Background: What defines a labor shortage?

Labor shortages occur when employers believe that there are insufficient qualified candidates to fill open positions, and thus the supply of workers is less than the demand. According to the U.S. Government Accountability Office, a labor shortage is hallmarked by a low unemployment rate, and significant increases in pay and hiring. ATP certified pilots currently enjoy an unemployment rate of just 2.7%, far less than the national average (Withrow & Azam, 2017). Additionally, in the past 12 to 18 months, regional airlines have increased the hourly pay of pilots from 50% to 100%. This is coupled with new signing and retention bonuses, commonly ranging from $10,00 to $20,000 across regional airlines. In a recent interview, Piedmont Airlines CEO Lyle Hogg confirmed, “I think [these bonuses] are going to be permanent because of the demand in the industry” (Epstein, 2016). The sudden upsurge in regional pilot pay paired with a minimal unemployment rate makes a strong case for a labor shortage: there aren’t enough pilots to fill these positions at regional airlines (Dillingham, 2014).

What are the causes of the pilot shortage?

The reasons for the imminent pilot shortage are complex and nuanced. On one hand, the hiring of pilots tend to occur in cohorts. In times of economic growth, the airline industry expands to fill the economy’s increased demand and as a result hires more pilots, but then not hire more pilots until the next period of sustained economic growth. Because there is a hard maximum age to work as a commercial airline pilot at 65, these cohorts tend to retire en masse. As a result, retirement happens in waves, with the current wave projected to peak in 2021. In fact, over the next 10 years, more than 40,000 commercial airline pilots, representing over 35% of employed airline pilots, will retire (Bureau of Labor Statistics, 2016). This is coupled with the projected growth of air travel, necessitating an additional 100,000 pilots in the U.S. over the next 20 years, and an additional 515,000 additional pilots worldwide (Boeing, 2016). This creates additional pressure on U.S. airlines, as newly trained pilots are wooed by lucrative offers overseas, particularly in East Asia. To make matters worse, one of the historically primary suppliers of highly trained pilots, the military, is also overhauling efforts to retain pilots, paying a premium to keep pilots employed. Before 2001, over 70% of commercial airline pilots were ex-military, contrasted with just 30% today (Government Accountability Office, 2014). In short, airlines are being squeezed from both sides: a large group of pilots is on the verge of retirement, and the usual streams of new aviators aren’t producing numbers sufficient to sustain the economy’s growing demand for air travel.

