How I built it:

I built the backtesting infrastructure for the Fibonacci geometrical pattern strategy using a combination of Python and C++. Here's an overview of the steps and technologies used:

- Research: Started by thoroughly researching Fibonacci geometrical patterns and understanding the psychology behind them in financial market analysis. Gathered historical financial data for testing.

- Python: Utilized Python for data preprocessing, visualization, and strategy development. Popular libraries such as Pandas, Matplotlib, and NumPy were employed to handle data and create visual representations of patterns. C++: Employed C++ for performance-critical components of the backtesting infrastructure. C++ is well-known for its speed and efficiency, making it ideal for handling large datasets. Backtesting Engine: Developed a backtesting engine that could simulate the execution of the Fibonacci geometrical pattern strategy over historical data.

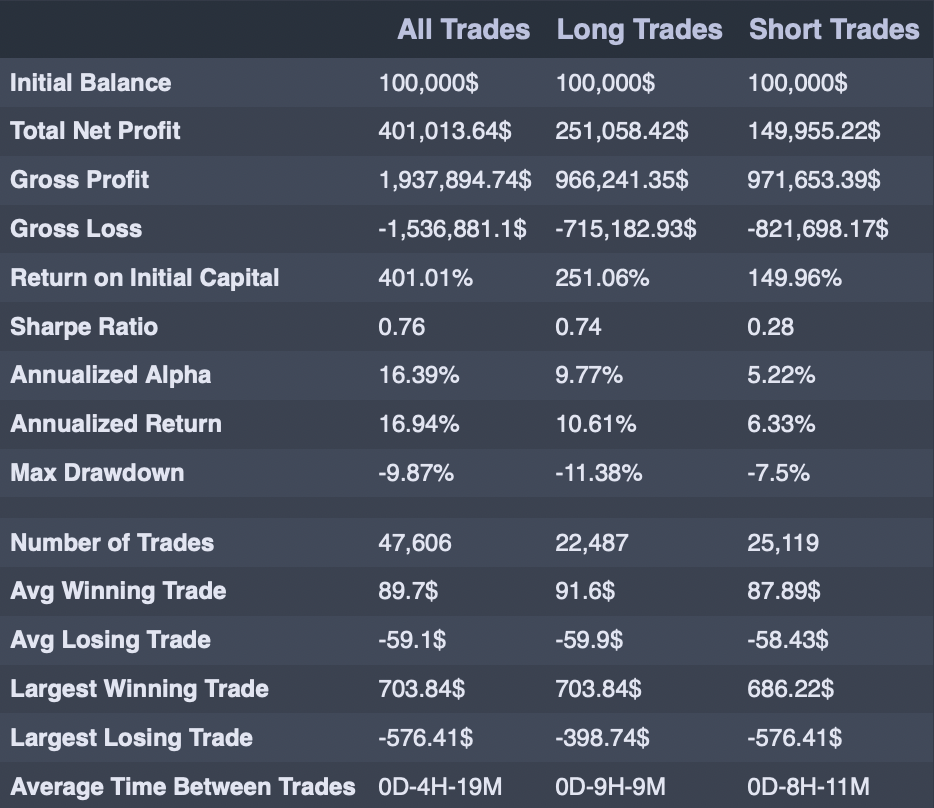

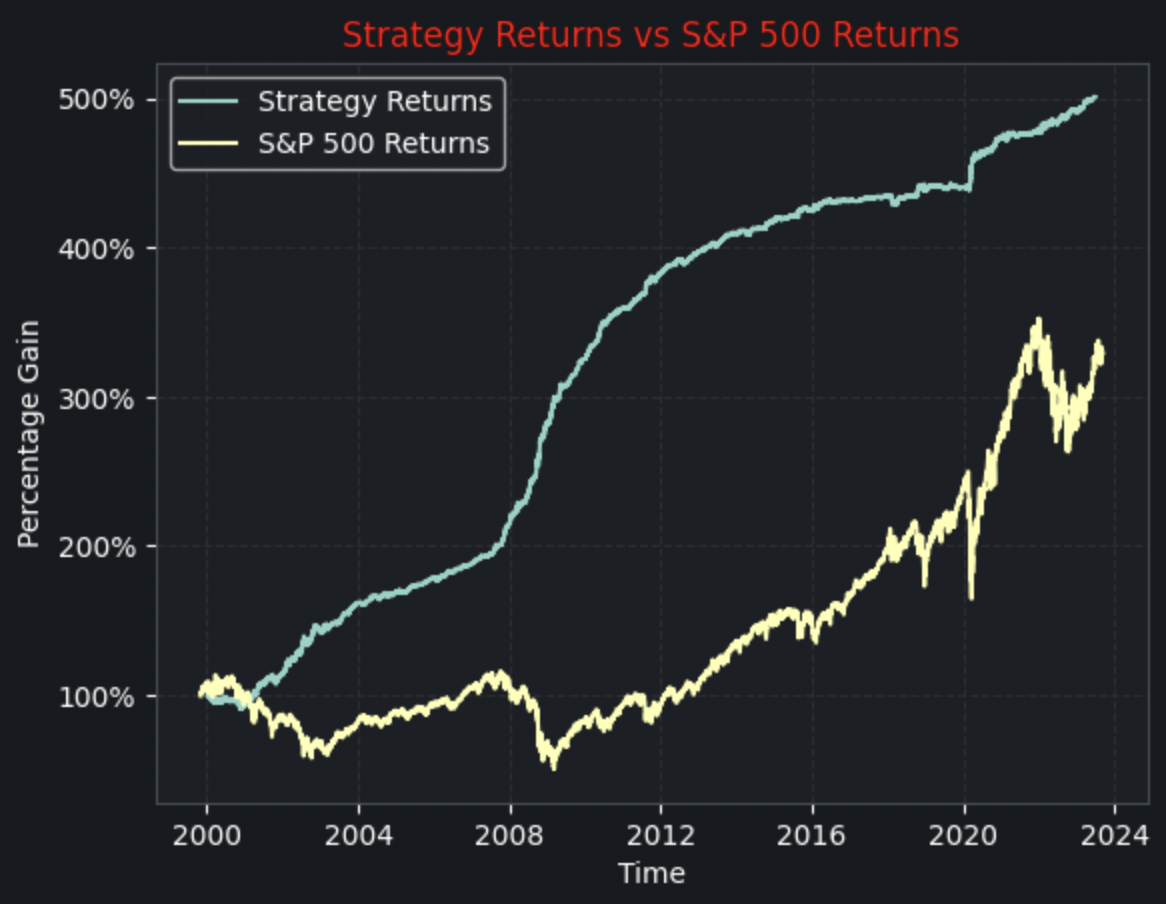

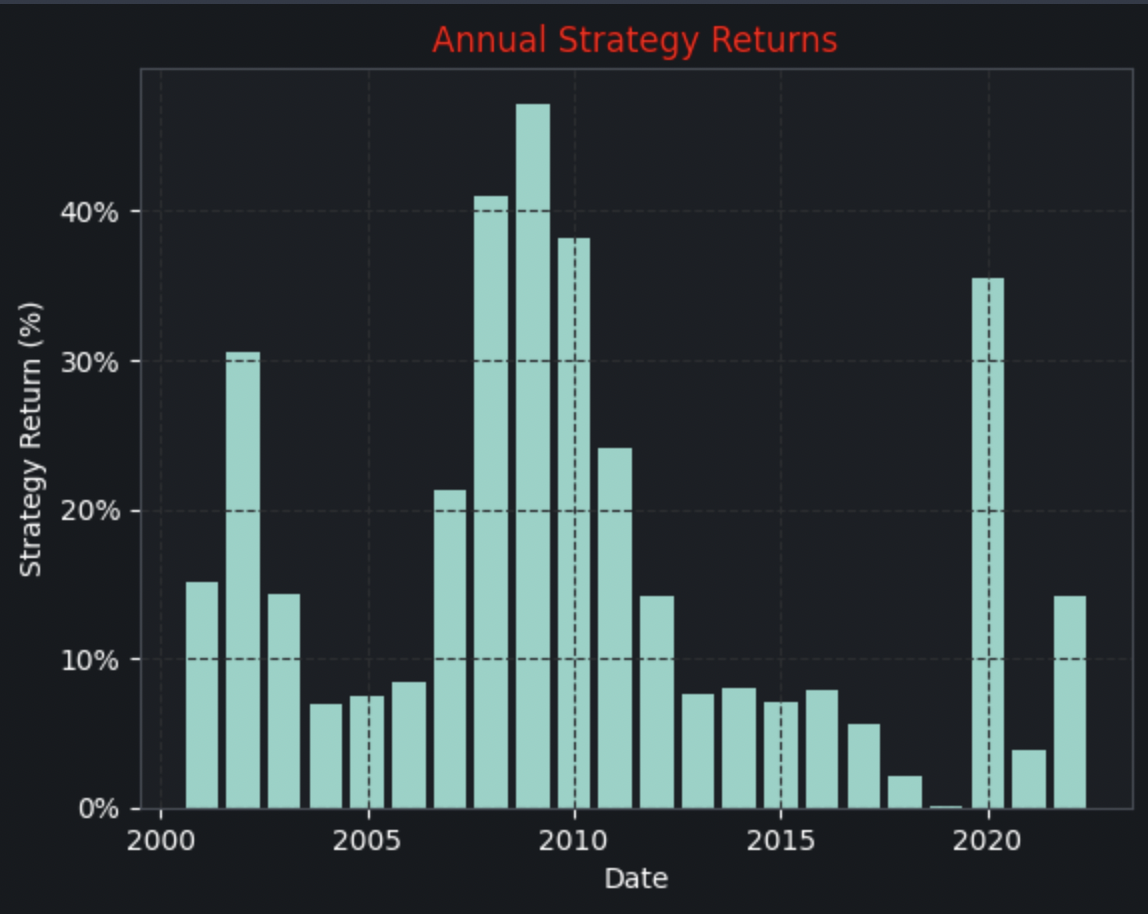

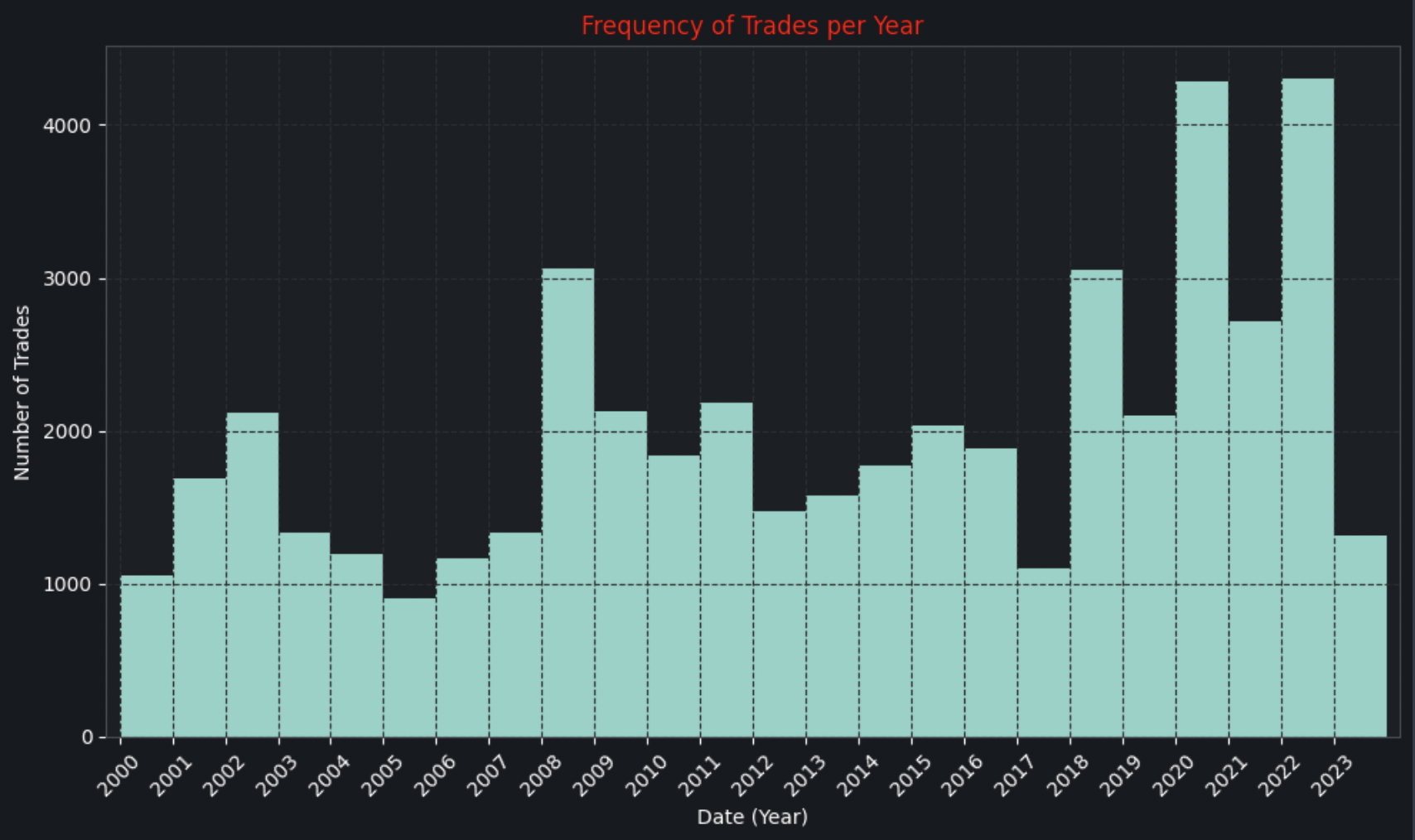

