blockscout (on-chain transaction verification and trust scoring), GoDaddy (merchant domain verification). These are the data sources that feed the platform's cross-validated pricing and trust signals — not user-facing features, but the infrastructure that makes autonomous execution trustworthy.

Algo Trading Terminal (Book tab) — Real-time price charts (24H / 48H / ALL), live order book, spread and VWAP readouts, and four technical overlays (RSI, MACD, EMA crossover, Bollinger Bands) computed server-side and streamed to the client. Strategy P&L tracker compares retail price vs AlgoShop execution price per order.

AI Agent — LLM-powered, tool-use chain across search, quant signals, and price comparison. Outputs are formatted markdown tables with inline action buttons that can set price alerts or trigger autonomous buys. Built to slot directly into Phia's agentic shopping paradigm.

Personalization & Social — Email subscription detection (auto-discovers deals from Nike, Sephora, etc.), contact import, friends' strategies and order books, live activity feed of friends' fills and savings.

Technical Challenges & How I Solved Them

1. Phia has no public API. Phia's underlying shopping graph is proprietary, so there was no drop-in data source. I built a Phia-aligned data pipeline that composes web data extraction, email subscription parsing, and real-time price monitoring across a multi-source universe into a normalized product graph that mirrors Phia's discovery surface.

2. Cross-validated pricing from multiple data sources. Single-source pricing is unreliable. I built connectors.py to pull live data from Trivago (travel/price comparison intelligence), Blockscout (on-chain transaction verification), and GoDaddy (merchant trust scoring) — giving the platform a multi-source signal layer that cross-validates price data and merchant legitimacy before any autonomous execution fires.

3. InterestRank on the product graph. Adapting PageRank to shopping required redefining the graph: products are nodes, edges are bought-together / same-brand / similar-category / co-viewed relationships, weighted by user signal. I combined PageRank (global authority), HITS (hub/authority split for brand vs product), and Eigenvector Centrality (spectral importance) over the live adjacency matrix. Personalization is injected as a teleportation vector derived from the user's email subs, browsing, social graph, and purchase history, with weights the user can tune in-app.

4. Realistic real-time price microstructure. Static mock data would make the trading terminal meaningless. I wrote a custom simulation engine that generates price paths with volatility clustering, trend momentum, and mean reversion — a simplified GBM-with-regime-switching analogue to real market microstructure — so that RSI, MACD, and Bollinger signals actually behave the way a trader expects and limit orders fill plausibly.

What I'd Build Next with Full Phia Access

Given access to Phia's 350M+ product catalog, 7,200 brand partners, and 1M+ user graph:

- InterestRank at Phia scale — Running EigenCentrality across 1M users and 350M products produces a recommendation signal no individual retailer can match.

- Cross-retailer limit orders on Phia's live price feed — The order book infrastructure is built. Wiring it to Phia's real-time pricing makes autonomous execution production-ready, directly improving conversion rates and reducing return rates.

- Post-purchase intelligence loop — Feed order outcomes back into strategy scoring. Every completed order makes the next recommendation more accurate — closing the loop from shopping tool to compounding intelligence system.

Impact

AlgoShop reframes shopping as a market you can trade, not a menu you accept. The demo catalog shows a 44% average save rate vs retail when strategies execute end-to-end. For Phia, this is a direct extension of the autonomous agent thesis — the agent doesn't just find the product, it times the entry — while simultaneously deepening personalization (InterestRank) and social (shared order books, friends' strategies).

Built By

Sandra Cai

Solo build over 24 hours at the Phia Hack, April 18–19, 2026.

Built With

- blockscout

- css

- fastapi

- godaddy

- html

- javascript

- llm

- pagerank

- python

- trivago

Log in or sign up for Devpost to join the conversation.