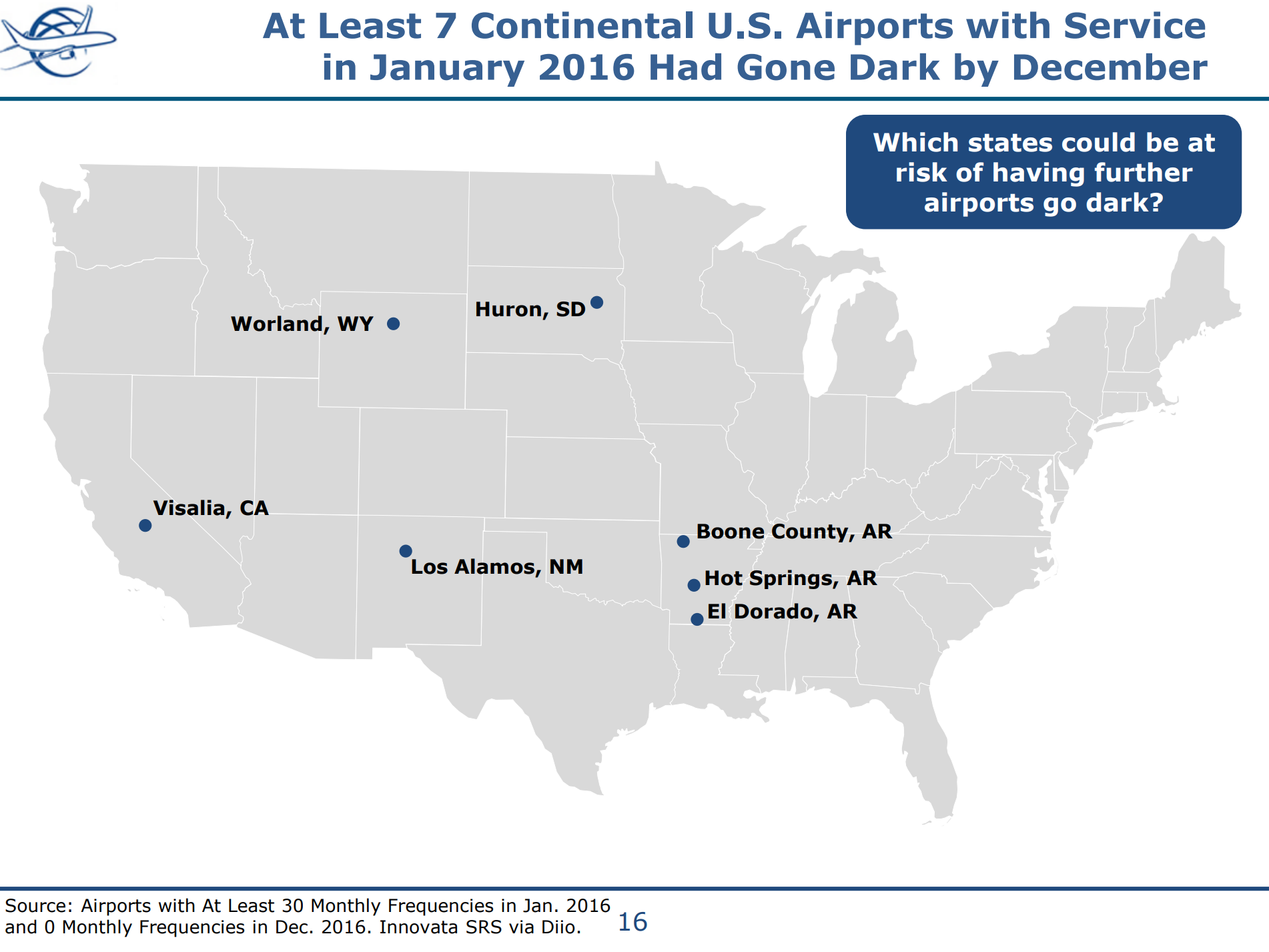

How does the shortage affect regional vs. major airlines?

The current shortage of pilots is not a true shortage. Rather, it is a manufactured shortage, induced by major airlines’ attempts to maximize profits, at the expense of regional airlines. The resultant pilot shortage will be felt by major airlines eventually, but regional airlines will bear the brunt of the economic backlash and are in greater danger of bankruptcy due to the shortage than the major airlines are. Due to the projected shortage, as many as 1,500 aircraft, representing 65% of the regional fleet, may be grounded (Sunderman, 2017). The reason for this is twofold, and both the major airlines and unions are to blame. On the part of the unions, negotiations tend to be led by more senior captains and so their interests are prioritized. As a result, seniority is respected as law. More senior pilots command higher salaries, not only because they demand the longer more lucrative routes, but also because they fight to keep the disparity between new and senior pilots high. This leads to a strongly skewed income distribution: new pilots can expect starting salaries between $20,000 and $50,000, meanwhile senior pilots command salaries topping off at over $500,000. Because of this, the major airlines are primarily composed of senior pilots flying longer routes. From the major airlines’ perspective, it doesn’t make sense to put more experienced pilots on the shorter regional flights. Consequently, regional airlines are composed almost exclusively of new pilots logging hours before bidding up to the major airlines where there’s more room for job growth. For this reason, the pilot shortage is expected to disproportionately affect regional airlines.

What are the current barriers to entry?