- Data Management: Ensured proper data management, including historical price data, economic indicators, and other relevant information. Data was acquired through the Alpha Vantage API Visualization: Created visualizations to analyze the strategy's performance, including the alpha return, the Sharpe ratio, trade frequency, drawdowns, and risk metrics. Psychological Aspects: Incorporated psychological factors into the strategy, such as recognizing trader behavior influenced by Fibonacci patterns.

Challenges I ran into: Building an algorithmic trading system involves numerous challenges, including:

- Data Quality: Ensuring accurate and clean backtesting data. Dealing with gaps, outliers, and data anomalies can be challenging while avoiding overfitting of data.

- Performance: Optimizing the code for speed and efficiency, especially when dealing with large datasets, can be complex.

- Risk Management: Developing robust risk management techniques to protect against significant losses.

- Psychological Factors: Integrating human psychology into the strategy and accurately simulating trader behavior can be tricky.

- Backtesting Accuracy: Achieving realistic backtesting results that accurately represent real-world trading conditions can be challenging.

Accomplishments that I'm proud of:

I'm proud of the following accomplishments:

- Successful Backtesting: Developing a backtesting infrastructure that accurately simulates the Fibonacci geometrical pattern strategy's performance over historical data.

- Data Visualization: Creating visually appealing and informative visualizations to analyze the strategy's performance and gain insights.

- Psychological Insights: Incorporating psychological aspects into the strategy, which adds depth and relevance to its analysis.

- Empirical Data: Providing empirical data that contributes to the debate surrounding the effectiveness of Fibonacci strategies in financial market analysis.

What I learned:

Through this project, I learned:

- Algorithmic Trading: Gained a deep understanding of algorithmic trading, including strategy development, backtesting, and risk management.

- Python and C++ Integration: Gained experience in integrating Python and C++ for more efficient and high-performance trading infrastructure.

- Market Psychology: Enhanced knowledge of trader psychology and how it influences trading decisions. Data Handling: Developed skills in managing and preprocessing financial data.

What's next for Algorithmic Trading Using Fibonacci Geometrical Patterns:

The future of this project could involve several directions:

- Live Trading: Transitioning from backtesting to live trading, where the strategy is executed in real-time with real capital. This requires careful consideration of risk management and regulatory compliance.

- Machine Learning: Exploring the use of machine learning techniques to improve the strategy's performance and adapt to changing market conditions.

- Further Research: Continuously researching and refining the strategy to incorporate new insights and market dynamics.

- Community Engagement: Sharing the project's findings and insights with the trading and financial community, potentially through publications or presentations.

Built With:

- Python (Pandas, Matplotlib, NumPy)

- C++

- Financial data APIs provided by Alpha Vantage

- Algorithmic trading libraries and tools

Log in or sign up for Devpost to join the conversation.