-

-

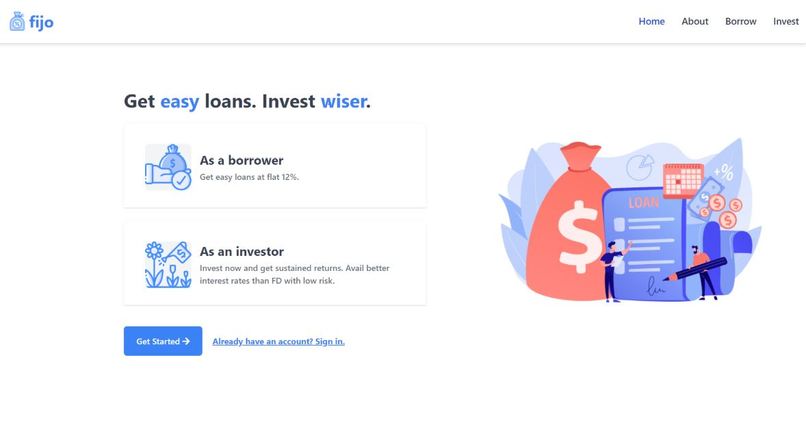

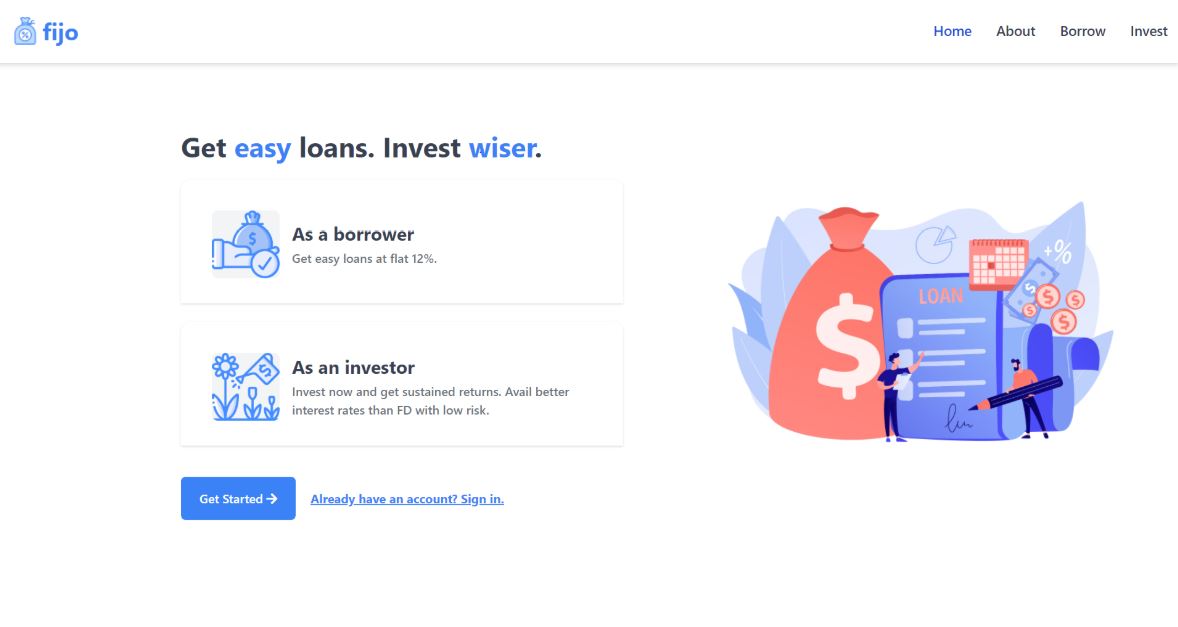

FiJo page

-

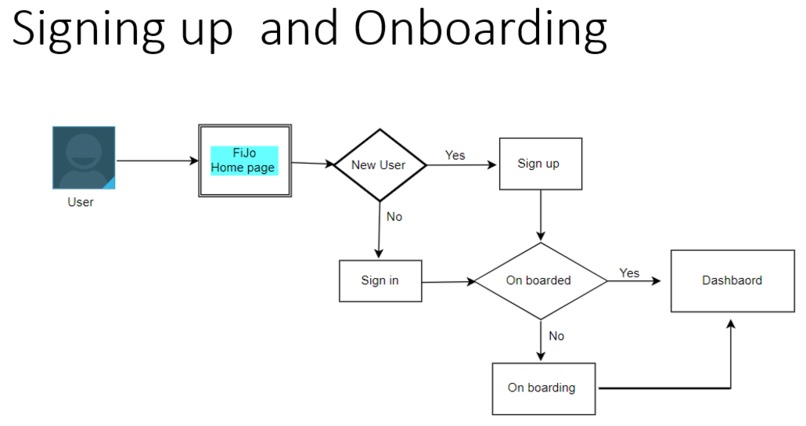

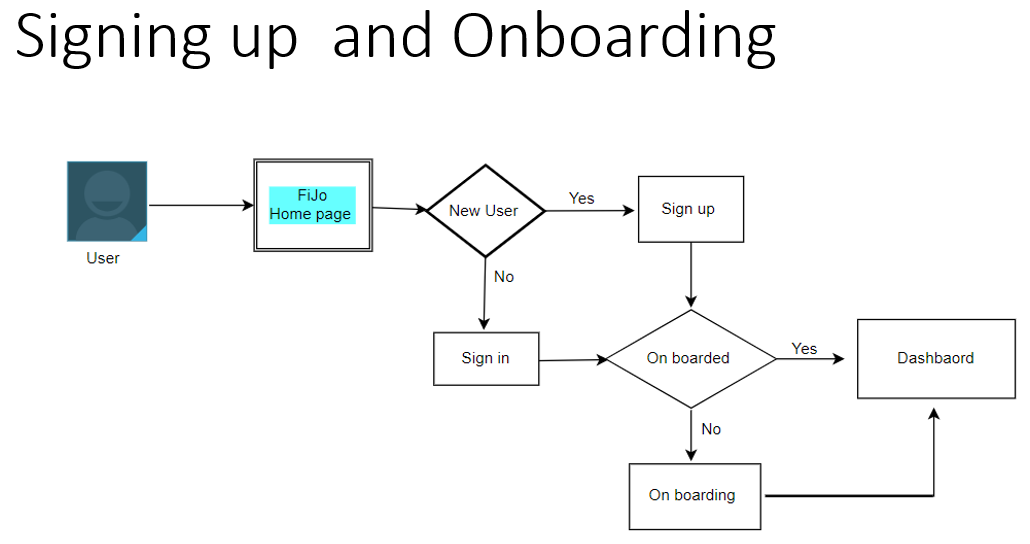

Signing Up and Onboarding process flow

-

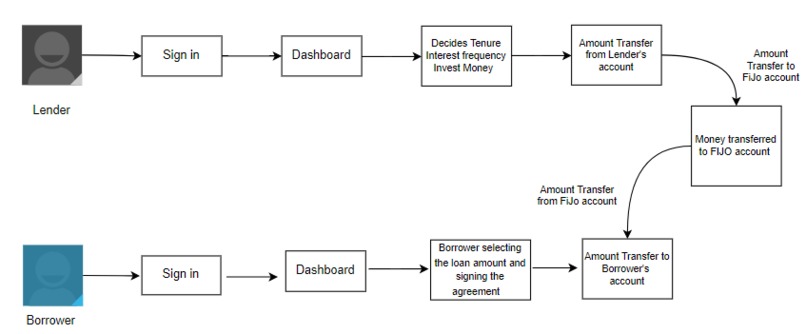

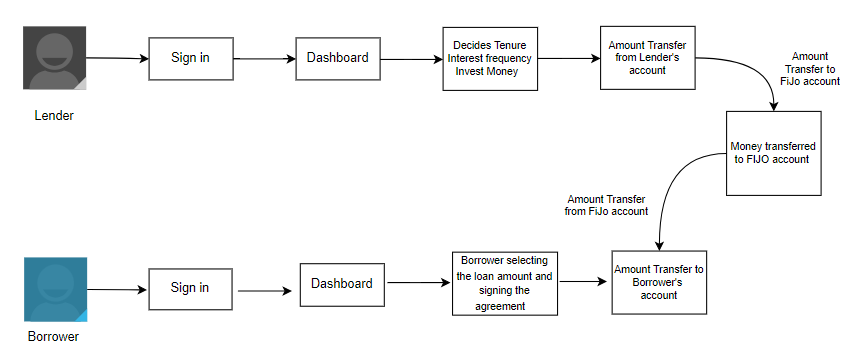

Loan process

-

FiJo Functionalities

-

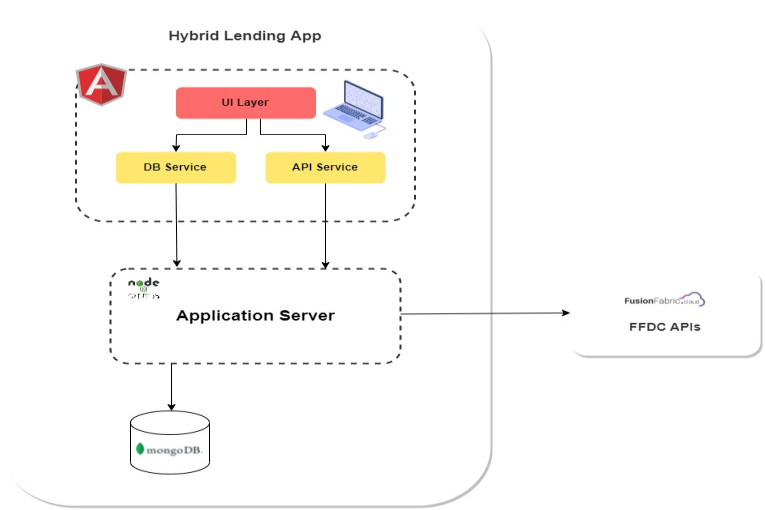

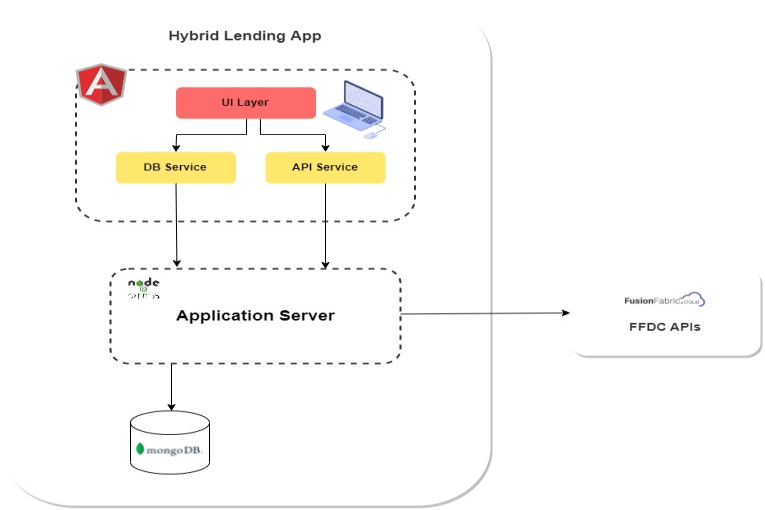

Technical Architecture

Inspiration

As per the CNBC report, more than 60% of credit loans were denied in 2019. Thus creating a huge imbalance and no access to people even though they have a good CIBIL score. This made the people look for alternative loans from NBFCs, SFBs, and non-registered lenders to avail of the loan at very high-interest rates touching whooping around 30%- 40% ROI at times. So we wanted to break the current system.

What is Fijo

Fijo is a hybrid retail lending model that is a win-win situation for both borrower and lender while ensuring seamless user experience, easy loan approval, and relief from traditional banking process hassles. In the proposed Hybrid model the parties involved are individuals, NBFC, NRIs, NGOs, and small finance banks as lenders and salaried individuals as borrowers. We provide a single platform to disburse loans and provide good returns to the lenders alternative to FDs and stocks at a flat 12% ROI.