The price of certification is currently the largest barrier preventing the training of more pilots. From start to finish, it can take 6-8 years and north of $200,000 to become fully certified. Even after a commercial license is obtained, regulation introduced after the 2009 Colgan crash requires pilots to log as many as 1,500 hours before receiving their Air Transport Pilot License. Once the ATP license is obtained, however, it’s still highly unlikely to be hired by one of the major airlines, and so pilots must start at smaller regional airlines, making $20-$40 an hour. Whereas pilots in the past commonly were trained through the military, today’s new pilots must pay for this training out of pocket, oftentimes taking out exorbitant loans with no guaranteed ability to pay these loans back for many years, and for many this is prohibitory to entry. There are additional barriers to entry as well. For one, the licensing process and the roles of a pilot are not commonly known, and so many will never consider being a pilot as a career because the path to employment isn't clear. Another concern for many younger prospects is the looming “threat” of automation: it isn’t clear what jobs will be able to be automated, and so many that would be interested turn to engineering or other similar fields where the starting salaries are higher and the job security greater. Solution: “America Takes Flight” Fellowship

The What:

A fellowship to help subsidize the training costs associated with flight school and lower the attrition rate once in flight school

The Who:

The U.S. Government, Major and Regional Airlines, Prospective Pilots

The Where:

Airports where training facilities already exist

The How:

The Department of Transportation works in conjunction with both major and regional airlines to develop a fellowship program that would help subsidize the cost of flight school, one of the key barriers to entry. The Department of Transportation would provide half the funding, with commercial airlines providing the other half. Once selected for the fellowship, cadets would be required to agree to a multi-year service contract to work for a U.S. based airline. This has three key benefits: lowering the attrition rate (1 in 10 who start flight school actually become pilots), stemming the loss of U.S. pilots to foreign airlines, and bidding down the labor cost of new pilots under conditions of high demand due to established relationships. Regional airlines would get primary jurisdiction over training centers in their “watershed,” building an established program and reputation at each facility, much akin to a “Top Gun for Commercial Aviation.”

The Why:

The economic infrastructure that airlines provide is invaluable, and is recognized as a common good. As such, the government has invested interest in maintaining the pilot supply. This isn’t uniquely under the government’s jurisdiction, however, and for real change to occur, both major and regional airlines must work together to find a solution. While each airline could train their own pilots, shouldering the cost of training candidates with little to no aviation experience or background, as is the dominant system in Europe, it would requires each airline to develop their own training program, which burdens airlines with high initial costs. Instead, a more robust solution that takes advantage of already existing infrastructure would be a fellowship program, subsidized jointly through government funds and commercial airlines. The fellowship would fund much of the cost of flight school, mitigating a key barrier to entry. This arrangement is uniquely beneficial to all parties involved: the government keeps plane ticket cost low, which increases travel, which helps drive the economy. The regional airlines get a constant supply of new pilots, which they can build a relationship with over the course of their training, and then use that training as a pipeline into the company without having to compete with other companies, bidding down the high-demand prices. The major airlines benefit by evening out the distribution of new pilots and hires, avoiding waves of retirement like the current situation. This framework of training pilots as a collective is a paradigm shift from the dominant flight training regime of the past 50 years: instead of relying on the military to provide flight training at no personal cost to the aviators, the airlines must now work with the pilots and government to dampen the economic burdens of flight school to reinvigorate public interest in piloting and to lessen the shortage conditions in which the airlines currently find themselves.

Feasibility: Projected Costs

Of the 100,000 additional pilots the Boeing report claims are necessary over the next 20 years, 50,000 may be covered by the fellowship. This means 2,500 new pilots would be subsidized each year. If the fellowship, on average, payed for half the cost of flight school, and the government provided half of the available funding, then the total expenditure on the government’s part on a yearly basis comes out to $25 million, with commercial airlines providing an equal part. Within the Department of Transportation, similar subsidies to support and maintain the wellbeing of airline infrastructure such as the Essential Air Service exist with much larger budgets ranging in the hundreds of millions of dollars. This puts the budgeted cost of this program within the DOT’s jurisdiction.

Government Action

Given the minor costs associated with the program and the bipartisan nature of infrastructure legislation, the creation of this fellowship, whether as an add-on to a bill or a stand-alone bill, is well within the realm of feasibility.

