Inspiration

- For me trading is a mix of strategy, psychology and risk management. Strategy warrants significant data analysis for insight generation. Scanning through data is a cumbersome process and so is extracting insights. Automating this process can enable traders to create enhanced strategies, improve their psychology and risk management, eventually becoming a better trader.

What it does

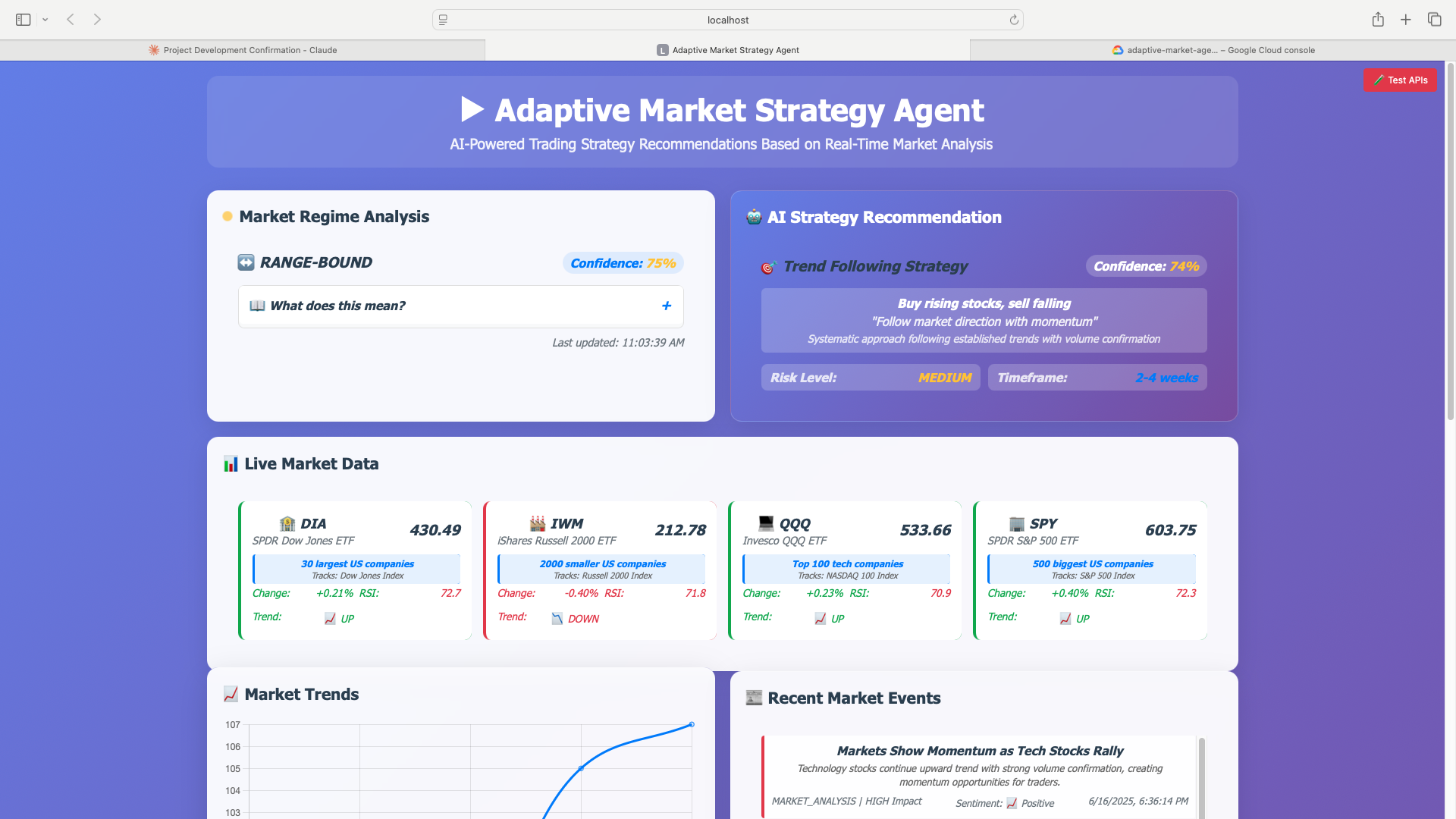

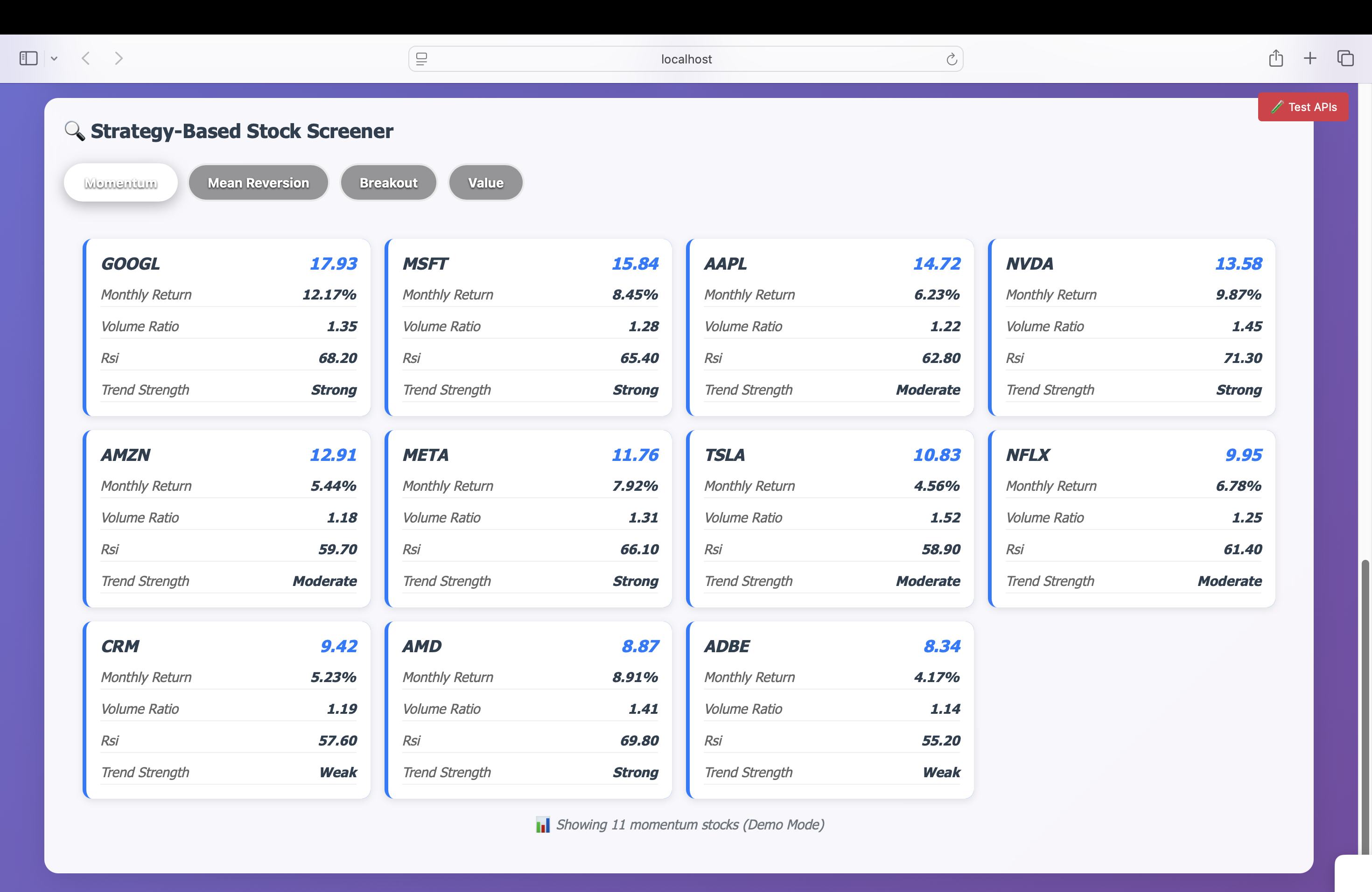

Our agent continuously analyzes market conditions and dynamically recommends optimal trading strategies based on real-time data. The strategies recommended are basis the risk profile of the trader and can be preset or customized as per the trading strategy of the trader. It can be simple or nuanced basis the type of the trader. ITs core functionality includes real time market analysis, market regime detection (AI, guided with rules), dynamic strategy matching to market conditions, live stock screening (strategies like momentum, breakout etc.), with built-in risk management. **PS : For the sake of hackathon demo, I have added dummy data, which can easily be replaced with live feeds from Alphavantage and Yahoo Finance

How I built it

This tool is built using FastAPI and MongoDB Atlas for data storage with vector search capabilities. The system integrates Alpha Vantage and Yahoo Finance APIs for real-time market data, processing four major ETFs (indicative of indices like NASDAQ, DJIA etc.) every five minutes. Core AI engine uses custom algorithms for market regime classification and strategy matching. MongoDB's vector search enables historical pattern matching for similar market conditions. The scalable architecture is designed for Google Cloud deployment with Cloud Run for serverless scaling. Built with Python, it has HTML/JavaScript frontend with Chart.js visualizations. Environment variables ensure secure credentials, while comprehensive APIs enable seamless integration and future institutional-grade enhancements.

Challenges I ran into

Data integration was a challenge with multiple data formats from open source data sources. Market regime classification needed extensive algo with preset confidence limits.

Accomplishments that I am proud of

- Stock screening performance - 50+ stocks processed under 30 seconds (plan to further scale this for institutional grade processing capabilities)

- Market regime classification has proven effective over last 5 days of testing since I have built it.

What I learned

Real-time financial data requires proper error handling, effective credential management, and scalable architecture design.

What's next for Adaptive Capital Markets Agents

- Building risk analytics and performance tracking for retail

- Adding more stock screeners and further granular market regime classification with more parameters

- Refining strategy, risk management and data processing to level it up for institutional trading grade

- Adding derivative trading strategies, cyptocurrency trading strategies and other advanced ones

Built With

- alphavantage

- fastapi

- gcp

- html

- javascript

- mongodb

- newsapi

- python

- yahoofinance

Log in or sign up for Devpost to join the conversation.