How we built it

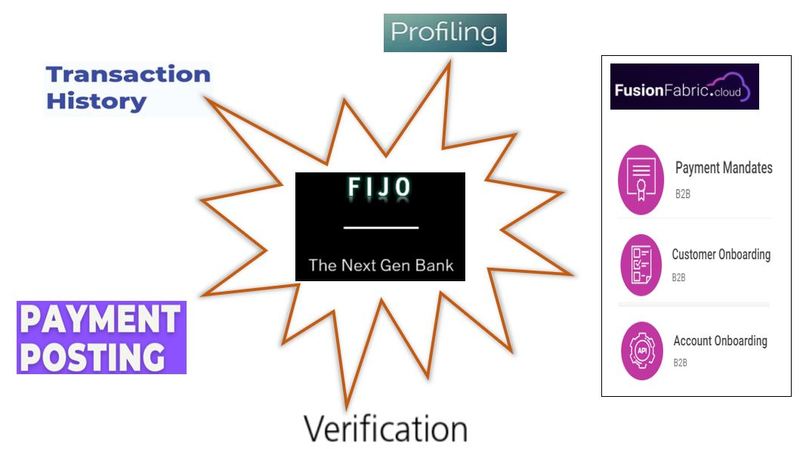

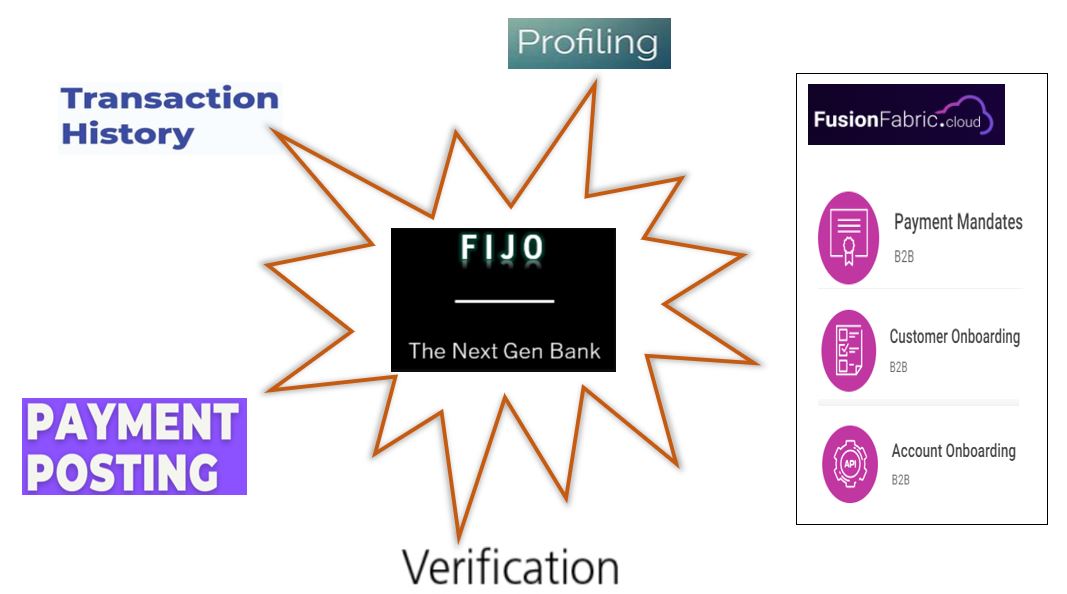

We have leveraged Payment Mandates from Fusion Essence, Customer Onboarding from Fusion Essence, Account Onboarding from Fusion Cash Management APIs from FFDC. Used MongoDB, express, angular, and node.js(MEAN stack) for the application.

Challenges we ran into

We couldn't find most of the fields for the project as part of the available API schema. Response time for customer onboarding API calls was very high.

What's next for Fijo - Hybrid Lending Model

We would expand Fijo to everyone not just to salaried individuals, and we would love to expand this to all underdeveloped, and developing countries.

USP of Fijo - Hybrid Lending Model

Every salaried individual should be getting access to loans without any biases (irrespective of CIBIL score, locations, and employer).

To provide loans at an affordable rate of interest (flat 12%).

Loans should be approved very fast and easier with the ease of digital intuition.

Greater flexibility in loan repayments.

To provide the best alternative to FDs and stocks for lenders.

Better UI and user experience

Log in or sign up for Devpost to join the conversation.