Automation/Single Pilot Solutions

The What:

Regulation allowing for single piloted flights and partially autonomous systems

The Who:

The U.S. Government, Major and Regional Airlines, and Aircraft Manufacturers

The Where:

Airports, Aircraft Manufacturers

The How:

Airbus, as well as Boeing with its recent acquisition of Aurora Flight Science, has been developing advanced autopilot and automation capabilities, allowing the right seat of commercial aircraft to be filled by an automated bot. DARPA funding has been instrumental in the development of this technology, and lead to programs such as Project ALIAS, which retrofits older aircraft with robotic controls that allow for the aging fleet to take advantage of advances in automation (Lowy, 2016). Next generation aircraft produced by both companies will support this type of advanced autopilot system natively. As this technology matures and public trust in autonomous systems strengthen, it will become more and more reasonable to suggest single pilot flights for shorter flights, and three pilot crews as opposed to four for longer duration routes.

The Why:

Recognizing the imminent pilot shortage, both airline manufacturers and government bodies have been mobilizing over the past five years to engineer technical solutions to this supply problem. While automation and autopilot functions in planes have been developed for decades, their growth is accelerating exponentially to make up for market conditions and the pilot shortage. Moving to increasingly automated systems allows for the potential of single pilot flights, mitigating the effects of the pilot shortage. Having aircraft with this technology built-in opens the door to additional regulatory schemes as well, which may prove vital under these increased demand conditions: while Captains will still require the same number of flight hours logged, it may be possible to cut the minimum required hours for First officers, if autonomous systems can prove themselves reliable, as they have over the past five years. This would alleviate another major barrier to entry, as the decreased number of hours required to sit in the right seat will allow for valuable on-the-job training, backed by a failsafe automation system.

Feasibility:

If tried to pass as a single major revision to FAA policy, it is unlikely that flights would be allowed to immediately go single pilot, First Officer training hours would be cut, and automation systems would be widely accepted. Instead, the burden lies with the aircraft manufacturers to incorporate this technology into next generation aircraft up to the point where it's ubiquitous and readily accepted -- it’s much easier to convince the FAA to update its policy to match already existent trends than it is to encourage the FAA to push new standards. However, aircraft manufacturers will only invest in this type of technology if demand for it exists, and so airline manufacturers must be willing to either retrofit their current fleets with advanced autopilot systems, or be willing to purchase automation enhanced aircraft. While this solution doesn’t increase the short term supply of pilots, it is a more likely long term solution, as it’s cheaper to build and maintain automation systems than it would otherwise be to hire the additional 600,000 pilots worldwide that Boeing projects will be required. While these systems will never be able to replace human pilots entirely -- human factors are essential to both the safety of and consumer confidence in aviation -- they can be a powerful tool for more efficiently using pilots and mitigating the effects of the pilot shortage.

Works Cited:

Sara Withrow and Melanie Stawicki Azam Illustrations by Raul Arias. (2017, April 19). The Pull of the Pilot Shortage. Retrieved October 15, 2017, from https://lift.erau.edu/pilot-shortage/

Office, U. G. (2014, February 28). Aviation Workforce: Current and Future Availability of Aviation Engineering and Maintenance Professionals. Retrieved October 15, 2017, from https://www.gao.gov/products/GAO-14-237

Epstein, C. (2016, December 22). Starting Salaries On the Rise at Regional Airlines. Retrieved October 15, 2017, from https://www.ainonline.com/aviation-news/air-transport/2016-12-22/starting-salaries-rise-regional-airlines

Bureau of Labor Statistics, U.S. Department of Labor, Occupational Outlook Handbook, 2016-17 Edition, Airline and Commercial Pilots, on the Internet at https://www.bls.gov/ooh/transportation-and-material-moving/airline-and-commercial-pilots.htm (visited October 14, 2017).

Boeing. (2016). 2016 Pilot and Technician Outlook. Retrieved October 15, 2017, from http://www.boeing.com/resources/boeingdotcom/commercial/services/assets/brochure/pilottechnicianoutlook.pdf

Lowy, J. (2016, October 18). That pilot in the cockpit may someday be a robot. Retrieved October 15, 2017, from https://phys.org/news/2016-10-cockpit-robot.html

Log in or sign up for Devpost to join the conversation.