Inspiration

The idea for 401a(llowance) originally came out of an interview where I was put on the spot to come up with a product idea that would help children save more, and I came up with the idea to create what is essentially a 401(k) system but for an allowance. The goal is to teach the value of delaying gratification by "matching" contributions from a weekly allowance that are placed into a savings account. This allows the child to get more allowance each week by promising a certain percentage of that money to their savings account.

How it works

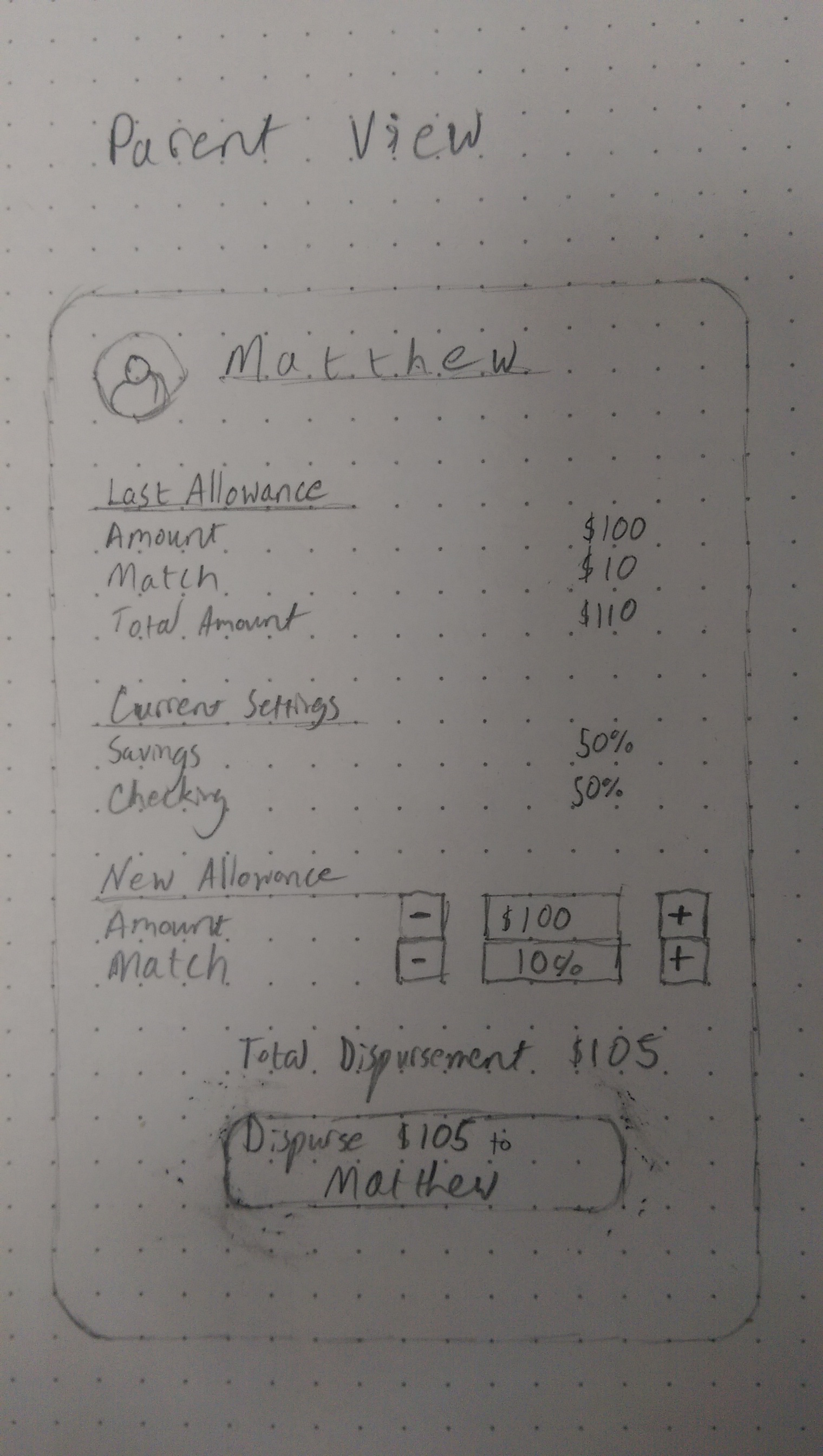

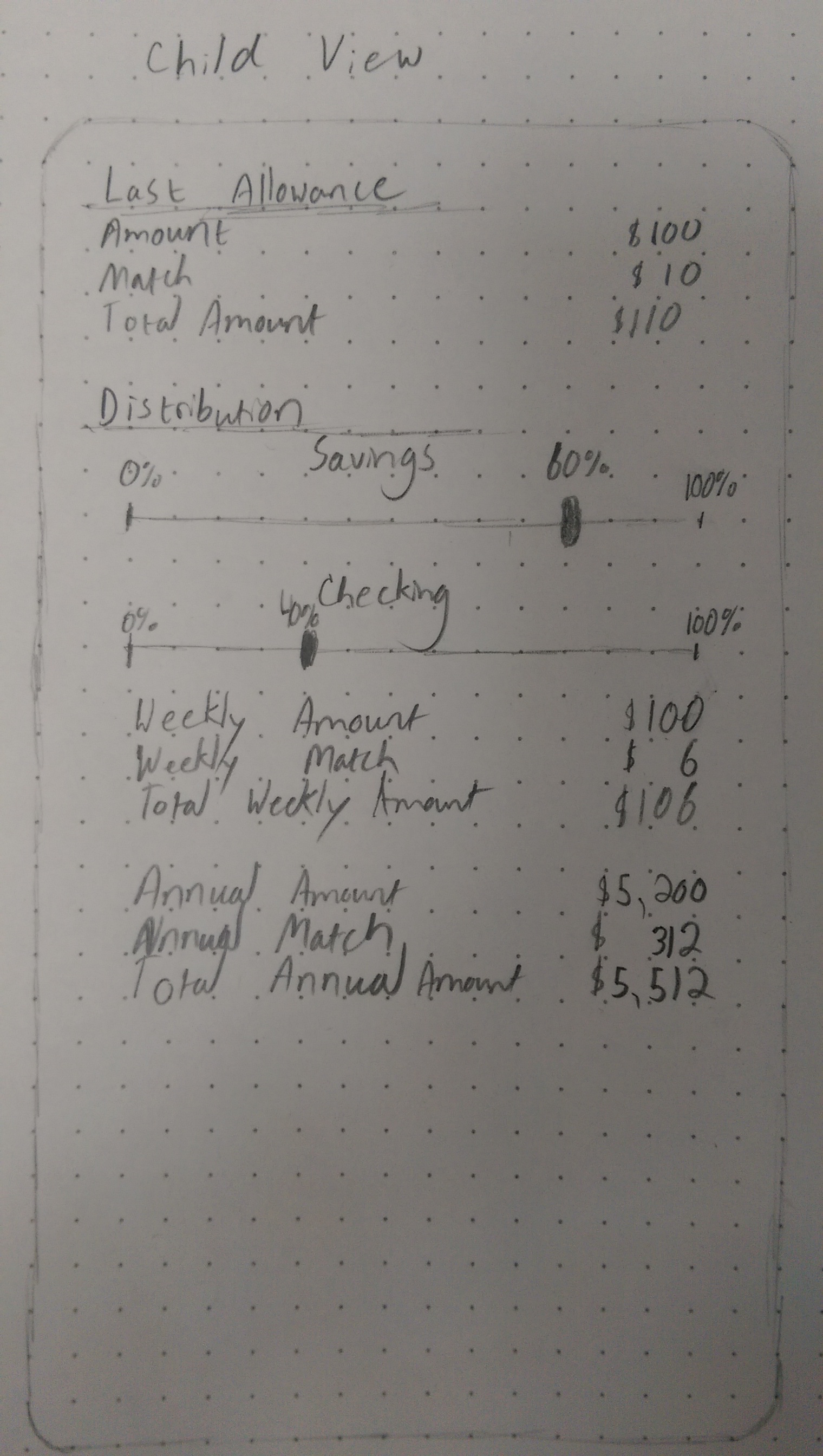

Well technically speaking, it doesn't work yet. It's just a couple of sketches and an idea. The way I envision it working is that parents and children would both install the applications on their devices. Children would be presented with a slider that would allow them to decide what portion of their allowance would be diverted into their checking account as spending money and what portion of their allowance would be diverted into their savings account. Similar to a 401(k), a certain percentage of portion diverted to savings would be matched by the parent, allowing the child to earn more than their typical allowance amount.

Here is a simple example to illustrate. Let's say that the child's weekly allowance is $100 (it's been a while since I received an allowance and I have no idea what a normal allowance is these days). In this example the parent allows for a 10% match of savings contributions, and the child chooses a 60/40 split between savings and checkings. This means that the child would receive $106 each week, with $60 + ($60 * 0.10) = $66 going into their savings account, and $40 going into their checking account. Over the course of one year, the child would have earned $60 x 52 = $312 in additional allowance by choosing to delay their gratification.

Difficulties I ran into

Since I haven't actually built anything yet, the only difficulty so far is thinking through how to prevent gaming of the system. Since funds can easily be transferred between checking and savings accounts, and recurring payments and other expenses can easily be set up to come out of savings accounts, there is no way to really enforce that the "savings match" from the parent is actually rewarding delayed gratification. One possible solution to this problem would be to use the funds that are matched to purchase an investment that would make it undesirable to cash out in the short term. An example of this would be purchasing a $25 government savings bond that wouldn't be able to be cashed for a year. This really only works for large allowances since it would take a few weeks for the "match" to add up to enough money to purchase these investments. If micro-lending becomes a viable option through things like Bitcoin, then it would be possible to invest the "match" no matter how small it is (allowing the compounding effect to kick in sooner).

Built With

- paper

- pencil

Log in or sign up for Devpost to join the conversation.